Bitcoin-backed Loan

Coinbase's Bitcoin Loans Are Not What They Seem

Earlier today, Coinbase announced the launch of “Bitcoin-Backed Loans” using Base, its native blockchain. But there’s one problem. (Actually, two.)

These loans are not backed by Bitcoin, nor are they even on the Bitcoin blockchain.

It’s disappointing that, in 2025, companies are still willingly omitting key details to mislead Bitcoin holders into giving up custody of their coins.

Here’s the truth: these loans are collateralized by cbBTC, Coinbase’s Bitcoin-wrapped product designed to compete with wBTC and tBTC. This is not Bitcoin. In fact, cbBTC is arguably the most centralized of these “wrapped” BTC tokens. To understand the trust assumptions associated with wrapped BTC, I recommend this excellent post by the Bitcoin Layers team: Analyzing tBTC Against wBTC and cbBTC.

Here’s the TL;DR:

“The BTC backing the cbBTC token is held in reserve wallets managed by Coinbase, a US-based centralized custodial provider. Coinbase holds funds backing cbBTC in cold storage wallets across a number of geographically distributed locations and additionally has insurance on funds they custody.”

Furthermore, instead of issuing these loans on a blockchain even remotely related to Bitcoin (such as Bitcoin sidechains or Bitcoin L2s), Coinbase is issuing them through Morpho Labs, a DeFi platform best described as an AAVE competitor. While Morpho is a well-established platform—and I don’t doubt its security—it has no connection to Bitcoin.

I, for one, look forward to seeing actual Bitcoin-backed loans issued on the Bitcoin network itself. Many L2 teams are working hard to make this a reality, striving to minimize trust assumptions—or even eliminate the need for bridging altogether (bullish!).

Why do we need native Bitcoin-backed loans in the first place? Consider this: many Bitcoiners today face stringent tax regulations that impose hefty liabilities on long-term holders who sell their Bitcoin to fund significant purchases like a house or a car. Taking out a loan backed by BTC allows individuals to avoid triggering these tax events.

Moreover, most Bitcoiners are confident that Bitcoin’s price will be significantly higher in the future than it is today. So why would anyone sell an asset with such promising long-term potential? Bitcoin-backed loans enable holders to retain exposure to Bitcoin’s upside while accessing the liquidity needed to meet life’s financial demands.

In today’s market, the options for Bitcoin-backed lending are limited. You can either rely on centralized companies (like the reputable team at Unchained) or turn to “DeFi” protocols, which are often centralized themselves and, in some cases, riskier than centralized alternatives like Unchained. However, there is currently no truly Bitcoin-native solution—no option for Bitcoiners to maintain custody of their coins while accessing loans.

Some companies, like Lava.xyz, are beginning to address this gap. However, their market share remains a small fraction of the volumes handled by existing DeFi platforms. (Keep an eye on Lava—they’re poised to make waves in 2025!)

One quote from the original announcement stood out to me:

“The integration of Bitcoin-backed loans on Coinbase is ‘TradFi in the front, DeFi in the back,’” said Max Branzburg, Coinbase’s vice president of product, in a statement to The Block.

Let’s call it what it really is: centralized in the front, and centralized in the back.

It’s time to leave these misleading offerings behind and bring true Bitcoin Finance (BTCfi) to users—not just marketing buzzwords and half-truths.

Instead of saying: Bitcoin backed on-chain loans let’s say: multisig-backed derivatives loans on a centralized chain.

This article is a Take. Opinions expressed are entirely the author’s and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Articles I write may discuss topics or companies that are part of my firm’s investment portfolio (UTXO Management). The views expressed are solely my own and do not represent the opinions of my employer or its affiliates. I’m receiving no financial compensation for these takes. Readers should not consider this content as financial advice or an endorsement of any particular company or investment. Always do your own research before making financial decisions.

Source link

Founder: Nicolas Burtey

Date Founded: September 2019

Location of Headquarters: United States

Number of Employees: 11

Website: https://www.galoy.io/

Public or Private? Private

Last week, Galoy launched Lana, software that enables banks to accept bitcoin as collateral for loans.

Lana helps community and challenger banks (the banks with which Galoy is looking to work) to offer bitcoin-backed loans to various types of customers.

“Some banks might want to use it to sell to retail, and some might want to use it to sell commercial customers or high-net-worth individuals,” Burtey told Bitcoin Magazine.

In offering such loans to a wide array of customers, Burtey believes that the high cost of borrowing currently associated with such products will come down.

“Today’s interest rates are 12% to 15% if you want to get a loan using your bitcoin as collateral,” said Burtey.

“The rates are high because there are so few financial institutions offering this type of product. We see an opportunity now that the regulations are allowing banks to do things with bitcoin,” he added.

“We think a lot of banks will want to enter this market.”

If Burtey is correct in his prediction that banks are keen to offer bitcoin-backed loans, this will not only lower rates for such loans, but it will also introduce open-source Bitcoin software into the world of banking, which could initiate a new trend in the industry.

But more on that in just a minute. First, some background on Galoy.

Galoy’s History: From Blink Wallet To Lana

Founded in September 2019, Galoy had intentions to enable banks to use bitcoin from the start, but it had to hold off on doing so due to an unfriendly regulatory environment.

So, instead, it focused its efforts on creating and supporting Blink wallet (which was originally called the Bitcoin Beach wallet and which Galoy recently sold), a custodial Bitcoin and Lightning wallet predominantly used at first in El Salvador and then in Bitcoin circular economies globally.

“Galoy’s mission was to onboard banks to Bitcoin five years ago,” said Burtey.

“But the regulatory environment was so bad during the last five years that we decided to create Blink. The reason we are now focusing on our original mission is because with the end of Choke Point 2.0 and the repeal of SAB 121, we think now is the perfect time to help banks adopt Bitcoin.”

Burtey spoke about his work in creating and growing Blink fondly and shared that he had to stop working on the project only because it would be too difficult to continue managing it while also aiming to serve a new type of clientele.

“Blink is a B2C (Business-To-Customer) play, and it’s hard as an early-stage startup to focus on too many things,” explained Burtey.

“Galoy is a B2B (Business-To-Business)-driven business, and we want to work with banks and financial institutions,” he added.

“It’s good to be focused on just one thing.”

And, as mentioned, that one thing will now be Lana.

How Lana Works

Lana is software that Galoy helps banks integrate and manage for a subscription fee. With this software, banks can issue bitcoin-backed loans under the terms they create.

“We’re not the ones deciding how much interest will be charged or anything like that,” explained Burtey.

“We give banks the platform to do this, and then they can figure out their cost of capital, the duration of the loan, the liquidation price for the bitcoin in the loan and the rate at which they want to lend,” he added.

“We’re giving you software, and helping you run and automate that software.”

Something else that Galoy doesn’t do for banks is custody the bitcoin provided as collateral for the loans they issue. Each of the banks with whom the company works is responsible for selecting their own custodian.

“You can go to BitGo or Fireblocks or each loan can have its own multisig,” said Burtey. “We’re agnostic on custody.”

With that said, Lana helps banks monitor the bitcoin in custody so that banks can be aware of whether or not collateral is nearing liquidation levels.

“A key piece of this product is risk management,” said Burtey.

“Bitcoin is volatile, and the bank will need a tool to show that it’s taking calculated risk. So, we’ll provide banks with a dashboard to monitor this risk,” he added.

Who Will Use Lana?

Galoy is targeting community banks and other smaller financial institutions with this new product mostly because they think these smaller players will benefit most from it — and because the big banks likely won’t need such a product.

“We don’t think JP Morgan will really want to work with us,” said Burtey. “They’re probably building something like this themselves, whereas a smaller bank, a credit union or small company probably isn’t.”

Burtey also understands that smaller lenders’ incorporating Lana as opposed to building something comparable themselves can save these financial institutions a significant amount of time and effort.

“Our goal is to say, ‘Look, you can develop this internally, and it will take you six months, a year or longer depending on how much you know about Bitcoin,’” said Burtey. “‘Or we have a lending product as a service for you, and you can launch it much more quickly.’”

And as Burtey and his team onboard their first round of smaller banks, they’ll not only be making history in enabling more banks to accept bitcoin as collateral for loans, but they’ll potentially be altering the trajectory of banking in general by introducing open-source software to it.

Open-Source Bitcoin Banking

Burtey’s long-term vision for Galoy is to do much more than just help banks issue bitcoin-backed loans. He’s looking to introduce open-source software into banking as more banks begin to embrace Bitcoin.

However, it’s important to note that Lana isn’t open-source just yet. It’s fair-source software, and, under such a license, code becomes open-source after two years.

“It’s a delayed open-source system, but it’s all available on GitHub,” said Burtey. “You can go and try it, test it, and play with it on your own.

Under the fair-source license, no company other than Galoy can sell the product to a bank right now, allowing Galoy to profit while still building with auditable code.

“We sell the deployment, and we help banks to plug in to their custodian,” explained Burtey. “We’re building in the open — but we also want to generate revenue.”

Beyond helping banks implement Lana, Burtey’s wants to develop open-source “core banking software,” as he’s looking to disrupt the “core ledger” oligopoly.

“The core ledger is where banks store the account data, customer information and transaction details,” said Burtey. “It’s the source of truth for banks.”

And only three companies — FIS, Fiserv and Jack Henry — have the core ledger market cornered.

“These are all like hundred billion dollar companies that you’ve probably never heard about because all they do is focus on selling software to banks,” said Burtey.

“Our long-term goal is to disrupt this industry by making something that is open source,” said Burtey. “Today, there is no company that does core banking with the idea of open source, and so we’re working towards this.”

Burtey envisions a world in which open-source software can make it much easier for someone to start a Bitcoin bank. (For those who wince at the words “Bitcoin” and “bank” being used in tandem, might I remind you that it was the legendary Hal Finney himself who wrote that bitcoin-backed banks would serve as a scaling solution.)

“To start a bank today is a very expensive and complicated process,” said Burtey. “You have to pay $100,000 plus just to purchase the core ledger technology.”

Burtey then referenced his own experience in starting Blink wallet, essentially a bitcoin bank run on open-source code, before continuing.

“I just went to El Salvador and started what was effectively my own bank because I wanted to,” said Burtey.

“We need to reinvent how core banking software is being made in the world of Bitcoin, and I think this is where open-source becomes relevant,” he added.

“This is really why I think the world of banking and Bitcoin will be very different from the world of banking with fiat, and I think we’re one of the companies at the forefront of this.”

Source link

Over the past year, the Bitcoin Renaissance has brought significant attention to BTCfi, or “Bitcoin DeFi” applications. Despite the hype, very few of these applications have delivered on their promises or managed to retain a meaningful number of “actual” users.

To put things into perspective, the leading lending platform for Bitcoin assets, Liquidium, allows users to borrow against their Runes, Ordinals, and BRC-20 assets. Where does the yield come from, you ask? Just like any other loan, borrowers pay an interest rate to lenders in exchange for their Bitcoin. Additionally, to ensure the security of the loans, they are always overcollateralized by the Bitcoin assets themselves.

How big is Bitcoin DeFi right now? It depends on your perspective.

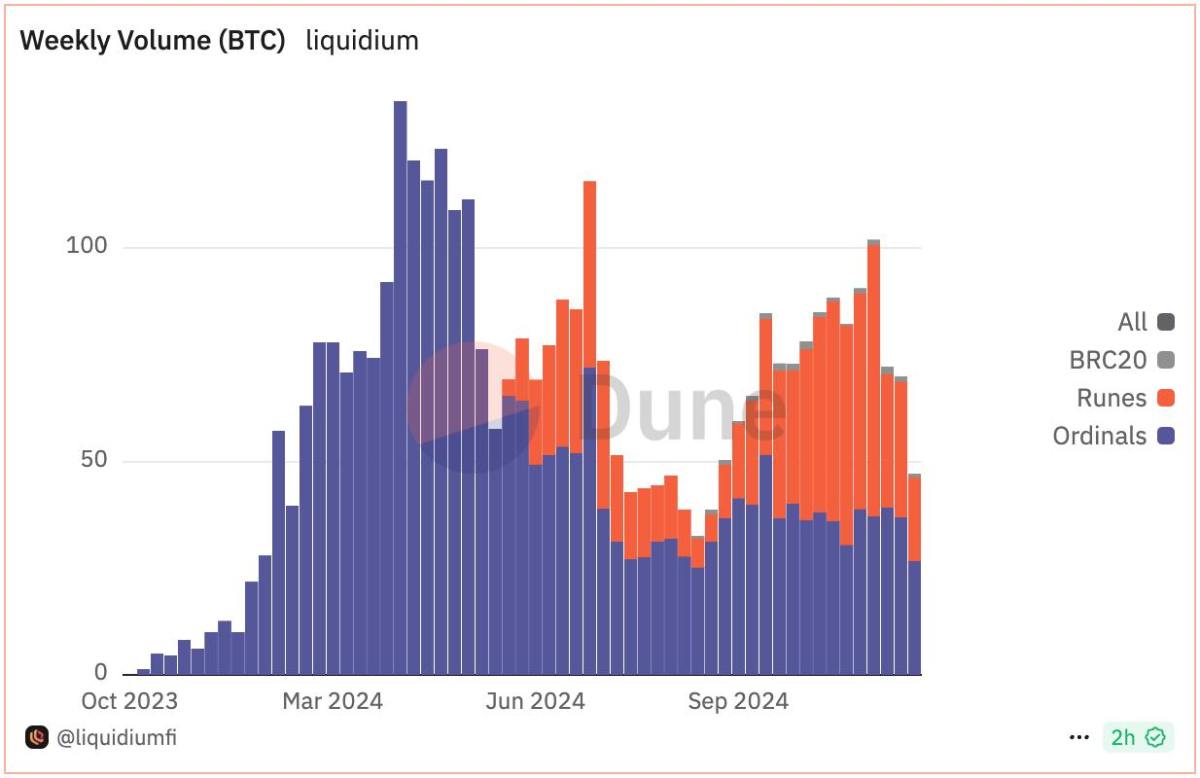

In about 12 months, Liquidium has executed over 75,000 loans, representing more than $360 million in total loan volume, and paid over $6.3 million in native BTC interest to lenders.

For BTCfi to be considered “real,” I would argue that these numbers need to grow exponentially and become comparable to those on other chains such as Ethereum or Solana. (Although, I firmly believe that over time, comparisons will become irrelevant as all economic activity will ultimately settle on Bitcoin.)

That said, these achievements are impressive for a protocol that’s barely a year old, operating on a chain where even the slightest mention of DeFi often meets with extreme skepticism. For additional context, Liquidium is already outpacing altcoin competitors such as NFTfi, Arcade, and Sharky in volume.

Bitcoin is evolving in real time, without requiring changes to its base protocol — I’m here for it.

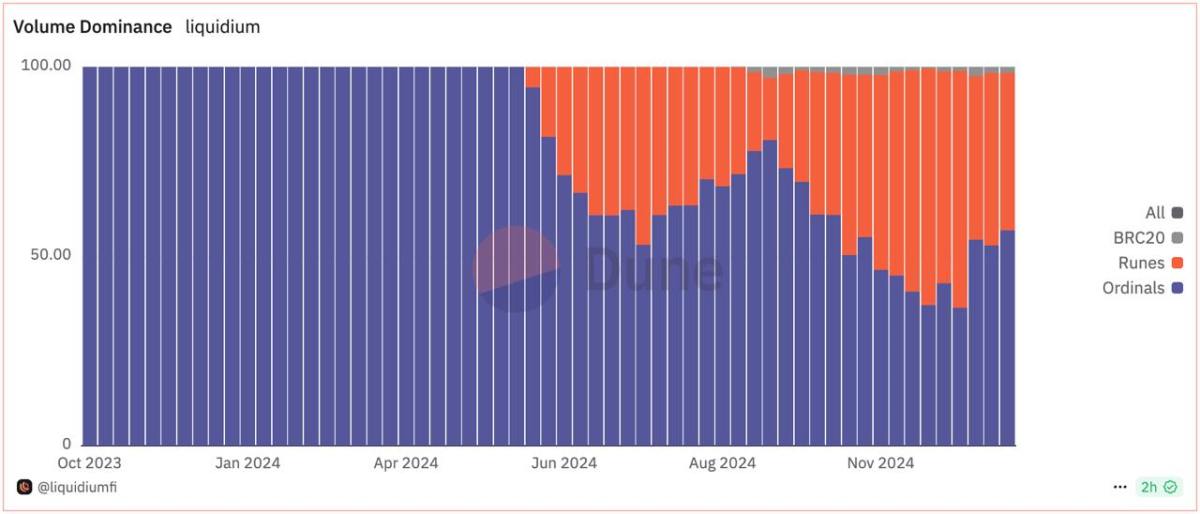

After a rocky start, Runes are now responsible for the majority of loans taken out on Liquidium, outpacing both Ordinals and BRC-20s. Runes is a significantly more efficient protocol that offers a lighter load on the Bitcoin blockchain and delivers a slightly improved user experience. The enhanced user experience provided by Runes not only simplifies the process for existing users, but also attracts a substantial number of new users that would be willing to interest on-chain in a more complex way. In contrast, BRC-20 struggled to acquire new users due to its complexity and less intuitive design. Having additional financial infrastructure like P2P loans is therefore marking a step forward in the usability and adoption of Runes, and potentially other Bitcoin backed assets down the line.

The volume of loans on Liquidium has consistently increased over the past year, with Runes now comprising the majority of activity on the platform.

Ok so Runes are now the dominant asset backing Bitcoin native loans, why should I care? Is this good for Bitcoin?

I would argue that, regardless of your personal opinion about Runes or the on-chain degen games happening right now, the fact that real people trust the Bitcoin blockchain to take out decentralized loans denominated in Bitcoin should make freedom lovers stand up and cheer.

We’re winning.

Bitcoiners have always asserted that no other blockchain can match Bitcoin’s security guarantees. Now, others are beginning to see this too, bringing new forms of economic activity on-chain. This is undeniably bullish.

Moreover, all transactions are natively secured on the Bitcoin blockchain—no wrapping, no bridging, just Bitcoin. We should encourage and support people who are building in this way.

This article is a Take. Opinions expressed are entirely the author’s and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Source link

Can a Meme Coin Fund the Future of Scientific Research?

Analyst Confirms XRP Price Is Still On Path To $130

Proof-of-Work Crypto Mining Doesn’t Trigger Securities Laws, SEC Says

Crypto campaign donations are democracy at work — former Kraken exec

1 Million Bitcoin In New Whale Hands—A Mega BTC Rally On The Horizon?

Argentina’s Senate Hosts First-Ever Conference On Bitcoin Regulation

Justin Sun Stakes $100,000,000 Worth of Ethereum Amid Calls for ‘Tron Meme Season’

Cardano wallet Lace adds Bitcoin support

Donald Trump Vows to Make America the ‘Undisputed Bitcoin Superpower’

Will Trump Announce Zero Tax Gains in Today’s Crypto Summit Talk?

Avalanche (AVAX) Drops 4.5%, Leading Index Lower

Tether’s US treasury holdings surpass Canada, Taiwan, ranks 7th globally

Here’s Where Support & Resistance Lies For Solana, Based On On-Chain Data

President Trump To Address The Digital Assets Summit Tomorrow

Analyst Says Bitcoin Primed for ‘Party Time’ if BTC Breaks Above Critical Level, Updates Outlook on Chainlink

24/7 Cryptocurrency News4 months ago

24/7 Cryptocurrency News4 months agoArthur Hayes, Murad’s Prediction For Meme Coins, AI & DeFi Coins For 2025

Bitcoin2 months ago

Bitcoin2 months agoExpert Sees Bitcoin Dipping To $50K While Bullish Signs Persist

24/7 Cryptocurrency News2 months ago

24/7 Cryptocurrency News2 months agoAptos Leverages Chainlink To Enhance Scalability and Data Access

Bitcoin5 months ago

Bitcoin5 months agoBitcoin Could Rally to $80,000 on the Eve of US Elections

Altcoins2 months ago

Altcoins2 months agoSonic Now ‘Golden Standard’ of Layer-2s After Scaling Transactions to 16,000+ per Second, Says Andre Cronje

Bitcoin4 months ago

Bitcoin4 months agoInstitutional Investors Go All In on Crypto as 57% Plan to Boost Allocations as Bull Run Heats Up, Sygnum Survey Reveals

Opinion5 months ago

Opinion5 months agoCrypto’s Big Trump Gamble Is Risky

Price analysis5 months ago

Price analysis5 months agoRipple-SEC Case Ends, But These 3 Rivals Could Jump 500x