Borrowing

Why You May Want To Redeem Your Bitcoin From THORChain's Lending Service

Two days ago, the atebites X account pointed out that THORChain’s lending service currently has nowhere near enough bitcoin to repay its creditors.

As of the time of the post, the total amount of bitcoin to be repaid to depositors was 1,604, while the lending pool only had 592 bitcoin in it.

We need to be raising awareness on just how bad of a shape Thorchain lending is right now, posing a potential risk to the protocol itself.

As it stands, at current mark to market rates for RUNE, complete loan closure will mint 24 million RUNE.

1,604 in BTC collateral, 18,258… pic.twitter.com/OykZbMQCdx

— atebites (@ate_bites) January 8, 2025

As Lava founder Shehzan Maredia explained in a post on X, when you borrow on THORChain, they sell the bitcoin you put up as collateral for their own token, RUNE. When you repay your loan, they sell the RUNE for bitcoin to give you back your collateral.

I predicted the Thorchain collapse in 2023 when they launched their "lending" feature, and it's happening now. The lesson people never seem to learn: any system in crypto that can fail will fail.

When you borrowed on Thorchain, they would sell your BTC collateral for their…

— Shehzan (@MarediaShehzan) January 10, 2025

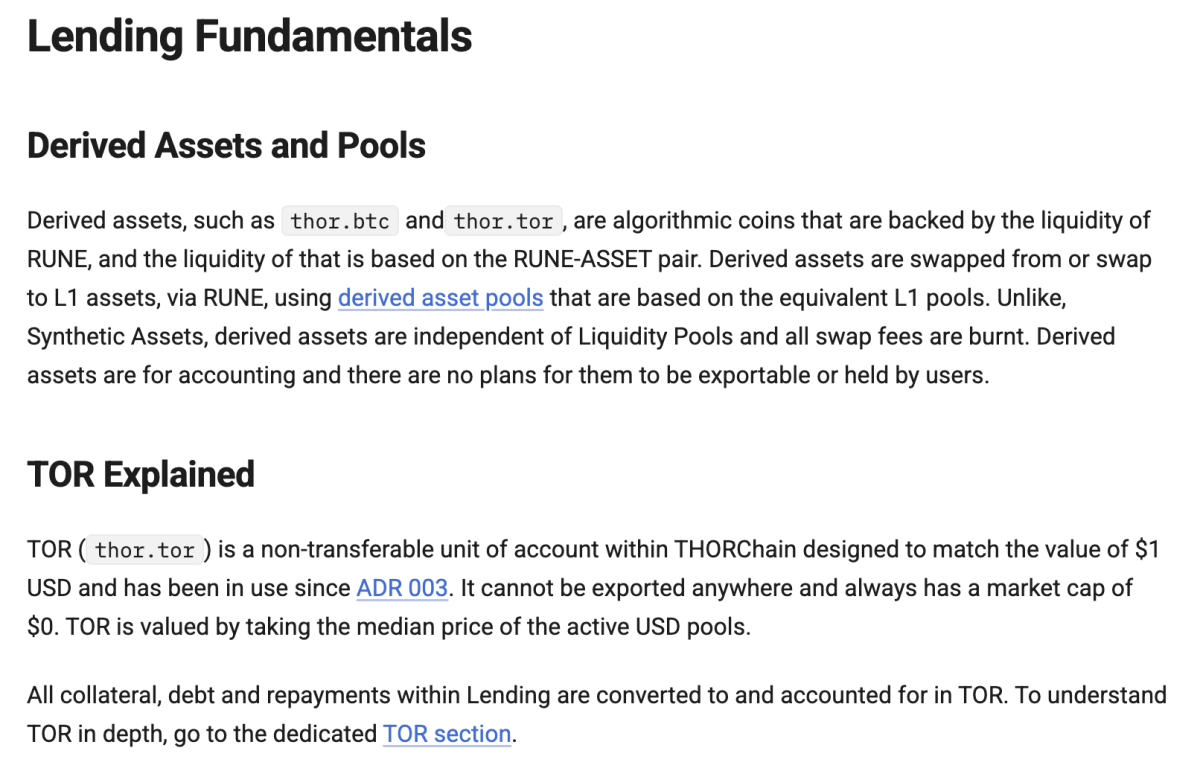

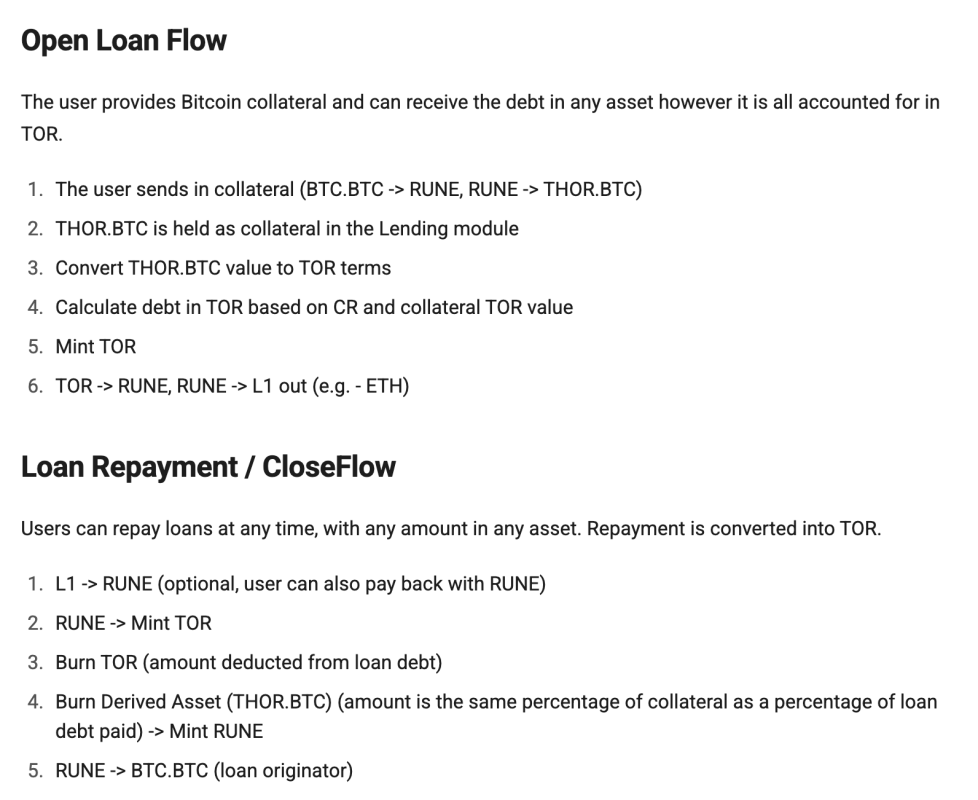

The actual mechanics of how this works are a bit more complex and are detailed on THORChain’s website.

See screenshots from the website below:

The primary issue in this scenario is that half of the value borrowed in U.S. dollar denominations was borrowed when bitcoin traded at significantly lower prices than that at which bitcoin trades today, according to atebites.

This means that for THORChain to meet its current demands, it will need to mint upwards of 24 million RUNE (as of January 8). While this would only be about 8% of the circulating supply of RUNE, it would lead to a reduction in the price of the asset, which would give THORChain even less purchasing power as they try to buy bitcoin back on behalf of their creditors.

If traders were to start shorting RUNE on top of this, THORChain’s ability to purchase the required amount of bitcoin to redeem its creditors would diminish even further.

This could lead to something akin to the Terra/Luna death spiral we saw in 2022.

With that said, prominent supporter of the project Erik Voorhees shared that THORChain’s lending service is operating as it was intended to and that there is no foreseeable danger.

Thorchain continues working as designed.

Yes, loan redemptions cause downward pressure on RUNE price, but scale is not dangerous.

If you're worried, just go pay off your loan.

— Erik Voorhees (@ErikVoorhees) January 10, 2025

A core developer for THORChain that goes by the name Nine Realms on X also made the case that THORChain is resilient:

1/ Addressing Community Concerns

There's been a lot of discussion recently about the state of the network and the outstanding lending protocol liability.

Let’s dive into the facts to shed light on what’s really happening and why we remain confident in THORChain's resilience.

— Nine Realms (@ninerealms_cap) January 10, 2025

While it surely isn’t a given that this situation will end in disaster, you may want to redeem the bitcoin you’ve put up as collateral via THORChain’s lending service just in case.

This article is a Take. Opinions expressed are entirely the author’s and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Source link

Company Name: Ledn

Founders: Mauricio Di Bartolomeo and Adam Reeds

Date Founded: September 2018

Location of Headquarters: N/A (Fully remote)

Number of Employees: 51

Website: https://ledn.io/

Public or Private? Private

“Lending is the type of relationship where you value the return of your assets more than the return on your assets.”

This was Di Bartolomeo’s answer when I asked him what has set Ledn, a bitcoin and crypto borrowing and lending platform, apart from its competitors, including now defunct companies that offered similar services like BlockFi, Celsius and Voyager.

“There’s no company in this space that has a better track record of returning your assets than Ledn,” Di Bartolomeo told Bitcoin Magazine.

Since its founding, Ledn has prioritized security and reliability. Di Bartolomeo and his co-founder, Adam Reeds, have not only wanted to win the trust of the traditional financial institutions with which Ledn interfaces but that of Ledn’s global user base, some of whom are accessing financial services for the first time thanks to the company.

And Di Bartolomeo’s work is quite personal to him in part because he understands the importance of Bitcoin thanks to his firsthand experience with it in his home country of Venezuela.

Di Bartolomeo’s Bitcoin Journey

“My family found Bitcoin and started mining it in Venezuela in late 2014/early 2015 in the middle of hyperinflation where basically it was illegal for them to buy or hold U.S. dollars or anything that would preserve value,” recounted Di Bartolomeo.

“When I saw how they and other Venezuelans were using Bitcoin to opt out of their broken system, I thought to myself “How many people in the world live like this and how many people in the world are going to need this?” And my answer was a number that I couldn’t compute in my head,” he added.

Di Bartolomeo decided to begin working in the Bitcoin space soon after. He moved to Canada where he and Reeds began helping miners grow their operations. Di Bartolomeo recalled that these miners wanted to expand but didn’t want to sell their bitcoin to do so.

“They had bitcoin revenues and fiat expenses, and there was no real place for them to get any type of financing,” said Di Bartolomeo.

“We sought financing, but nobody would give us a loan. So, we decided to solve our own problem,” he added.

“That was the genesis of Ledn.”

How Ledn Differentiated Itself

When Ledn was founded in 2018, only a few other services like it existed. However, there was a notable difference between Ledn and its competitors.

“There were other bitcoin-backed lenders in the market, but they required tokens,” said Di Bartolomeo.

“This was around the ICO era and we saw Nexo and Celsius come into the space with tokens. My view was that they were only using them to raise cash without selling off equity,” he added.

Di Bartolomeo and Reeds didn’t want to issue a token, as they saw it as a questionable practice from a regulatory perspective.

“When you look at finance at scale, immediately you think about compliance and regulation,” said Di Bartolomeo. “We wanted to build a company that was able to sit in front of BlackRock or Goldman Sachs, heavily regulated banks, and say, ‘Hey, I want to interact with you guys.’”

What is more, Ledn also prioritized transparency. In 2021, it became one of the first major Bitcoin companies to issue a proof of reserves, a system that allows anyone to audit Ledn’s bitcoin holdings.

“We’re still the only lender operating in the U.S. or other highly-regulated markets that has this proof of reserves where every six months our clients can come and check it out,” said Di Bartolomeo. “We’ve been doing this since before it was cool.”

Ledn also publishes a monthly Open Book Report that breaks down Ledn’s lending strategies.

From early on, Di Bartolomeo believed that taking a buttoned-up and transparent approach would foster trust amongst Bitcoin enthusiasts, a group that lives by the “don’t trust, verify” mantra, and his thesis has played out.

Reducing Risks

Of the many products Ledn offers, one is yield generation on bitcoin — the same type of product that caused the demise of BlockFi.

However, Ledn approaches its version of this product differently than its former competitor did.

“We generate Bitcoin yield on bitcoin primarily by lending it to market makers that arbitrage the BlockRock IBIT ETF and units of Coinbase spot,” said Di Bartolomeo.

“These groups are price neutral. They don’t have directional exposure. They’re just closing price gaps and benefitting from volatility,” he added.

BlockFi’s approach was far riskier.

“With BlockFi, there was a duration mismatch,” explained Di Bartolomeo.

“They were taking open-term deposits, and they were deploying them into mining infrastructure that had five-year payback. What do you think is going to happen when somebody shows up before the five years are done?” he added, alluding to the notion that what happened to BlockFi seemed inevitable.

What is more, Ledn only deals in highly liquid assets like bitcoin (and ether, which they added in 2023), which helps alleviate asset liability mismatch risk.

“With bitcoin, you always have people on both sides of the house with demand,” said Di Bartolomeo.

“When you start supporting things like Shiba Inu or Dogecoin and people want to earn interest on those, you then have to turn that Dogecoin into something else, and you create asset liability mismatch in the process,” he added.

Di Bartolomeo also noted that all of Ledn’s products are ring-fenced from one another.

“When you’re paying for a custody loan, you are not exposed to the credit risk of our other products,” he said. “This is very similar to how traditional finance works, and it’s something we do very differently as compared to our now defunct peers.”

Growing Competition

As more people begin to view bitcoin as “pristine collateral,” more bitcoin borrowing and lending platforms are destined to pop up. Many already have.

Centralized bitcoin borrowing and lending services like Salt and Nexo remain competitors to Ledn, while institutional bitcoin financing services like Newmarket Capital’s Battery Finance are also poised to cut into Ledn’s business. And services that enable users to borrow against their bitcoin in a non-custodial manner, including Debifi and Lava, may also increase their market share.

Di Bartolomeo is aware of the competition but doesn’t seem concerned. In fact, he believes that in such a market, the biggest winner will be the consumer, and he doesn’t have any plans to change Ledn’s strategy. Instead, he’s looking to double down on what Ledn does best.

“Our sweet spot is going to be individuals or people who prioritize transparency, security of funds and compliance,” said Di Bartolomeo.

“Safety, trust and transparency are what makes Ledn stand out. There is no other operator like us in this space with an equivalent track record as far as loans processed, years in the business and cycles survived,” he added.

“This industry is volatile. You have to have the right expertise and the right set of values powering your team, and I think other companies would be hard pressed to demonstrate what we have over the time that we have. Will you be able to find something cheaper? Yes. Will that be riskier? Absolutely.”

Fostering Financial Inclusion

One of the primary ways in which Ledn differs from traditional borrowing and lending platforms is that its rates don’t differ based on the jurisdiction in which the lender or borrower is located.

“This makes people feel very empowered because they know that whether they’re in Madrid or Medellín, they’re getting the same rate,” said Di Bartolomeo.

And Di Bartolomeo smiled from ear to ear as he discussed this point, as it seemed to remind him of why he got involved with Bitcoin in the first place.

“This is one of the things that makes me proudest about this business,” he said.

“We have people back in Latin America who’ve come to us to say we are the first loan they’ve ever been approved for. This is because all we look at is ‘Did you complete KYC?’; ‘Are you a compliant citizen?’; ‘Do you have Bitcoin?,’” he added.

“It’s not ‘Where do you live?’; ‘Who are your parents?’; What’s your skin color?’ I love this aspect of Bitcoin and what we do.”

Source link

This Week in Bitcoin: Strategy Stalls, But White House Plans to Buy More BTC

Layer3 (L3) Price Prediction March 2025, 2026, 2030, 2040

Ripple Token Zooms 5% Higher as Bitcoin Grapples With $84K Level

Bitcoin’s megaphone pattern, explained: How to trade it

Is Bitcoin Price Headed For $70,000 Or $300,000? What The Charts Are Saying

This Rare Bitcoin Buy Signal Could Ignite Next BTC Rally

There’s a Good Chance the Bull Cycle’s Over if Bitcoin Plunges to This Level, Warns Analyst Benjamin Cowen

Ethena overtakes PancakeSwap and Jupiter with $3.28m daily revenue

Gold ETFs Winning the Asset Race With Bitcoin Funds–for Now

BTC Regains $84K; ETH, XRP, SOL Pump

Court Approves 3AC’s $1.53B Claim Against FTX, Setting Up Major Creditor Battle

Sacks and his VC firm sold over $200M in crypto and stocks before WH role

Polkadot (DOT) Price Stability Fuels Hopes For Short-Term Recovery

Bitcoin Is A Strategic Asset, Not XRP

Bank of America Insider Helps Criminals and Illicit Businesses Launder Funds in Massive Global Conspiracy: US Department of Justice

24/7 Cryptocurrency News4 months ago

24/7 Cryptocurrency News4 months agoArthur Hayes, Murad’s Prediction For Meme Coins, AI & DeFi Coins For 2025

Bitcoin2 months ago

Bitcoin2 months agoExpert Sees Bitcoin Dipping To $50K While Bullish Signs Persist

24/7 Cryptocurrency News2 months ago

24/7 Cryptocurrency News2 months agoAptos Leverages Chainlink To Enhance Scalability and Data Access

Bitcoin4 months ago

Bitcoin4 months agoBitcoin Could Rally to $80,000 on the Eve of US Elections

Bitcoin4 months ago

Bitcoin4 months agoInstitutional Investors Go All In on Crypto as 57% Plan to Boost Allocations as Bull Run Heats Up, Sygnum Survey Reveals

Altcoins1 month ago

Altcoins1 month agoSonic Now ‘Golden Standard’ of Layer-2s After Scaling Transactions to 16,000+ per Second, Says Andre Cronje

Opinion4 months ago

Opinion4 months agoCrypto’s Big Trump Gamble Is Risky

Price analysis4 months ago

Price analysis4 months agoRipple-SEC Case Ends, But These 3 Rivals Could Jump 500x