Bitcoin mining

F%$K Bad Research

This article is featured in Bitcoin Magazine’s “The Halving Issue”. Click here to get your copy. It is also report #1 of the “FUD Fighters” series powered by HIVE Digital Technologies LTD.

F%$K Bad Research: I spent over a month analyzing a bitcoin mining study and all I got was this trauma response.

“We must confess that our adversaries have a marked advantage over us in the discussion. In very few words they can announce a half-truth; and in order to demonstrate that it is incomplete, we are obliged to have recourse to long and dry dissertations.” — Frédéric Bastiat, Economic Sophisms, First Series (1845)

“The amount of energy needed to refute bullshit is an order of magnitude bigger than that needed to produce it.” — Williamson (2016) on Brandolini’s Law

For too long, the world has had to endure the fallout of subpar academic research on bitcoin mining’s energy use and environmental impact. The outcome of this bullshit research has been shocking news headlines that have turned some well-meaning people into angry politicians and deranged activists. So that you never have to endure the brutality of one of these sloppy papers, I’ve sacrificed my soul to the bitcoin mining gods and performed a full-scale analysis of a study from the United Nations University, published recently in the American Geophysical Union’s Earth’s Future. Only the bravest and hardest of all bitcoin autists may proceed to the following paragraphs, the rest of you can go back to watching the price chart.

Your soft baby ears might have screamed with shock at the strong proclamation in my lede that the biggest and squeakiest research on bitcoin mining is bullshit. If you’ve ever read Jonathan Koomey’s 2018 blog post on the Digiconomist–also known as Alex deVries, or his 2019 Coincenter report, or Lei et al. 2021, or Sai and Vranken 2023, or Masanet et al. 2021, or… Well, the point is that there’s thousands of words already written that have shown that bitcoin mining energy modeling is in a state of crisis and that this is not isolated to bitcoin! It’s a struggle that data center energy studies have faced for decades. People like Jonathan Koomey, Eric Masanet, Arman Shehabi, and those nice guys Sai and Vranken (sorry, we’re not yet on a first-name basis) have written enough pages that could probably cover the walls of at least one men’s bathroom at every bitcoin conference that’s happened last year, that show this to be true.

My holy altar, which I keep in my bedroom closet, is a hand-carved, elegant yet ascetic shrine to Koomey, Masanet, and Shehabi for the decades of work they’ve done to improve data center energy modeling. These sifus of computing have made it all very clear to me: if you don’t have bottom-up data and you rely on historical trends while ignoring IT device energy efficiency trends and what drives demand, then your research is bullshit. And so, with one broad yet very surgical stroke, I swipe left on Mora et al. (2018), deVries (2018, 2019, 2020, 2021, 2022, and 2023), Stoll et al. (2019), Gallersdorfer et al. (2020), Chamanara et al. (2023), and all the others that are mentioned in Sai and Vranken’s comprehensive review of the literature. World, let these burn in one violent yet metaphorically majestic mega-fire somewhere off the coast of the Pacific Northwest. Reporters, and policymakers, please, I implore you to stop listening to Earthjustice, Sierra Club, and Greenpeace for they know not what they do. Absolve them of their sins, for they are but sheep. Amen.

Now that I’ve set the mood for you, my pious reader, I will now tell you a story about a recent bitcoin energy study. I pray to the bitcoin gods that this will be the last one I ever write, and the last one you’ll ever need to read, but my feeling is that the gods are punishing gods and will not have mercy on my soul–even in a bull market. One deep breath (cue Heath Ledger’s Joker) and Here… We… Go.

On a somewhat bearish October afternoon, I got tagged on Twitter/X on a post about a new bitcoin energy use study from some authors affiliated with the United Nations University (Chamanara et al., 2023). Little did I know that this study would trigger my autism so hard that I would descend into my own kind of drug-induced-gonzo-fear-and-loathing-in-vegas state, and hyper-focus on this study for the next four weeks. While I am probably exaggerating about the heavy drug use, my recollection of this time is very much a techno-colored, toxic relationship-level fever dream. Do you remember Frank from the critically acclaimed 2001 film, Donnie Darko? Yeah, he was there, too.

As I started taking notes on the paper, I realized that Chamanara et al.’s study was really confusing. The paper was perplexing because it’s a poorly designed study that bases its raison d’etre entirely on de Vries and Mora et al. It uses the Cambridge Center for Alternative Finance (CCAF) Cambridge Bitcoin Energy Consumption Index (CBECI) data without acknowledging the limitations of the model (see Lei et al. 2021 and Sai and Vranken 2023 for an in-depth analysis of the issues with CBECI’s modeling). It conflates its results from the 2020-2021 period with the state of bitcoin mining in 2022 and 2023. The authors also relied on some environmental footprint methodology that would make you think it was actually possible for you to shrink or grow a reservoir depending on how hard you Netflix and chill. Really, this is what Obringer et al. (2020) inferentially conclude is possible and the UN study cites Obringer as one of its methodological foundations. By the way, Koomey and Masanet did not like Obringer et al.’s methodology, either. I’ll light another soy-based candle at the altar in their honor.

Here’s a more clearly stated enumeration of the crux of the problem with Chamanara et al. (and by the way, their corresponding author never responded to my email asking for their data so I could, you know, verify, not trust. 🥴):

The authors conflated electricity use across multiple years, overreaching on what the results could reveal based on their methods.

The authors used historical trends to make present and future recommendations despite extensive peer-reviewed literature clearly showing that this leads to overestimates and exaggerated claims.

The paper promises an energy calculation that will reveal bitcoin’s true energy use and environmental impact. They use two sets of data from CBECI: i) total monthly energy consumption and ii) average hashrate share for the top ten countries where bitcoin mining is operated. Keep in mind that CBECI relies on IP addresses that are tracked at several mining pools. CBECI-affiliated mining pools represent an average of 34.8% of the total network hashrate. So, the data used likely have fairly wide uncertainty bars.

After about an hour or so of Troy Cross talking me off a rather impressive, art deco and weather-worn ledge that’s probably seen a few Great Gatsby flappers jump–a result of feeling an overwhelming sense of terror after my exasperated self realized that no amount of cognitive behavioral therapy would get me through this study–I determined the equation that the authors used to calculate the energy use shares for each of the top ten countries with the most share of hashrate (based on the IP address estimates) had to be the following:

Don’t let the math scare you. Here’s an example of how this equation works. Let’s say China has a shared share for January 2020 of 75%. Then, let’s also say that the total energy consumption for January 2020 was 10 TWh (these are made-up numbers for simplicity’s sake). Then, for one month, we’d find that China used 7.5 TWh of energy. Now, save that number in your memory palace and do the same operation for February 2020. Next, add the energy use for January to the energy use found for February. Do this for each subsequent month until you’ve added up all 12 months. You now have CBECI’s China’s annual energy consumption for 2020.

Before I show the table with my results, let me explain another caveat to the UN study. This study uses an older version of CBECI data. To be fair to the authors, they submitted their paper for review before CBECI updated their machine efficiency calculations. However, this means that Chamanara et al.’s results are not even close to realistic because we now believe that CBECI’s older model was overestimating energy use. Moreover, to do this comparison, I was limited to data through August 31, 2023, because CBECI switched to the new model for the rest of 2023. To get this older data, CCAF was generous and shared it with me upon request.

| Country | 2020 Energy Consumption (TWh) | 2021 Energy Consumption (TWh) | 2020 + 2021 Energy Consumption (TWh) | Chamanara et al.’s 2020 + 2021 Energy Consumption (TWh) | Percent Change Between 2020 + 2021 Calculations (%) |

|---|---|---|---|---|---|

Mainland China | 44.45 | 32.89 | 77.34 | 73.48 | 5.25 |

United States | 4.65 | 25.20 | 29.85 | 32.89 | -9.24 |

Kazakhstan | 3.18 | 12.06 | 15.24 | 15.94 | -4.39 |

Russia | 4.71 | 7.59 | 12.29 | 12.28 | 0.081 |

Malaysia | 3.31 | 4.13 | 7.44 | 7.29 | 2.06 |

Canada | 0.80 | 5.25 | 6.05 | 6.62 | -8.61 |

Iran | 2.33 | 3.06 | 5.39 | 5.13 | 4.82 |

Germany | 0.67 | 3.31 | 3.98 | 4.18 | -4.78 |

Ireland | 0.62 | 2.69 | 3.31 | 3.43 | -3.50 |

Singapore | 0.31 | 1.13 | 1.43 | 1.56 | -0.083 |

Other (Excluding Singapore) | 3.69 | 6.73 | 10.42 | 10.63 | -1.98 |

Total | 68.72 | 104.04 | 172.76 | 173.42 | -0.38 |

Another tricky thing about this study is that they combined the energy use for both 2020 and 2021 into one number. This was really tricky because if you look at their figures, you’ll notice that the biggest text states, “Total: 173.42 TWh”. It’s also slightly confusing because the figure caption states, “2020-2021”, which for many people would be interpreted as a period of 12 months, not 24 months. Well, whatever. I broke them up into their individual years so everyone could see the steps that were taken to get to these numbers.

Look at the far right column with the header, “Percent Change Between 2020 + 2021 Calculations (%)”. I calculated the percent change between my calculations and Chamanara et al.’s. This is rather curious, isn’t it? Based on my conversations with the researchers at CCAF, the numbers should be identical. Maybe the changelog doesn’t reflect a smaller change somewhere, but our numbers are slightly different nonetheless. China has a greater share and the United States has a smaller share in the data that CCAF shared with me compared to the UN study. Despite this, the totals are fairly close. So, let’s give the authors the benefit of the doubt and say that they did a reasonable job calculating the energy share, given the limitations of the CBECI model. Please bear in mind that noting that their calculation was reasonable doesn’t mean that it’s reasonable to use these historical estimates to make claims about the present and future and direct policy. It isn’t.

One evening while working by candlelight, I glanced to my left and saw Frank’s stabbing, black pupils (the Donnie Darko character I mentioned earlier) staring at me like two pieces of Stronghold waste coal, fixed in a quiet bed of pearly sand. He was reminding me that this report was still not finished and something about time travel. I grabbed my extra-soft curls (I switched to bar shampoo, it’s a godsend for frizz) and yanked as hard as I could. Willie Nelson’s 1974 Austin City Limits pilot episode blasting on my cheap-ass Chinese knock-off monitor’s mono speakers was moving through my ears like heroin through Lou Reed’s 4-lanes wide network of veins. Begrudgingly, I accepted my fate. I needed to go deeper down this rabbit hole. I needed to do a deeper analysis of the 2020 and 2021 CBECI data to show how important it is to do an annual analysis and not blur the years into one calculation. Realizing I was out of my hard liquor of choice, a splash of sherry in a Shirley Temple (shaken, not stirred), I grabbed a bottle of bootleg antiseptic that I got during the pandemic lockdown and chugged.

I flipped through my notes. I have lots of notes because I’m a serious person. What about the mining map issues? Can we do this through an analysis of the two separate years? What was happening for each of the ten countries? Does that tell us anything about where hashrate went after the China ban? What about the Kazakhstan crackdown? That’s post-2021, but the UN study acts like it never happened when they’re talking about the current mining distribution…

Not to the authors’ credit, they failed to mention to the peer-reviewers and to their readers that the mining map data only goes through January 2022. So, even though they talk about bitcoin mining’s energy mix as if it represents the present, they are completely wrong. Their analysis only captures historical trends, not the present and definitely not the future.

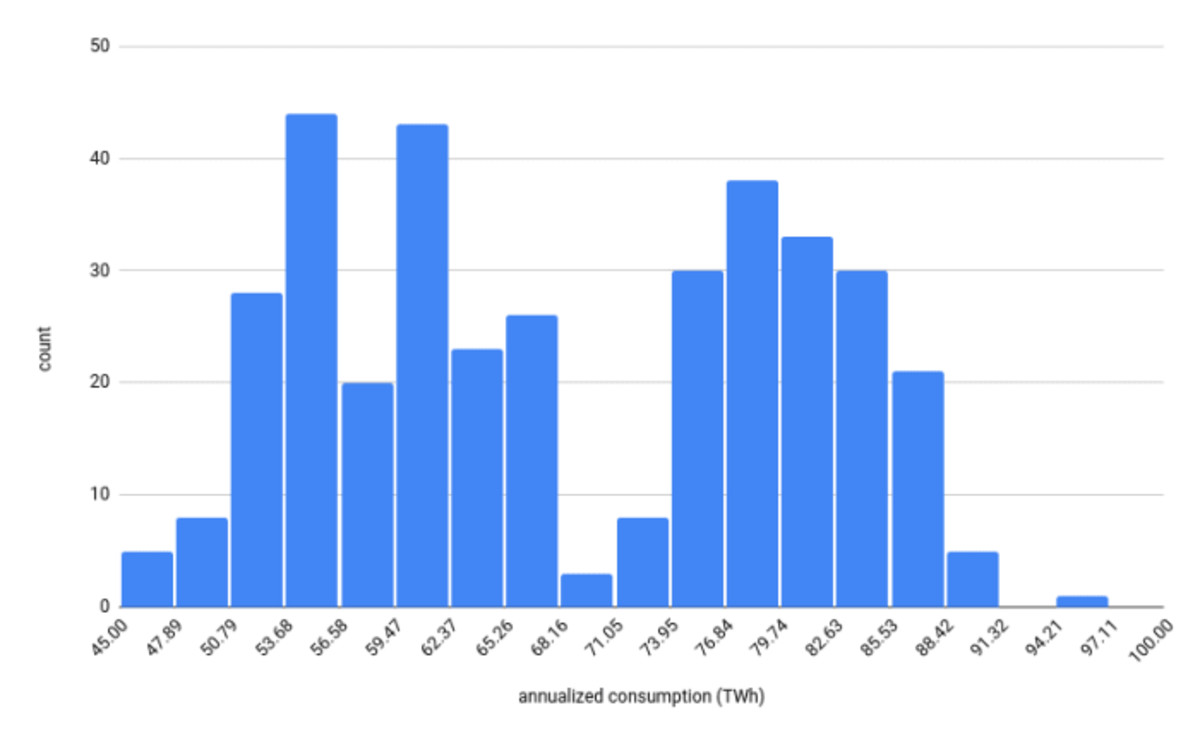

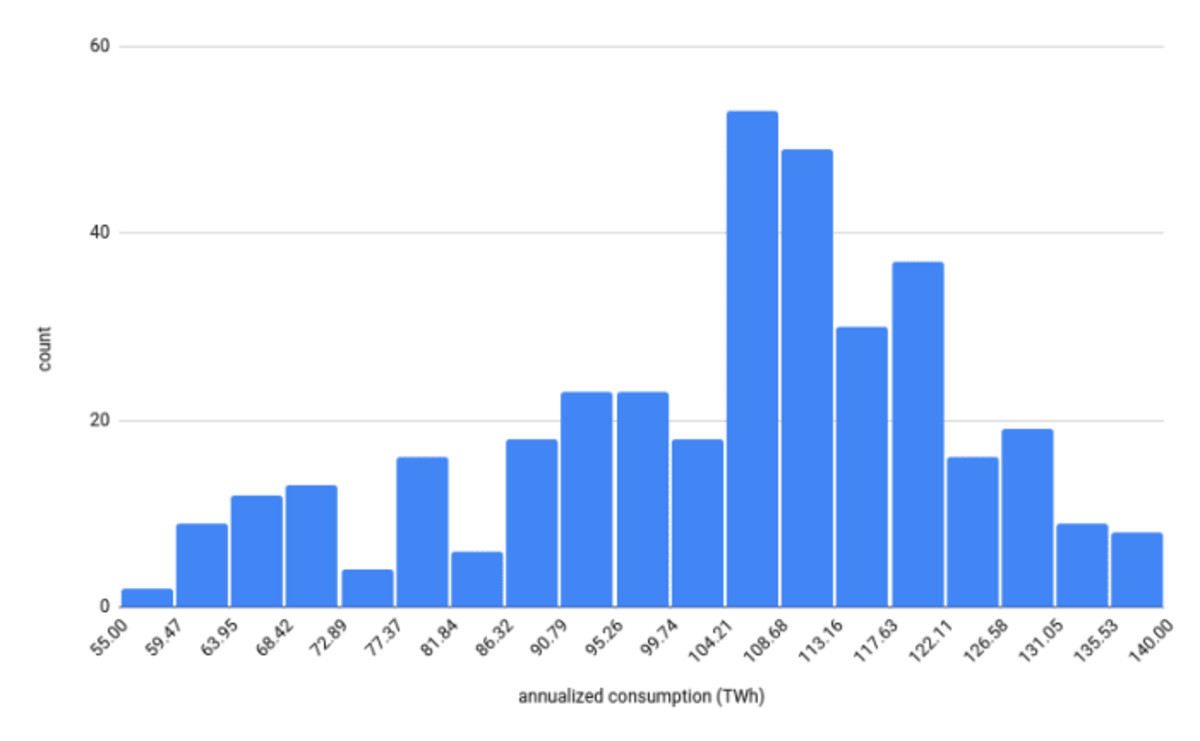

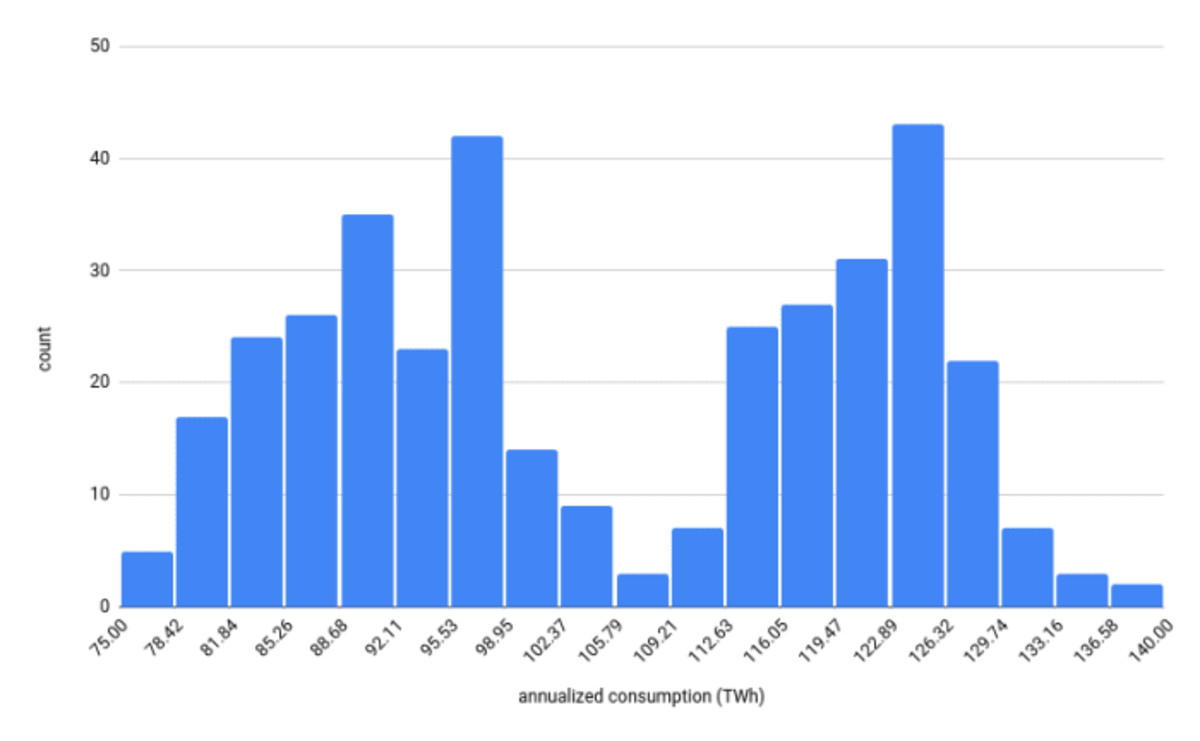

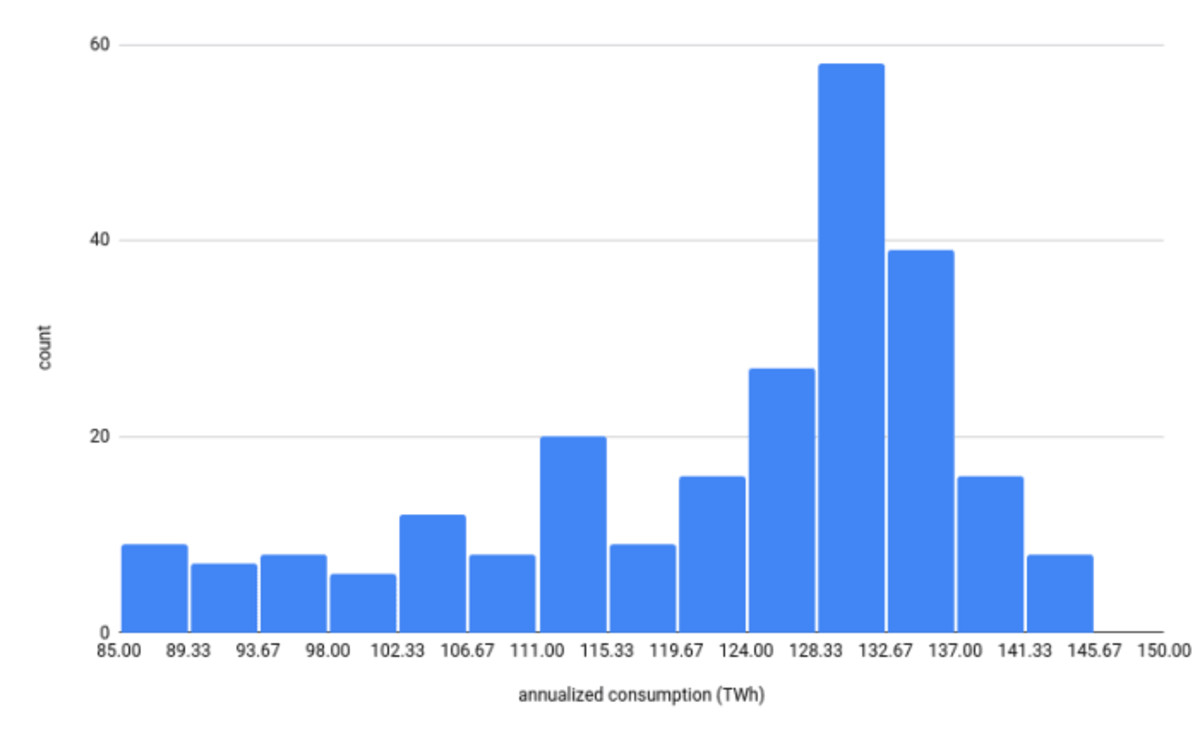

See this multi-colored plot of CBECI’s estimated daily energy use (TWh) from January 2020 through August 31, 2023? At this macro scale, we see plenty of variability. But also it’s apparent just from inspection that each year is different from the next in terms of variability and energy use. There are a number of possible reasons for the cause of variability at this scale. Some possible influences on energy use could be bitcoin price, difficulty adjustment, and machine efficiency. More macroscale influences could be as a result of regulation, such as the Chinese bitcoin mining ban that occurred in 2021. Many of the Chinese miners fled the country for other parts of the world, Kazakhstan and the United States are two countries where hashrate found refuge. In fact, the power of the Texas mining scene really came to be at this unprecedented moment in hashrate history.

Look at the histograms for 2020 (top left), 2021 (top right), 2022 (bottom left), and 2023 (bottom right). It’s obvious that for each year, the estimated annualized energy consumption data shows different distributions. Even though we do see some possible distribution patterns, we have to be careful not to take this as a pattern that happens every four-year cycle. We need more data to be sure. For now, what we can say is that some years in our analysis show a bimodal distribution while other years show a kind of skewed distribution. The main point here is to show that the statistics for energy use for each of these four years are different, and distinctly so for the two years that were used in Chamanara et al.’s analysis.

In the UN study, the authors wrote that bitcoin mining exceeded 100 TWh per year in 2021 and 2022. However, if we look at the histograms of the daily estimated annualized energy consumption, we can see that daily estimates vary quite a bit, and even in 2022 there were many days where the estimated energy consumption was below 100 TWh. We’re not denying that the final estimates were over 100 TWh in the older estimated data for these years. Instead, we’re showing that because bitcoin mining’s energy use is not constant from day to day or even minute-to-minute, it’s worth doing a deeper analysis to understand the origin of this variability and how it might affect energy use over time. Lastly, it’s worth noting that the updated data now estimates the annual energy use to be 89 TWh for 2021 and 95.53 TWh for 2022.

One last comment, Miller et al. 2022 showed that operations (specifically buildings) with high variability in energy use over time are generally not suitable for emission studies that use averaged annual emission factors. Yet, that’s what Chamanara et al. chose to do, and what so many of these bullshit models tend to do. A good portion of bitcoin mining doesn’t operate like a constant load, Bitcoin mining can be highly flexible in response to many factors from grid stability to price to regulation. It’s about time that researchers started thinking about bitcoin mining from this understanding. Had the authors spent even a modest amount of time reading previously published literature, rather than operating in a silo like Sai and Vranken noted in their review paper, they might have at least addressed this limitation in their study.

—

So, I’ve never been to a honky tonk joint before. At least not until I found myself in a taxi cab with several other conferencegoers at the North American Blockchain Summit. Fort Worth, Texas, is exactly what you’d imagine. Cowboy boots, gallon-sized cowboy hats, Wrangler blue jeans, and cowboys, cowboys, cowboys everywhere you looked through the main drag. On a brisk Friday night, Fort Worth seemed frozen in time, people actually walked around at night. The stores looked like the kind of mom-and-pop shops you’d see on an episode of The Twilight Zone. I felt completely disoriented.

My companions convinced me that I should learn how to two-step. Me, your standard California girl, whose physics advisor once told her that while you can take the girl out of California, you can’t take California out of the girl, should two-step?! I didn’t know a two-step from an electric slide and the only country I remember experiencing was a Garth Brooks commercial I saw once on television when I was a child. He was really popular in the nineties. That’s about as much country as this bitcoin mining researcher gets. The place was filled with kitschy gift shops and bright lights everywhere radiating from neon signs. At the center of the main room, a bartender wearing a black diamond studded belt with a white leather gun holster and lined with evenly spaced silver bullets. Who the hell knows what kind of gun he was packing, but it did remind me of the guns in the 1986 film, Three Amigos.

It was here, against the backdrop of what sounded like a country band that wasn’t entirely sure that it was country, that I watched the Texas Blockchain Council’s Lee Bratcher address a ball with the kind of trigonometric grace that you could only find at the end of a cue and land that billiard in a tattered, leather pocket for what seemed like the hundredth time that night. The smooth clank of billiard against billiard awoke something inside me. I realized that I was not yet out of the rabbit hole that Frank sent me down. I remembered somewhere scribbled in my notes that I had not plotted the hashrate share over time for the countries mentioned in the UN study. So, at half past three in the morning, I threw my head back to take a swig of some club soda and bumped it against the wall of the photo booth where nuclear families could pose with a mechanical bull, and fell unconscious.

Three hours later, I was back in my hotel room. Thankfully, someone placed some worthless fiat in my hand, loaded me into a cab, and had the driver take me back to the non-smoking room I checked into at the very center of the decay of twenty-first-century business travel, the Marriott Hotel. Fuzzy-brained and bleary-eyed, I let the blinding, dangerously blue light from my computer screen wash over my tired face and increase my chances of developing macular degeneration. I continued my analysis.

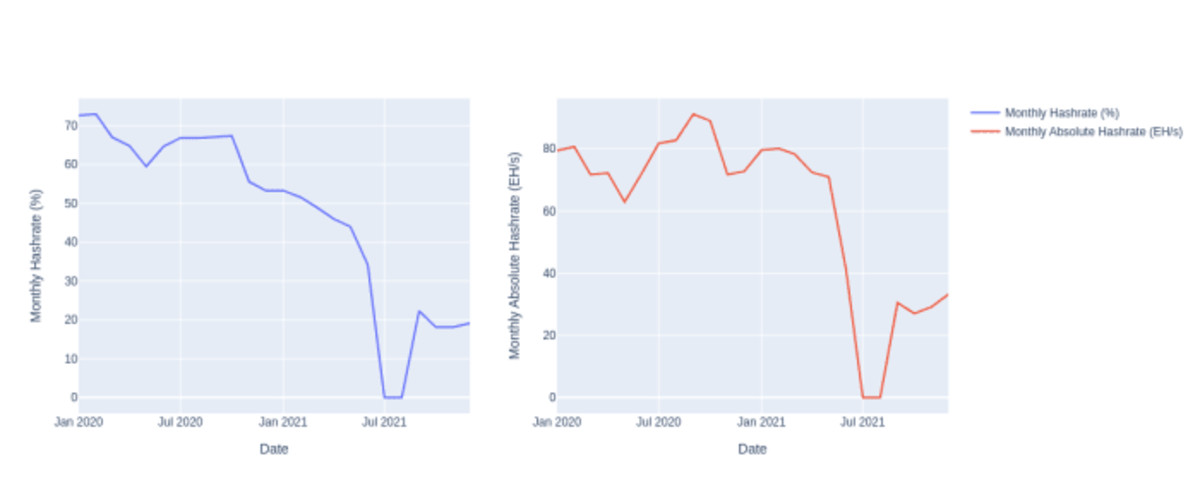

What follows are a series of plots of CBECI mining map data from January 2020 through January 2022. Unsurprisingly, Chamanara et al. focus attention on China’s contribution to energy use, and subsequently to its associated environmental footprint. China’s monthly hashrate peaked at over 70 percent of the network’s total hashrate in 2020. In July 2021, that hashrate share crashed to zero until it recovered to about 20 percent of the share at the end of 2021. We don’t know where it stands today, but industry insiders tell me it’s likely still hovering around this number, which means that in absolute terms, the hashrate is still growing there despite the ban.

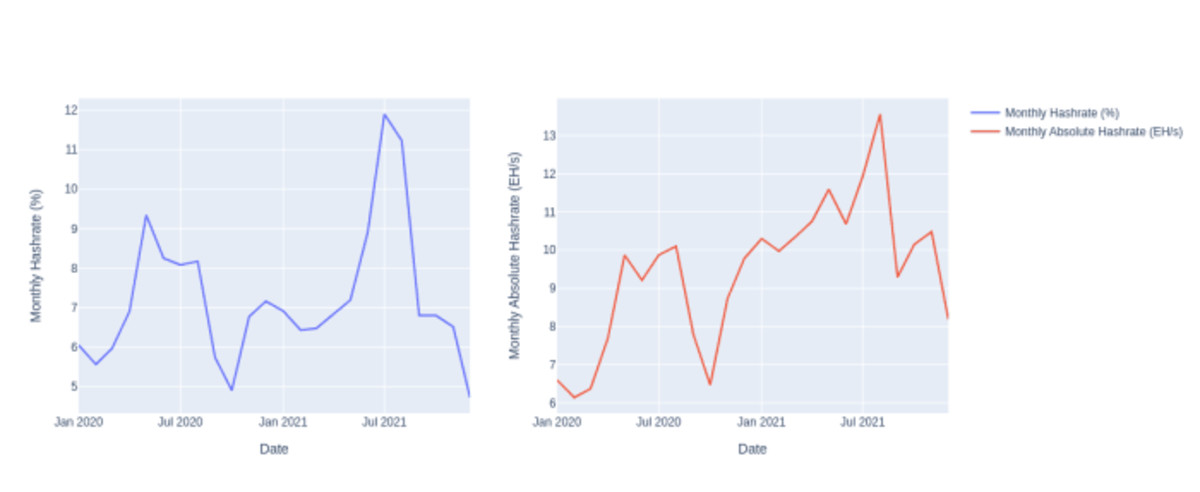

Russia, also unsurprisingly, gets discussed as well. Yet, based on the CBECI mining map data from January 2020 through January 2022, it’s hard to argue that Russia was an immediate off-taker of exiled hashrate. There’s certainly an immediate spike, but is this real or just miners using VPN to hide their mining operation? By the end of 2021, the Russian hashrate declined to below 5 percent of the hashrate and in absolute terms, declined from a brief peak of over 13 EH/s to a bit over 8 EH/s. When looking at the total year’s worth of CBECI estimated energy use for Russia, we do see that Russia did hold a significant portion of hashrate, it’s just not clear that when working with such a limited set of data, we can make any reasonable claims about the present contribution to hashrate and environment footprint for the network.

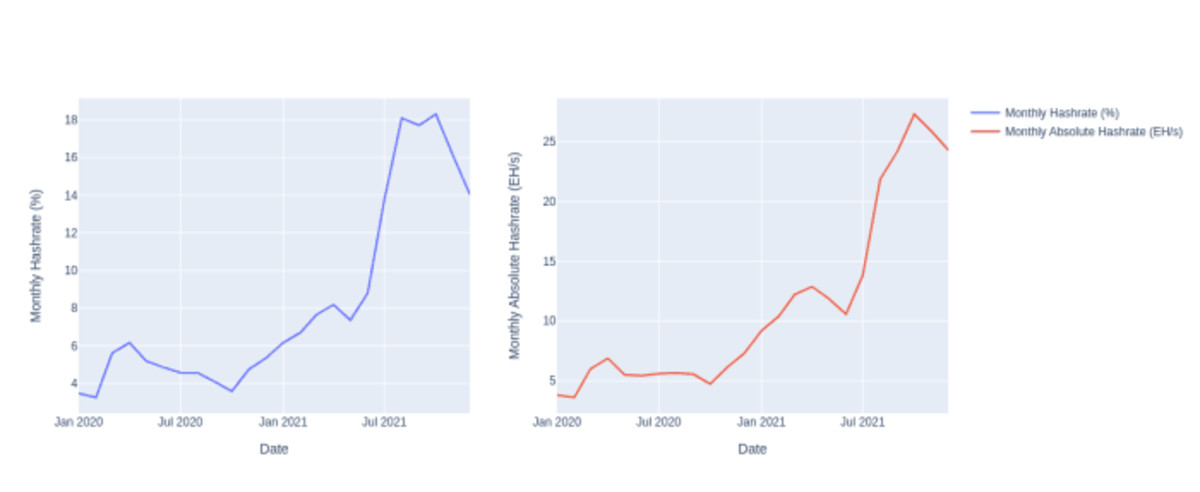

The most controversial discussion in Chamanara et al. deals with Kazakhstan’s share of energy use and environmental footprint. Obviously, the CBECI mining map data shows that there was a significant increase in hashrate share both in relative and absolute terms. It also appears that this trend started before the China ban was implemented, but certainly appears to rapidly increase just before and after the ban was implemented. However, we do see a sharp decline from December 2021 to January 2022. Was this an early signal that the government crackdown was coming in Kazakhstan?

In their analysis, Chamanara et al. ignored the recent Kazakhstan crackdown, where the government imposed an energy tax and mining licenses on the industry, effectively pushing hashrate out of the country. The authors overemphasized Kazakhstan as a current major contributor to bitcoin’s energy use and thus environmental footprint. If the authors had stayed within the limits of their methods and results, then noting the contribution of Kazakhstan’s hashrate share to the environmental footprint for the combined years of 2020 and 2021 would have been reasonable. Instead, not only do they ignore the government crackdown in 2022, but they also claim that Kazakhstan’s hashrate share increased by 34% based on 2023 CBECI numbers. CBECI’s data has not been updated since January 2022 and CCAF researchers are currently waiting for data from the mining pools that will allow them to update the mining map.

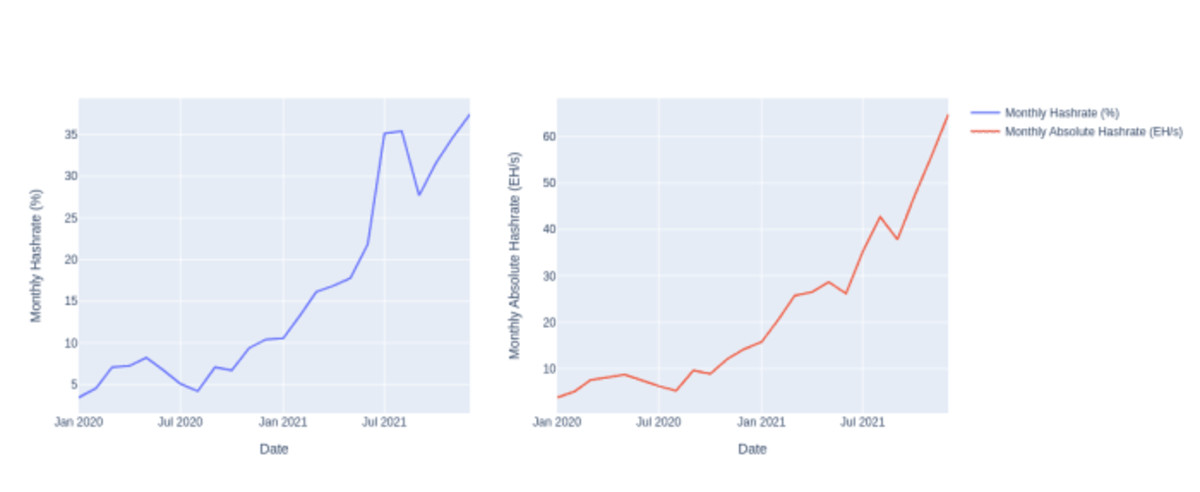

I know I’ve shown you, my faithful reader, a lot of data, but go ahead and have another shot of the hardest liquor you have in your cabinet, and let’s take a look at one more figure. This one represents the United States hashrate share in the older CBECI mining map data. The trend we see for the United States is also similar for Canada, Singapore, and what CBECI Calls “Other countries”, which represent the countries that did not make the top ten list for hashrate share. There’s a clear signal that reflects what we know to be true. The United States took a significant portion of Chinese hashrate and this hashrate share grew rapidly in 2021. While we know that the CBECI mining map data is limited to less than a majority of the network hashrate, I do think that their share is at least somewhat representative of the network’s geographic distribution. Hashrate geographic distribution seems to be heavily shaped by macro trends. While electricity prices matter, government stability and friendly laws play an important role. Chamanara et al. should have done this kind of analysis to help inform their discussion. If they had, they might have realized that the network is responding to external pressures at varying times and geographic scales. We need more data before we can make strong policy recommendations when it comes to the effects of bitcoin’s energy use.

—

At this point, I was no longer sure if I was a bitcoin researcher or an NPC, lost in a game where the only points tallied were for the intensity of self-loathing I was feeling for agreeing to this undertaking. At the same time, I could smell the end of this analysis was near and that, with enough somatic therapy and EMDR, I might actually remember who I used to be before I got dragged into this mess. Just two days prior, Frank and I had a falling out over whether Courier New was still the best font for displaying mathematical equations. I was alone in this rabbit hole now. I dug my fingers into the dirt walls surrounding me and slowly clawed my way back to sanity.

Upon exiting the hole, I grabbed my laptop and decided it was time to address the study’s environmental footprint methodology, wrap up this puppy, and put a bow on it. Chamanara et al. claimed that they followed the methods used by Ristic et al. (2019) and Obringer et al. (2020). There are a few reasons why their environmental footprint approach is flawed. First, the footprint factors are typically used for assessing the environmental footprint of energy generation. In Ristic et al., the authors developed a metric called the Relative Aggregated Factor that incorporated these factors. This metric allowed them to evaluate the placement of new electricity generators like nuclear or offshore wind. The idea behind this approach was to be mindful that while carbon dioxide emissions from fossil fuels were the main driver for developing energy transition goals, we should also avoid replacing fossil fuel generation with generation that could create environmental problems in different ways.

Second, Obringer et al. used many of the factors listed in Ristic et al. and combined them with network transmission factors from Aslan et al. (2018). This was a bad move because Koomey is a co-author on this paper, so it shouldn’t be surprising that in 2021, Koomey co-authored a commentary alongside Masanet where they called out Obringer et al. In Koomey and Masanet, 2021, the authors chided the assumption that short-term changes in demand would lead to immediate and proportional changes in electricity use. This critique could also be applied to Chamanara et al., which looked at a period when bitcoin was experiencing a run-up to an all-time high in price during a unique economic environment (low interest rates, COVID stimulus checks, and lockdowns). Koomey and Masanet made it clear in their commentary that ignoring the non-proportionality between energy and data flows in network equipment can yield inflated environmental-impact results.

More importantly, we have yet to characterize what this relationship looks like for bitcoin mining. Demand for traditional data centers is defined by the number of compute instances needed. What is the equivalent for bitcoin mining when we know that the block size is unchanging and the block pace is adjusted every two weeks to keep an average 10-minute spacing between each block? This deserves more attention.

Either way, Chamanara et al. did not seem to be aware of the criticisms of Obringer et al.’s approach. This is really problematic because as mentioned at the start of this screed, Koomey and Masanet laid the groundwork for data center energy research. They should have known not to apply these methods to bitcoin mining because while the industry has differences from a traditional data center, it’s still a type of data center. There’s a lot that bitcoin mining researchers can take from the torrent of data center literature. It’s disappointing and exhausting to see papers published that ignore this reality.

What more can I say other than this shit has to stop. Brandolini’s Law is real. The bullshit asymmetry is real. I really want this new halving cycle to be the one where I no longer have to address bad research. While I was writing this report, Alex de Vries published a new bullshit paper on bitcoin mining’s “water footprint”. I haven’t read it yet. I’m not sure that I will. But if I do, I promise that I will not write over 10,000 words on it. I’ve stated my case and made my peace with this genre of academic publishing. It was a fun ride, but I think it’s time to practice some self-care, treat myself to several evenings of healthy binge-watching, and dream of the ineffable.

—

If you enjoyed this article, please visit btcpolicy.org where you can read the full 10,000-word technical analysis of the Chamanara et al. (2023) study.

This is a guest post by Margot Paez. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.

Source link

Another bitcoin miner, Hut 8 (HUT), has decided to pull the trigger on buying bitcoin in the open market, following the likes of MicroStrategy (MSTR) and MARA Holdings (MARA).

The Miami, Florida-based company said it bought about 990 bitcoin for an average price of $101,710 each. The latest purchase will bring the amount of bitcoin held in Hut 8’s reserve to 10,096, or about $1 billion in market value, and make it among the top 10 largest corporate owners of bitcoin, the company said in a statement on Thursday.

The miner is planning to use the reserve through options strategies, pledges, sales or other strategies, according to the statement. Hut 8’s CEO, Asher Genoot, told CoinDesk that his firm will be opportunistic in buying more bitcoin in the open market.

“Today, the market recognizes and values our strategic reserve, which effectively lowers our cost of capital and strengthens our financial position. As long as this market dynamic persists, we will remain opportunistic in expanding our Bitcoin reserve,” Genoot said.

The move follows Hut 8’s announcement earlier this month that it started a new $500 million at-the-market share issuance program. At the time, the firm said some of the proceeds from the fund would be used to buy bitcoin in the open market, among other things.

MicroStrategy, the largest corporate holder of bitcoin on its balance sheet, started the trend of buying bitcoin in the open market. It wasn’t until MARA Holdings’ purchase of bitcoin in the open market this year that this became prominent among the miners. Most recently, peer Riot Platforms (RIOT) bought 667 bitcoin at an average price of $101,135 on Dec. 16.

Buying large amounts of bitcoin in the open market has paid off for miners opening up new avenues of raising funds at a time when the industry is grappling with a profit squeeze after the recent Bitcoin halving event. Last month, MARA was able to raise $1 billion in convertible debts—a financial instrument where investors can convert debt into equity—with zero interest. This means investors are willing to let go of the interest income from the debt for the equities that provide them with exposure to bitcoin.

Hut 8 said holding bitcoin reserve serves as a flexible option for the firm that can help the company grow. “We view our strategic reserve as a dynamic financial asset that can be actively managed to drive returns well beyond simple price appreciation,” Genoot told CoinDesk.

“Together with the significant investments we are making to expand our core operating business—with a clear path to 24 EH/s of self-mining capacity by Q2 2025—strategic Bitcoin purchases in the open market can strengthen our balance sheet and ability to invest thoughtfully in growth,” he said.

Shares of Hut 8 have risen 74% this year, while CoinShares Valkyrie Bitcoin Miners ETF (WGMI) climbed 28%.

Source link

Company Name: Gridless

Founders: Janet Maingi, Erik Hersman and Philip Walton

Date Founded: August 2022

Location of Headquarters: United States | Operations in Kenya, Malawi and Zambia

Number of Employees: 10

Website: https://gridlesscompute.com/

Public or Private? Private

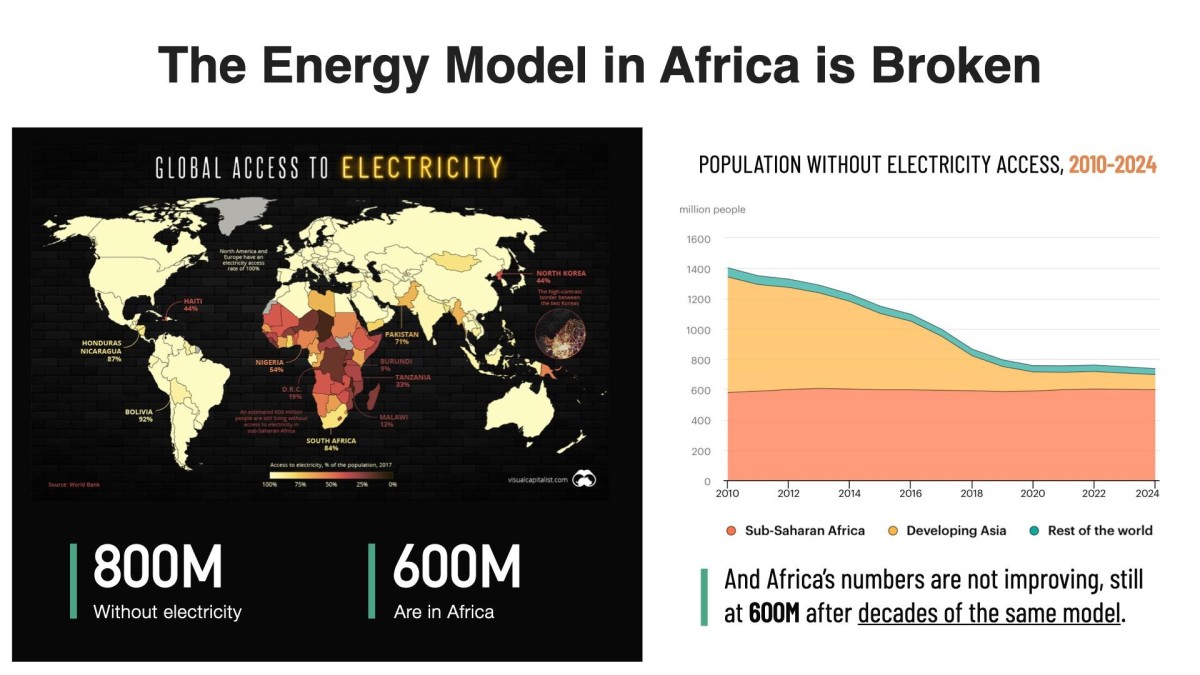

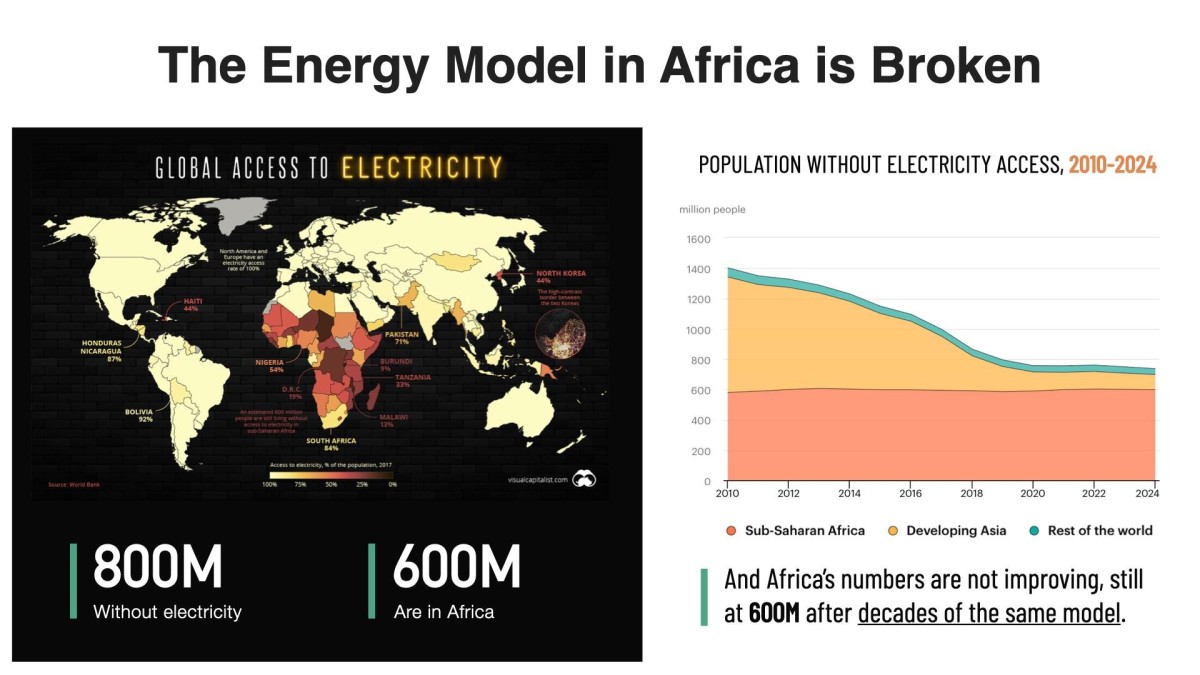

Gridless doesn’t just mine bitcoin — it helps to facilitate the electrification of rural Africa, which is notably improving the lives of those who previously either didn’t have access to power or couldn’t afford it.

Gridless’ co-founder Janet Maingi explained to Bitcoin Magazine how the company’s facilities, which are based in Kenya, Malawi and Zambia, have a win-win-win effect for the company itself, the Bitcoin network and the communities that benefit from Gridless’ operations.

“Our mission is to mine Bitcoin profitably,” Maingi told Bitcoin Magazine. “But as we do this, we also do two other things: we push electrification out to the edge in Africa and we decentralize the Bitcoin network, which has historically been very centralized to North America and China.”

In just over two years, Gridless has set a new standard for the type of impact a Bitcoin mining company can have, showing the world that Bitcoin mining can have a symbiotic relationship with the communities it touches and that it can be a catalyst for human flourishing.

I sat down with Maingi in person in Kenya after this year’s Africa Bitcoin Conference to discuss the work she does and the impact it has on the communities it reaches.

A transcript of our conversation, edited for length and clarity, follows below.

Frank Corva: How does Gridless help to electrify Africa?

Janet Maingi: About 600 million Africans have no access to electricity. That’s about two-thirds of our population. The private sector has stepped in because the main grids do not reach everyone on the continent.

You’ll find that bigger cities like Nairobi or Mombasa have electricity, but if you go to rural Africa, people have no access to electricity because of distribution challenges.

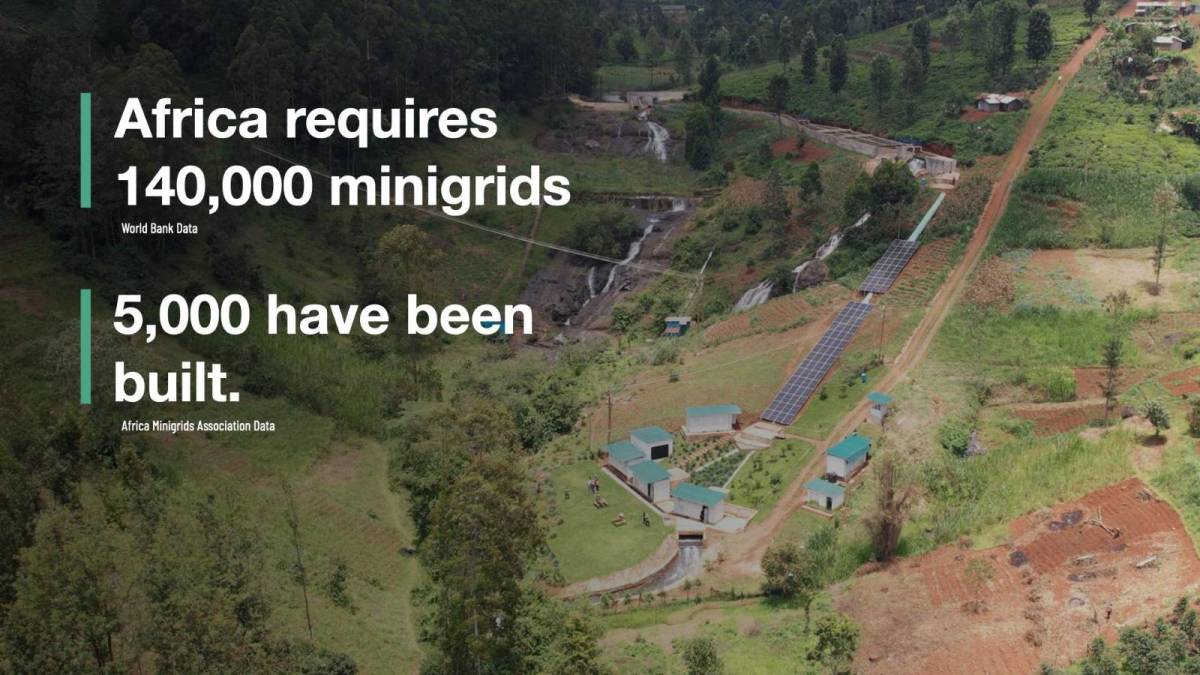

So, the private sector came and started setting up mini-grids. Private companies have done the best they can with these mini-grids. However, they’re very capital intensive, and so there are struggles with fundraising. And even when you actually get them set up, the consumers around your area might not be very wealthy. They’re just living day-to-day. They may have to consider “Do I need electricity or do I need food?”

The companies that construct the mini-grids build power plants that use hydro energy. Let’s say they want to build one that produces one megawatt of energy, but the community only ends up using 200 kilowatts. There’s 800 kilowatts that they generated from the river, but for that 800 kilowatts, they get zero shillings, zero dollars, zero anything.

So, we at Gridless come in and say “That electricity that you’re not able to send to anyone, is what we want.” That’s what you call stranded power or wasted energy, and it’s what we want. So, we become your buyer of last resort.

We come and create an agreement to use that extra electricity, and from a revenue sharing perspective, we work together. It’s a win-win situation. Our data centers use that electricity to mine bitcoin.

But then the catalyzing of electrification comes in. When we’ve used that electricity, it’s become a source of revenue for the energy power plant. They were not making money on that electricity previously, and now they’re profiting from it.

What have we seen as the effect? One, they are able to extend their reach, to distribute electricity further. And secondly, some of them have been able to actually lower their prices. So, consumers who are within their reach but wouldn’t use the electricity because of the cost are suddenly saying, “Hey, hook me up. I can afford to pay for this now.”

Corva: So, in a sense, you’re subsidizing the rate of electricity.

Maingi: Yes, because we come in and use this power, the energy generator is able to give better prices and increase its reach. So, again, what does this mean? More homes getting lit, more small enterprises getting electricity, more factories getting powered and more health centers getting electricity. You can now imagine the upward spiral effect.

However, the challenge is that doing business in Africa is like an extreme sport.

Corva: Why is that?

Maingi: So, let’s start with just getting the equipment. The mining machines come from China, either from Bitmain or MicroBT, or you’ll get them from a company in the U.S., and the process of getting them into Africa can be painful.

We received a batch that came from the U.S. and it took us 60 something days just to get them into the country. This is from putting them on a ship to getting them here. This doesn’t include figuring out the logistics around getting the miners on site and going through pre-shipment inspection to make sure that they meet the Kenyan standards.

It’s a process that takes almost 120 days from start to end. If you’re running a business, and it takes you 120 days to get your product on the ground, it’s painful.

Secondly, these machines are designed to work very well in China or the U.S.

Conditions in Africa are different, though.

Corva: Does this have anything to do with air quality?

Maingi: Air quality, dust, heat. In Kenya, average temperatures range from 20 to 40 degrees Celsius. So, when you power those machines in an environment where the average temperature is 30 degrees Celsius, you can imagine the heat that they have to deal with.

And then there’s dust. When you get a pre-fitted container from China or somewhere, you discover that the designers just focus on inflow and outflow. But we realized we have issues with dust, so we have to put dust filters on the machines.

And then, in 2022, we learned when we set up the first site that, because of the lights on the miners, they attracted bugs. During the rainy season, the bugs could see the lights and flew into the fans and got mashed up — something nobody thought about.

Lastly, the containers initially were going to cost us $100,000 each, which was too much for us to be profitable. The math didn’t math, as we say. So, we sat down and designed our own container.

Corva: Amazing.

Maingi: Right? And that’s what we’ve been deploying at a quarter of the price. And then the advantage that came with being made in Kenya has allowed us to get passage through the COMESA (Common Market for Eastern and Southern Africa) region, without having to pay extra duties or taxes because it’s recognized as a COMESA product.

That also helped because, being made in Kenya, it’s very easy for us to move the containers around the COMESA region without having to pay extra taxes. We get a tax exemption. Even if the containers from China made sense, if we brought them to Kenya and I had to move them to Uganda, I would have to pay taxes to Uganda, too.

Any country you move foreign products to, you have to pay taxes again. So, it’s been hard, but good solutions have come out of the difficulties.

Have you heard of GAMA, the Green Africa Mining Alliance?

Corva: Yes.

Maingi: During the first Africa Bitcoin Mining Summit last year, we released a blueprint of the container we designed. So, anyone who wants to use it to build their own container using our blueprint can feel free to do so.

Where you need our support, we’ll be ready to guide you. That’s the whole thing about GAMA — How do we exploit our synergies? How do we benefit from one another? How do we find a young lady who wants to start mining and walk her through the journey of getting started?

Corva: Incredible. I want to go back to electrification in Africa. You mentioned earlier that you wanted to share some numbers.

Maingi: What I was saying is that there’s a ripple effect when we partner with the energy generator. We’ve been able to see more homes or households getting connections.

If you’ve been in rural Kenya or Africa, then you understand how one bulb can transform a life. I’ll use the example of children coming home from school. They have assignments and use these tiny paraffin lamps to study. The fumes from them are horrible for their health. But this is a child for whom there’s no plan B. The teacher expects this child to come back to school with her assignments completed. Not having electricity is not an excuse.

A guy once told me that sometimes, when his daughter is busy doing an assignment, the paraffin runs out. When the nearest gas station is almost four miles away, who is going to go and look for paraffin at that time? Nobody. Tough luck.

So, the child gets to school and is either in trouble because she didn’t do her assignments or is now lagging behind because now those quote unquote “are yout personal problems.” Because of that one bulb they now have, he was like, “My daughter is performing so well in school.” Then, health wise, all these visits they used to make to the hospital because she was breathing in the paraffin fumes no longer happen.

Corva: It seems you want to make my cry.

Maingi: No, there’s no crying. (Author’s note: This woman doesn’t play.) It’s a reality.

Then, in Zambia, I remember talking to women who were talking about childhood vaccinations. Between zero and three years, there are certain vaccinations recommended by the WHO that your kid needs to get — measles, polio, etc. — but the nearest health center that has them sometimes isn’t close.

So, you do your math, and you’re like, “I can’t afford bus fare to do this.” And so this disease sounds more serious, I’ll get my child the vaccination for that one, while this one I’ll pass on. But really all of them are important for children.

Now, Gridless is coming into Malawi and getting electricity providers to connect more homes in the Bondo area. Health centers are getting powered on, so more vaccines are available in more local health centers.

While before you used to say “Polio sounds serious, I’ll get my child that vaccine, but with measles, I don’t know who has died of that recently, so maybe, I won’t get my child that one,” now more people can get it.

Now, we will have a young generation who, we believe, as we keep doing this, is going to thrive. They’re going to grow. You’ll possibly get rid of childhood mortalities because these rural areas get electrified.

Corva: And bringing energy to these regions also helps support livelihoods I assume.

Maingi: Yes, of course. There’s a tea factory in Muranga, Kenya, which is in the highlands.

We partnered with the energy generator in the area and they were able to give the factory power. Now, their facilities are able to support the tea factory, which has two benefits: tea farmers can bring their tea to the factory, which means it doesn’t spoil on the farms because they can’t get it to point B in time and more employment has also been created just by that tea factory becoming an electrified space.

We keep saying why we know this will make a difference is because energy is a base of human progress.

Corva: There’s no such thing as an energy poor country that’s rich.

Maingi: If you look at the Maslow’s hierarchy of needs, it used to go food, shelter, clothing, but I put energy there. Energy is a basic need. It’s a must have for anybody to actually be allowed to live a decent life. For people to make a decent living, energy has to be in that math.

Corva: Is it true that you’ve recently created software that helps with energy demand response?

Maingi: Yes. We realized that we need to get more proactive in creating real-time demand response. Before, we were either reacting too late or too early to the power available.

Remember we’re the buyer of last resort, so communities come first and small businesses come second. For us to be able to live up to that promise, we had to make sure we weren’t sucking in electricity that was required by somebody else at that time.

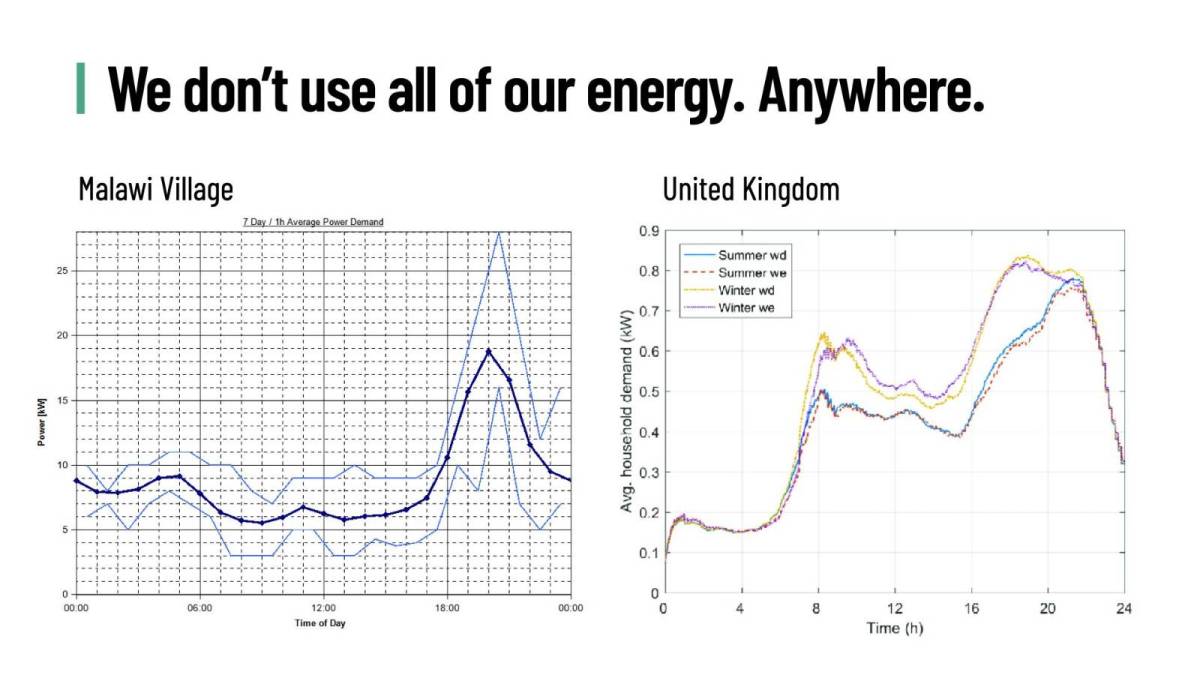

So, let me paint a picture. In normal households, people wake up at 6 a.m., so there’s a surge of electricity. At that stage, our software gets a signal and reduces our consumption to meet the demand needed by the grid. Then, at 8 a.m., everybody goes to school and switches off their lights and there’s too much electricity in the grid. That’s when we power more mining machines.

We get the signal, power more machines, suck in the electricity and keep on going until maybe 6 p.m. when people have gotten back home and they need the electricity. Gridless turns down their machines and returns the electricity.

At 10 p.m. they all go to bed, and we power up more machines. This is all done with software we developed internally called Gridless OS. It allows for real-time demand response. It makes it so everybody gets what they need, and it stabilizes the grid.

Corva: Are you setting certain standards with Gridless that others are following in Africa or in other parts of the world?

Maingi: It’s set a trend that people are following. Sometimes you go to conferences and people keep referring to Gridless. That’s when you realize, “My God, this thing is bigger than we thought.” And so you start to understand how this has made a difference, that it doesn’t exist in a vacuum.

At the end of the day, everyone has different ways of mining bitcoin, and there’s a positive impact to the community whichever way you do it. Look at Bigblock Datacenter — Sebastian Gouspillou in the Congo — where they’re using the heat to dry cocoa for chocolate they sell. Think of what that has created for that economy.

Corva: I think Sebastian brought me to tears when I met him, too.

Maingi: What’s exciting for us and other players within this space is that we are the ones who understand our problems, and it’s exciting to see African companies deciding “Not only will I mine bitcoin profitably and decentralize the network, but there’ll be some benefit to our community, as well.”

Source link

Bitcoin mining and tech firm Cleanspark has announced its intention to raise $550 million in Convertible Senior Notes offering. As the firm revealed, it is pricing the notes at 0% and will only make it available to qualified investors. Cleanspark said the convertible notes will mature in 2030.

Cleanspark Plans Exclude Bitcoin

The update from the firm shows its plans to offer the notes to the initial purchasers for resale in a private offering as securities. The firm said it will cap the initial price of the notes at $24.66 per share of the company’s common stock. Per the filing, this amount represents 100% premium to the closing price of the stock as of December 12, 2024.

As an added allowance, Cleanspark hinted that it can allow up to a 13-day option to repurchase up to $100 million aggregate principal amount of the notes. If investors exercise this extended repurchase option, the Bitcoin mining firm can raise up to $633.6 million.

While fundraise via convertible notes is not uncommon among US firms, the purpose of this funding is different. Despite being a Bitcoin mining firm, Cleanspark will not use the capital to buy additional BTC. Instead, it said it will designate $145 million to repurchase shares from investors who participate in the notes sales.

In addition, Cleanspark said it will deploy some of the funds to settle its line of credit with Coinbase exchange. The remaining capital will go into capital expenditures, acquisitions and general corporate purposes.

The Unusual Twist With Bitcoin Mining Firms

Unlike Cleanspark, other Bitcoin mining firms like Riot Platforms have raised funds by issuing convertible senior notes. However, unlike the former, Riot Platforms used the proceeds to buy 5,113 Bitcoin for $510 million earlier on December 13.

MARA Holdings have also made this move in the past, solidifying the thesis that Bitcoin miners are increasingly adopting BTC beyond the daily mining operations.

These firms are learning from the MicroStrategy Bitcoin playbook. As reported earlier, MicroStrategy has grown its BTC stash to 423,650 units after its latest 21,550 Bitcoin purchase for $2.1 billion. The goal for this firms is that the price of the coin will continue to appreciate against the US Dollar.

With its treasury reserve success, MicroStrategy is now on track for Nasdaq-100 Index inclusion. Why Cleanspark refused to allocate any amount to Bitcoin remain a puzzle in the broader ecosystem.

Godfrey Benjamin

Benjamin Godfrey is a blockchain enthusiast and journalists who relish writing about the real life applications of blockchain technology and innovations to drive general acceptance and worldwide integration of the emerging technology. His desires to educate people about cryptocurrencies inspires his contributions to renowned blockchain based media and sites. Benjamin Godfrey is a lover of sports and agriculture.

Disclaimer: The presented content may include the personal opinion of the author and is subject to market condition. Do your market research before investing in cryptocurrencies. The author or the publication does not hold any responsibility for your personal financial loss.

Source link

Metaplanet makes largest Bitcoin bet, acquires nearly 620 BTC

Tron’s Justin Sun Offloads 50% ETH Holdings, Ethereum Price Crash Imminent?

Investors bet on this $0.0013 token destined to leave Cardano and Shiba Inu behind

End of Altcoin Season? Glassnode Co-Founders Warn Alts in Danger of Lagging Behind After Last Week’s Correction

Can Pi Network Price Triple Before 2024 Ends?

XRP’s $5, $10 goals are trending, but this altcoin with 7,400% potential takes the spotlight

CryptoQuant Hails Binance Reserve Amid High Leverage Trading

Trump Picks Bo Hines to Lead Presidential Crypto Council

The introduction of Hydra could see Cardano surpass Ethereum with 100,000 TPS

Top 4 Altcoins to Hold Before 2025 Alt Season

DeFi Protocol Usual’s Surge Catapults Hashnote’s Tokenized Treasury Over BlackRock’s BUIDL

DOGE & SHIB holders embrace Lightchain AI for its growth and unique sports-crypto vision

Will Shiba Inu Price Hold Critical Support Amid Market Volatility?

Chainlink price double bottoms as whales accumulate

Ethereum Accumulation Address Holdings Surge By 60% In Five Months – Details

182267361726451435

Why Did Trump Change His Mind on Bitcoin?

Top Crypto News Headlines of The Week

New U.S. president must bring clarity to crypto regulation, analyst says

Will XRP Price Defend $0.5 Support If SEC Decides to Appeal?

Bitcoin Open-Source Development Takes The Stage In Nashville

Ethereum, Solana touch key levels as Bitcoin spikes

Bitcoin 20% Surge In 3 Weeks Teases Record-Breaking Potential

Ethereum Crash A Buying Opportunity? This Whale Thinks So

Shiba Inu Price Slips 4% as 3500% Burn Rate Surge Fails to Halt Correction

Washington financial watchdog warns of scam involving fake crypto ‘professors’

‘Hamster Kombat’ Airdrop Delayed as Pre-Market Trading for Telegram Game Expands

Citigroup Executive Steps Down To Explore Crypto

Mostbet Güvenilir Mi – Casino Bonus 2024

NoOnes Bitcoin Philosophy: Everyone Eats

3 months ago

3 months ago182267361726451435

Donald Trump5 months ago

Donald Trump5 months agoWhy Did Trump Change His Mind on Bitcoin?

24/7 Cryptocurrency News4 months ago

24/7 Cryptocurrency News4 months agoTop Crypto News Headlines of The Week

News4 months ago

News4 months agoNew U.S. president must bring clarity to crypto regulation, analyst says

Price analysis4 months ago

Price analysis4 months agoWill XRP Price Defend $0.5 Support If SEC Decides to Appeal?

Opinion5 months ago

Opinion5 months agoBitcoin Open-Source Development Takes The Stage In Nashville

Bitcoin5 months ago

Bitcoin5 months agoEthereum, Solana touch key levels as Bitcoin spikes

Bitcoin5 months ago

Bitcoin5 months agoBitcoin 20% Surge In 3 Weeks Teases Record-Breaking Potential

✓ Share: