Blockchain

Central Bank Digital Currency on Corda - An Ultimate Guide

Central bank digital currencies (CBDC) is a tangible use case for distributed ledgers, already being implemented and explored by many of the largest nations. COVID-19 has accelerated the shift to a digital first mindset. Our increased time at home and online has brought into focus the efficiency potential and opportunities presented by digital and programmable money, as cash use has continued to decline.

Distributed ledger technology is one of the key technologies being evaluated by global central banks to pave the way for the next phase of the digital economy and to accommodate the needs of the modern financial world.

CBDCs present a way for banks and traditional financial services providers to achieve true digitalization. The rise in fintech and open banking has driven greater collaboration and competition across financial services. CBDCs extend the safest form of money available to banks, businesses and the public – central bank money – via new digital rails to further increase the potential for innovation.

As per a report by Coindesk, as many as 80% of central banks are considering a central bank digital currency while 40% are already in a proof-of-concept stage including China, Japan, Australia, and Singapore.

Enroll Now: Beginner’s Guide to Corda Development Course

What are CBDCs?

A CBDC is a digital payment instrument and store of value issued by, and as a liability of, a central bank or monetary authority. The main difference between a CBDC and other digital currencies is that it is denominated in the national unit of account of the central bank’s country or currency zone. CBDC, issued on distributed ledger and digital asset management infrastructure like Corda allows the digital financial system to stay in sync, with the appropriate identity, transaction privacy, resilience and governance controls required.

In other words, contrary to the existing process of printing money, CBDCs are a way of issuing digital tokens that represent fiat currency and provide a payment instrument for retail and wholesale banking. Just like money, CBDCs would be supplied, regulated and controlled by the central bank, making them very different from other cryptocurrencies, or even stablecoins.

Must Read: Advantages Of Central Bank Digital Currencies (CBDCs)

CBDCs and R3’s Corda

The Corda blockchain platform is one of the few being used extensively by global central banks, financial market infrastructure providers, and commercial banks for the exploration and implementation of CBDC projects.

Corda and R3’s ecosystem of global banks provide a ready-made network to integrate programmable money that can interoperate with currencies across different central banks’ networks. This allows central banks to tap into the global market and provide new services to both financial institutions and/or the general public. Compared to other blockchain networks, Corda enables much faster transaction processing, provides regulators the ability to trace transactions, and also preserves privacy by facilitating transactions in a point to point manner.

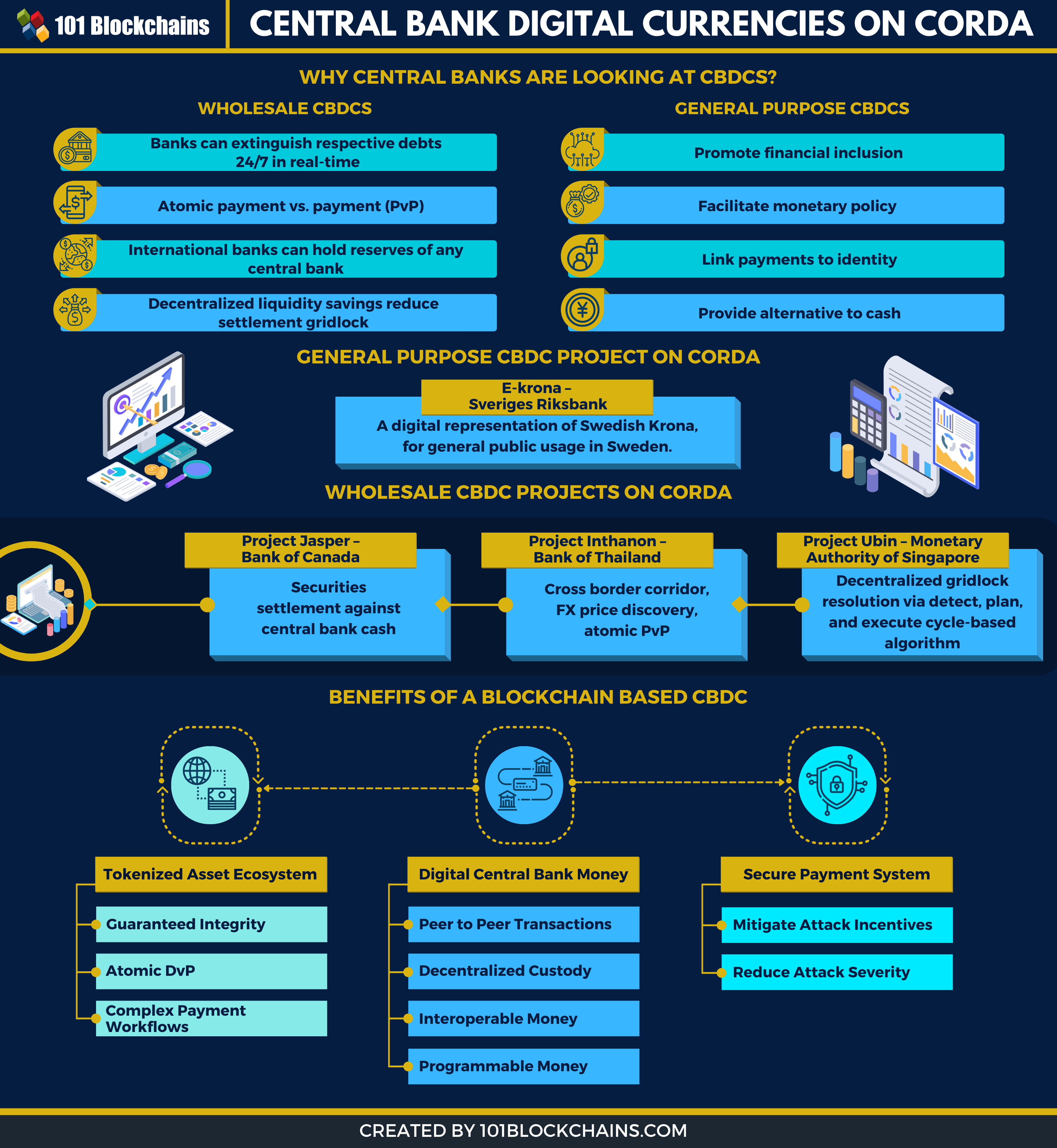

To know more about Central Bank Digital Currency on Corda, check out the detailed graphic here-

Please include attribution to 101blockchains.com with this graphic. <a href="https://101blockchains.com/wp-content/uploads/2021/07/Central-Bank-Digital-Currencies-on-Corda-v3.png" border="0" /> </a>

Learn the concepts of Corda blockchain with the Corda flashcards!

Mentioned below are some other factors why Corda’s core design is suitable for building CBDCs and regulated financial markets:

1. Data privacy

Being a permissioned blockchain with a peer-to-peer architecture, Corda ensures transactional data is only shared among concerned parties on a need-to-know basis – rather than distributing it over the whole network. Therefore, it allows control over data privacy while maintaining the necessary transparency and trust between counterparties.

2. Strong identity model

Corda’s identity model ensures that participants are represented as legal entities and managed consistently. Therefore, the intrinsic characteristics of Corda make it a perfect fit for CBDC implementations as a robust approach to identity brings trust and security to the network.

3. Scalability

The peer-to-peer architecture, scalable consensus model, workflows that can run in parallel, and other enterprise grade optimizations ensure that Corda can achieve unparalleled scalability. For example transaction validation is completed by notaries, and multiple notaries can be added to a network to increase throughput and reduce latency.

In addition to its core features, R3 has invested development work in the CBDC space,

launching its Digital Currency Sandbox following a year-long working group with over 140 central banks, FMIs, commercial banks, and service providers. The working group output provided reference models for retail and wholesale CBDCs, and a CBDC taxonomy to drive standardization in the way the ecosystem talks about CBDC. These learnings are now translated into the sandbox which enables central banks, commercial banks, exchanges, payment providers, and more to dive deep into the technology supporting a CBDC and develop strategies and applications for engaging alongside an emerging ‘ready-made payments ecosystem’.

Along with the rest of the sandbox ecosystem, users can simulate the issuance of a digital currency with demos and documentation. Participants will also learn how each transaction works on Corda, the only Distributed Ledger Technology (DLT) platform built specifically for highly regulated industries.

Preparing for Corda interview? Here we bring the expert guide that will cover the top corda blockchain interview questions for your preparation!

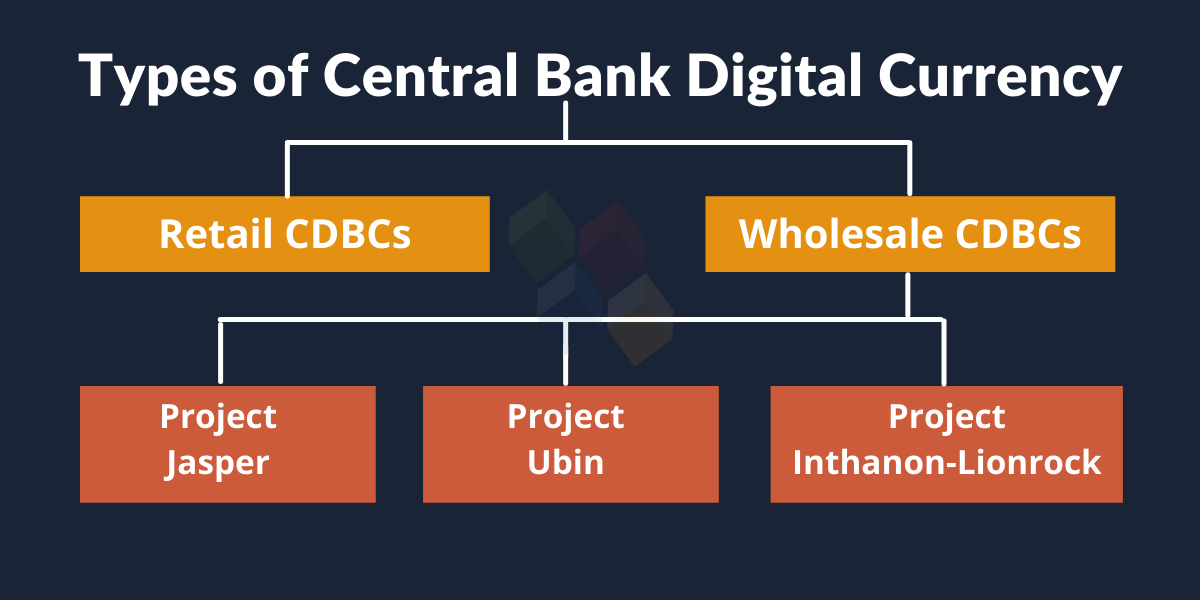

Types of CBDCs

1. Retail CBDC

Retail CBDCs, or general purpose CBDC issued to the general public represent the harder of the primary use cases for CBDC with many open conceptual questions about their potential design and implementation. While no production use cases yet exist, central banks are committing increasing resources to these projects. Central banks’ motivations include promoting financial inclusion, facilitating monetary policy, enabling participation in a tokenized financial ecosystem, fostering competition, providing a cash alternative, or generally modernizing payments.

A prominent example of Retail CBDC on Corda is the project by Riksbank. Riksbank identified the opportunity to provide the ‘e-Krona’ and started exploring the possibility of issuing a CBDC, using blockchain technology. On April 15, 2021, the Swedish bank governor revealed the target of having an operational digital currency in five years.

The project has already run in a testing environment where users were allowed to hold e-kronor for performing financial activities such as deposits, withdrawals, and making payments through a mobile app. Other possibilities are the use of smartwatches and other smart wearables for making payments using e-kronor.

2. Wholesale CDBCs

Wholesale CBDCs are primarily used to establish a seamless digital payment ecosystem between banks. Using wholesale CBDCs, banks can protect themselves from the build-up of credit risk through a real-time settlement process controlled by code. The transfers happening between banks in this scenario are “atomic” with the transfer of value represented by the exchange of tokenized CBDCs between parties made directly and without intermediaries.

Enroll Now: Central Bank Digital Currency (CBDC) Masterclass

As a result, there are a number of wholesale CBDC projects that have explored R3’s distributed ledger technology. A few of them are mentioned below:

The Bank of Canada started exploring the possibility of a Central bank Digital Currency which led to the initiation of project Jasper on R3’s Corda DLT platform. The project was released in three phases to understand its usefulness in the interbank settlement process and was marked as one of the most successful initiatives by the Bank of Canada.

From March of 2016 to June of 2016, the first phase of project Jasper was carried out. Phase 1 was focused on the storing and transferring of central bank-issued digital receipts on a distributed ledger providing security and auditability.

Phase 2 started in May of 2017 where the project was built on R3’s Corda introducing a liquidity savings mechanism for frictionless settlement between the banks.

Finally, phase 3 was initiated in October of 2017 after recognizing the powers of a DLT-based CBDC system along with the liquidity savings mechanism as well as atomic “Delivery vs Payment” transactions. This phase marked the development of a proof of concept for the project.

The Monetary Authority of Singapore (MAS) was not far behind in exploring the powers of distributed ledger for their financial ecosystem. The MAS initiated project Ubin in two phases.

Phase 1 was started in November 2016 which was successful in creating an efficient digital payment structure for interbank settlement using the digital representation of the Singapore dollar.

Phase 2 of Ubin started in June 2017 to explore different DLT platforms including R3’s Corda for the primary purpose of implementing a decentralized real-time gross settlement (RTGS) system along with Liquidity savings mechanisms.

- Project Inthanon-Lionrock

Started in March of 2017, LionRock on Corda explored the possibility of building an interbank settlement system including securities issuance, lifecycle, and delivery-vs-payment.

The project is a joint initiative by the Hong Kong Monetary Authority (HKMA) and the Bank of Thailand (BOT) to explore the possibility of CBDCs.

More recently, notable projects using Corda and partnering with R3 also include Project Helvetia run by the BIS Innovation Hub, SIX Group AG, and the Swiss National Bank and Project Jura.

Also Check: Top 10 Corda Use Cases You Should Know About

Benefits of CBDCs

In general, CBDCs have the following benefits:

- Transactions can be peer to peer, allowing for individual participants to custody their own money or assets, or hold accounts direct with central banks

- The underlying technology of blockchain ensures global integrity of the system in which CBDC exists

- Overall system risk has the potential to be greatly reduced with CBDCs

- Increased availability and accessibility due to the possibility of using mobile devices for digital transfer of value

- Cross-border payments using CBDCs can be completed in seconds and at a very low transaction fee as compared to the existing system

- They allow more control over money supply and new tools for the implementation of monetary policy

- Efficient tax control and tracking of payments is another benefit.

Specific to R3’s Corda, building CBDCs have numerous benefits aligned with the Corda features as listed below:

- Corda facilitates unparalleled data privacy which becomes a crucial factor for digital settlements

- Strong identity management on Corda allows a streamlined payment ecosystem in the digital space

- The scalability offered by Corda is a perfect fit for CBDC applications.

- Transactions and settlements are deterministic and validated by notaries rather than using a probabilistic approach.

Want to know more about Corda? Enroll now in Beginner’s Guide to Corda Development Course and learn the basic and advanced concepts of Corda.

About Author

![]()

101 Blockchains is the world’s leading online independent research-based network for Enterprise Blockchain Practitioners. Subscribe 101 Blockchains to get all the latest news about blockchain.

Source link

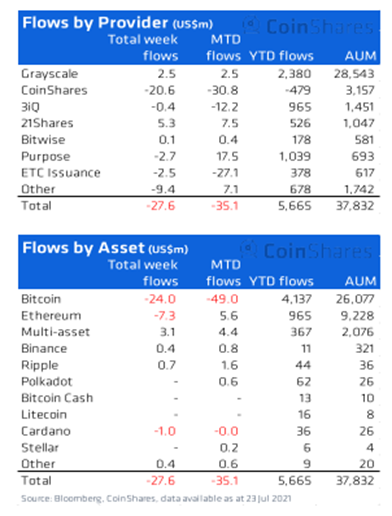

The price of Bitcoin slightly rebounded, which has increased by 24.15% over the past week, according to Coinmarketcap.

During the intraday, Bitcoin was trading at $36,954. The crypto market leader with a market cap of $691,522,863,909. On Monday, the price of Bitcoin surpassed the psychological barrier of $40K for the first time since June 16.

But despite the rebound in bitcoin prices, institutional investors seem to lack interest, with the institutional sentiment remains bearish.

Analysis company CoinShares released a report entitled “Digital Asset Fund Flows Weekly” on Monday, July 26. The report indicates the net outflow of digital asset investment products has reached $28 million, which is the third consecutive week of outflow of funds.

And the withdrawal of funds comes from Bitcoin. 85% of the total outflow amounting to 24 million funds were drawn from Bitcoin, a virtual currency investment asset, which is the biggest outflow since mid-June.

Coinshares stated that most of the funds showed varying degrees of outflow from Bitcoin and Ethereum. Ethereum also flowed out $7.3 million within a week, while multi-asset funds bucked the trend, with a total net inflow of $3.1 million, stating that:

“Last week’s outflows suggest negative sentiment still pervades the asset class despite more recent constructive comments from key industry players.”

Meanwhile, altcoins’ inflows such as Binance’s BNB token and ripple(XRP) were $0.4 million and $0.7 million, respectively.

Image source: Shutterstock

Source link

Aspiring to know about the Core Features of central bank digital currency? If yes, you have reached the right place.

Central banks have been the most trusted source of money for the public for many years in accordance with their public policy objectives. However, the world has been changing considerably, and the domain of finance is not new to the scope for change. From a commercial perspective, digital payments have become faster and more convenient, especially with growing volumes and diversity.

Now, central banks are seeking out alternatives to offer digital currency to the public in the form of a ‘general purpose’ central bank digital currency. CBDC features have started to gain profound levels of attention in recent times. So, what do CBDCs or central bank digital currencies have to offer for changing the face of financial services as we know them?

Enroll Now: Central Bank Digital Currency (CBDC) Masterclass

What are CBDCs?

Before diving into an outline of central bank digital currency features, it is important to understand their definition. CBDC basically points out any digital variant of central bank money, which is different from the balances in traditional reserves or settlement accounts. The interest in CBDC has been growing substantially in recent times as central banks carry out research and experiments.

In addition, continuing private experiments with different types of digital money alongside conceptual variety delivered by new technologies could imply confusion in defining CBDCs. The easiest definition of CBDC suggests that it is a digital payment instrument with denominations in a national unit of account. Most important of all, it is a direct liability of the central bank.

In order to understand the features of CBDC, you should know that central banks offer two distinct types of money. Central banks also offer the necessary infrastructure for supporting the third type of money, i.e. private money. Physical cash is the first type of money that is commonly accessible and is peer-to-peer in nature.

The second type of money refers to electronic central bank deposits, also referred to as settlement balances or reserves. The central bank reserves are generally electronic in nature, and only eligible financial institutions could access them. CBDCs give way for a new type of money. In the new system, CBDC would entail the requirements of a central bank, operators alongside the participating payment service providers and banks.

Foundational Principles of CBDC

The understanding of features of central bank digital currencies also depends a lot on the founding principles of CBDCs. Different types of motivations drive the ongoing research with respect to CBDCs. However, central banks follow common policy objectives, thereby calling for agreement on common principles.

The common foundational principles for CBDC are essential for incorporating the core features in central bank digital currencies and the underlying system. Here is an outline of the foundational principles for CBDCs, which can offer an in-depth understanding of CBDC features.

The first founding principle for CBDCs basically points out not doing any type of harm. Actually, the new variants of money supplied by the central bank should continue their support for fulfilling public policy objectives. Most important of all, the new form of money should not affect or intervene with the ability of a central bank to carry out necessary tasks for financial and monetary stability.

Another founding principle which forms the basis of features of central bank digital currencies refers to coexistence. Central banks have prioritized stability above everything else and move with caution in the new domain of CBDCs. Coexistence actually refers to the need for new and existing types of central bank money to complement each other. All the forms of central bank money should coexist for supporting public policy objectives. Furthermore, central banks must continue offering and supporting cash alongside the adequate public demand for cash.

-

Innovation and Efficiency

The final founding principle for CBDC refers to innovation and efficiency. Both elements are essential to keep users away from less safe financial instruments. Subsequently, the damage to monetary and financial stability with economic and consumer harm could follow. The existing payments ecosystem includes public authorities as well as private agents. With new ways for both of them to work together, CBDCs can definitely serve as a secure, efficient, and highly accessible system.

Curious to know the difference between crypto and CBDC? Here’s a guide to help you understand the differences of Crypto vs CBDC.

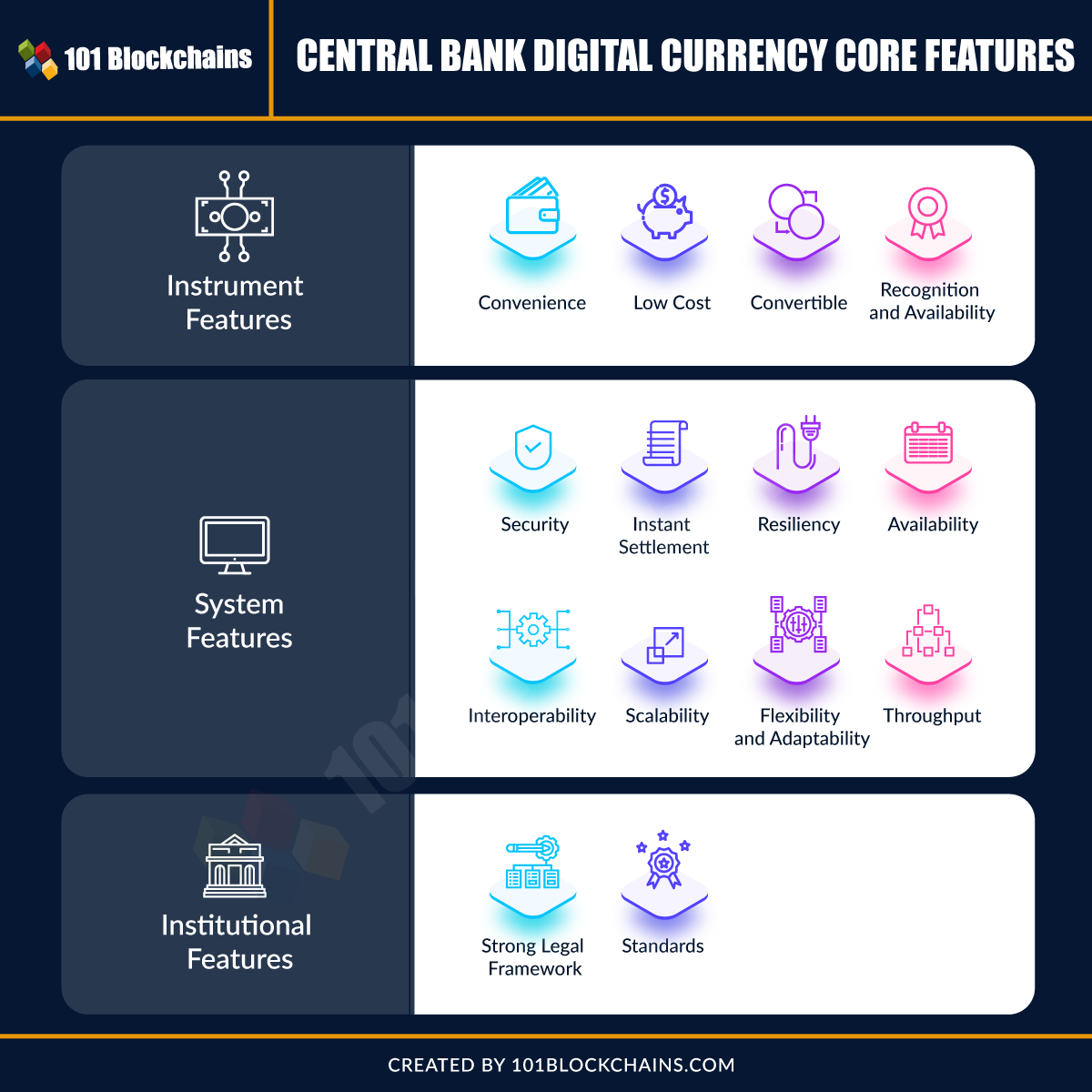

Understanding Central Bank Digital Currency Core Features

Please include attribution to 101blockchains.com with this graphic. <a href="https://101blockchains.com/blockchain-infographics/"> <img src="https://101blockchains.com/wp-content/uploads/2021/07/CENTRAL-BANK-DIGITAL-CURRENCY-CORE-FEATURES.png" alt="CBDC Core Features="0' /> </a>

The role of central bank digital currency features is clearly evident in the fact that they help in addressing the foundational principles. A new CBDC solution would need the core features with a specific focus on the instrument itself, the associated system and the wider institutional framework. So, one could find instrument features, system features as well as institutional features among the core features outlined for CBDC. Let us find out more about the features in each category.

Instrument Features

The first addition among core CBDC features would deal with the features that are specific to the CBDC instrument itself. Some of the core instrument features you can find in CBDC are as follows,

CBDC payments should be highly convenient and as simple as using cash, scanning a QR code or swiping a card. With convenient payments, CBDCs could encourage accessibility and adoption.

Another critical entry among central bank digital currency features refers to the availability of CBDC payments at extremely low or zero costs for end-users. In addition, CBDC must also ensure the limited requirement of technological investment for end-users.

CBDC should be easily exchangeable at par with private money or cash for maintaining the uniqueness of currency.

-

Recognition and Availability

CBDC should be applicable in all types of transactions that use cash, such as person-to-person or point-of-sale transactions. Furthermore, CBDC should also offer the ability for making offline transactions, generally for limited periods and with predefined thresholds.

Watch on-demand virtual conference on Digital Assets and Central Bank Digital Currencies (CBDCs) now!

System Features

The system features are particularly associated with the CBDC system or the platform hosting the solution. The important system features of CBDC are as follows,

The infrastructure, as well as participants in a CBDC system, should maintain formidable levels of resistance to cyber attacks as well as other threats. CBDC should ensure effective safeguards against counterfeiting.

CBDC should facilitate instant or near-real-time settlement for all end-users of the system.

Features of central bank digital currencies should also include the facility of higher resilience towards operational failure and disruption due to electrical outages, natural disasters, or other possible reasons. In addition, end-users should also have the ability for making offline payments when network connections are not available.

End-users of the CBDC system should have the ability to make payments 24 hours a day, seven days a week, and 365 days a year.

The system should have the capability to deliver adequate interaction mechanisms alongside private sector digital payment systems and arrangements to simplify the transfer of funds among systems.

The features of CBDC system should have the ability for expanding to address the need for potentially large volumes in the future.

-

Flexibility and Adaptability

You should also look for flexibility and adaptability in a CBDC system to ensure that it fits well with changing conditions alongside policy imperatives.

The CBDC system must have the capability for processing a considerably large number of transactions.

With so much hype about CBDC all around, are you wondering about the advantages of CBDC? Check this guide to learn the top advantages of central bank digital currency.

Institutional Features

The final set of features of central bank digital currencies refers to the institutional features. Institutional features actually refer to the overall environment in which CBDCs have to operate. The notable institutional features pertaining to CBDC are as follows,

Central bank should impose clear precedents and guidelines for exercising its authority in the process of issuing a CBDC.

The CBDC system, including the infrastructure and all the participating entities, must comply with all the relevant regulatory standards. For example, entities responsible for transferring, storing or maintaining custody of CBDC must have accountability to regulatory and prudential standards followed by firms offering the same services for cash or digital money.

Here’s a guide to help you understand the differences between Retail vs Wholesale CBDC?

Opportunities and Risks of CBDC

The understanding of CBDC features gives a comprehensive impression of their potential. At the same time, it also gives the foundation for determining the opportunities and risks associated with CBDC. First of all, CBDC could enable opportunities that are unlikely with cash. With the help of an accessible and convenient CBDC, users can have an alternative to possibly unsafe variants of private money.

In addition, it ensures user privacy while enabling fiscal transfers and reducing illegal activity. On the other hand, the introduction of CBDC could also present some implications for financial stability. For example, the possibility for digital bank runs during times of stress or the long-term consequences associated with bank funding.

New to the Blockchain? Get started with the Free Enterprise Blockchains Fundamentals course!

Bottom Line

Central bank digital currencies or CBDCs have the capability to serve an important role in helping central banks. CBDCs can change the ways of addressing public policy objectives of central banks. At the same time, they also help in facilitating evolution to the next step of digitalization in daily lives. The attention of the core features of CBDC focuses on strengthening usability while also safeguarding monetary and regulatory stability.

Simultaneously, it is also important to maintain a clear emphasis on design and technology trade-offs for security or offline transactions. Other important trade-offs you must consider are related to privacy or compliance and programmability or performance. The research on CBDC and its relevant features would continue, especially with collaborative efforts from renowned industry players. Learn more about CBDCs and their implications with the CBDC course for the broader financial landscape!

About Author

Software evangelist for blockchain technologies; reducing friction in online transactions, bridging gaps between marketing, sales and customer success. Over 20 years experience in SaaS business development and digital marketing.

Source link

Bitcoin surpassed above 40K before falling back to stand above the $36.8K level. The breakthrough was partly boosted by e-commerce giant Amazon Inc hinting that it would allow its users to pay for products using cryptocurrencies before the company denying it. Meanwhile, the platform still intends to hire blockchain and digital currency expert talent to manage and develop its crypto payment system.

BTC has surpassed the $40K level, touching the high of $40,499 level over the past 24 hours before falling back and standing above the $36.8K level, according to CoinMarkCap.

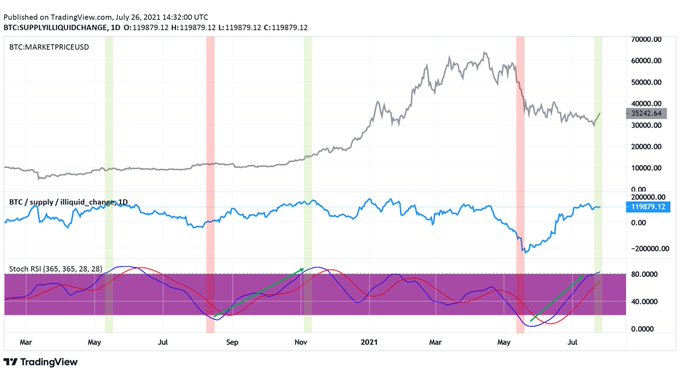

On-chain analyst Will Clemente believes that BTC’s supply squeeze is just getting started. He explained:

“Illiquid Supply RSI has flashed the first buy signal since November of last year. The supply squeeze is just getting started. This looks at the broader trend change in accumulation behavior by running a 365-day stoch RSI over the 30-day net change of illiquid supply.”

Crypto analytic firm Dilution-proof recently pointed out that bulls had created a great setup for a short-squeeze based on Bitcoin’s $3k intraday move despite futures markets remaining short. A short-squeeze usually prompts rapidly rising prices in tradable assets.

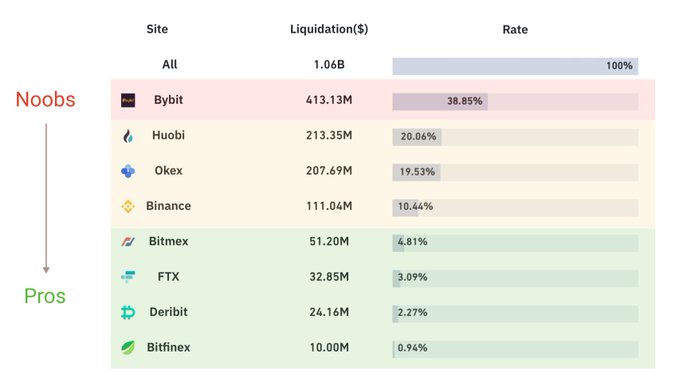

$1 billion BTC futures liquidated

According to market analyst Willy Woo:

“$1b of BTC futures liquidations in the last 12 hours.”

The upward momentum in the BTC market caused some traders to be caught in a massive liquidation. As a result, total liquidations in the cryptocurrency ecosystem topped $1 billion.

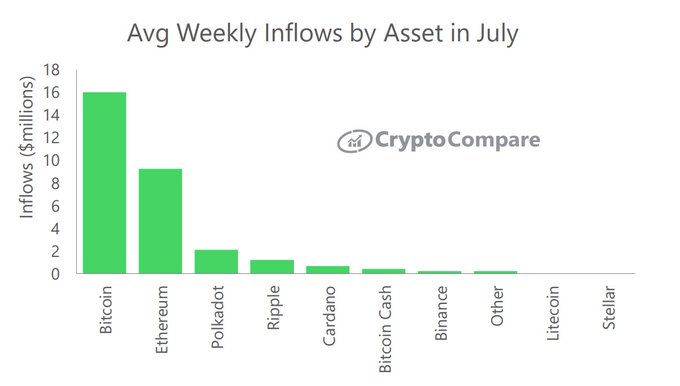

Meanwhile, average weekly inflows into Bitcoin hit $16 million, as acknowledged by CryptoCompare. The on-chain data provider noted:

“Average weekly inflows were positive in July - increasing from an average of -$59.5m in June to $58.5m. Weekly inflows into Bitcoin-based products averaged $16.0m. This was followed by Ethereum-based products with $9.3m and Polkadot-based products with $2.1m.”

As Bitcoin recently reclaimed the 50-day moving average (MA), is the 200-day MA next? If this happens, it will confirm an uptrend because this indicator shows the average of 40 weeks of trading.

Image source: Shutterstock

Source link

Pi Network: Is This Just a Massive Crypto Scam | Analyzed by an Accountant

Crypto For Beginners 2021 - Cryptocurrency Investing - Should I Buy Cryptocurrency? - BTC or ETH?

Yield Farming Paying 1,000% APR For Your Liquidity Pool Staking

Daily Farm Update | Token n Farm Launches | BSC & Polygon

BTT (BITTORENT) SIAP NAIK !?? SETELAH EVENT 10 JUNI?? PREDIKSI DAN ANALISA BTT (BITTORENT) 2021 !!

How to Transfer Crypto From Binance to Trust Wallet (2021) | CryptoCurrency Tutorial

-

liquidity4 weeks ago

liquidity4 weeks agoDaily Farm Update | Token n Farm Launches | BSC & Polygon

-

Usecase2 months ago

Usecase2 months agoBTT (BITTORENT) SIAP NAIK !?? SETELAH EVENT 10 JUNI?? PREDIKSI DAN ANALISA BTT (BITTORENT) 2021 !!

-

Usecase2 months ago

Usecase2 months agoHow to Transfer Crypto From Binance to Trust Wallet (2021) | CryptoCurrency Tutorial

-

Usecase2 months ago

Usecase2 months agoNext SAFEMOON | MARSMISSION Coin 100X ? Low Price Cryptocurrency 2021 | Best Profitable Crypto 2021

-

Education2 months ago

Education2 months agoKaran Dwivedi Zoom Meeting Crypto Bulls, ESPN Global, Master Nodes

-

Education2 months ago

Education2 months agoBest Crypto Coin To Invest in 2021 | Best Cryptocurrency To Invest 2021 | Wazirx | Safemoon Binance

-

liquidity2 months ago

liquidity2 months agoHow to Use Bunny Swap to Maximize Your Yield Farming on Binance Smart Chain

-

Usecase2 months ago

Usecase2 months ago4 Altcoins To Buy in the Dip For HUGE GAINS (Crypto Flash Crash 2021)