Binance

FTX to be the First to Receive a Virtual Asset Exchange (VAX) License in Dubai – Blockchain News, Opinion, TV and Jobs

Major global cryptocurrency exchange FTX is receiving a virtual asset exchange (VAX) license in Dubai, and is expanding its operations in the United Arab Emirates.

The VAX license is granted under a new cryptocurrency law and was issued by Sheikh Al Maktoum, creating a legal framework for crypto in the Emirate of Dubai, aimed at protecting investors and “designing much-warranted international standards” for industry governance.

The license allows FTX to operate within Dubai‘s crypto market model, which operates in compliance with global standards.

FTX founder and CEO Sam Bankman-Fried said that FTX had received the digital exchange license from Dubai. “Really excited to receive the first (and so far only) digial asset exchange license from Dubai!” Bankman-Fried tweeted. The company says it’s now planning to establish a regional headquarters in United Arab Emirates’ most international hub and city.

According to Bloomberg, Binance will also get a crypto license in Dubai under the same program, but it seems FTX beat the company to it. Apparently the United Arab Emirates is seeking to attract some of the world’s biggest crypto and fintech companies.

FTX recently reached $32 billion valuation after raising $400 million in a Series C round announced in January. The company has only been founded three years ago, but has already become one of the world’s largest crypto exchanges, in part through their marketing campaign during the Super Bowl.

Just like Binance, FTX’s European and Middle Eastern division FTX Europe was also among the first to join a new crypto hub, in the Dubai World Trade Centre, to create a specialised zone for virtual assets – including digital assets, products, operators and exchanges.

Source link

A proposal to ban global cryptocurrency exchange Binance from operating in the Philippines will not gather steam due to a lack of regulations towards cryptocurrencies in the country.

The Philippines’ Department of Trade and Industry (DTI) has cited no clear guidelines set out by the country’s central bank, Banko Sentral ng Pilipinas (BSP), as a dead-stop after a lobbying group called for the prohibition of Binance in early July.

Local think tank Infrawatch PH had asked the DTI to investigate Binance for the promotion of its services and offerings, which the group believed to have been done without the necessary permits.

Binance had looked to acquiesce the parties involved, telling Cointelegraph that it intends to secure virtual asset service provider and e-money issuer licenses in the Philippines.

Related: Terra crash highlights stablecoin risk to financial stability: ECB

Nevertheless, DTI is unable to enforce any ruling against Binance from operating in the country according to their latest correspondence with Infrawatch PH. As reported by Forkast, the department cited a lack of legislation for virtual assets creating a gray area:

“Cryptocurrency and other forms of virtual assets are not consumer products, the Department of Trade and Industry has no jurisdiction to act on applications for sales and promotion permits to promote virtual assets per se in the absence of clear legislation on the matter.”

The DTI noted that the proposal would fall under the auspices of the country’s central bank, which has to date not released any official guidelines or regulations for the use or sale of cryptocurrencies in the Philippines. This would include any companies or service providers conducting sales or promotion activities linked to financial products.

Source link

Citizens of Argentina are hedging their savings by using stablecoins amidst the recent climate of uncertainty created by the resignation of bound key members of the government.. The minister of economy within the country resigned last weekend, aboard alternative personalities, causing the turmoil that prompted the value of stablecoins within the country to rise by 11% on some exchanges.

Dollar-to-Peso Exchange Rate Plummets Because of Political Uncertainty in Argentina

The rate that voters in Argentina use to exchange the native enactment currency, the Argentinian peso, for Dollars, has plummeted because of the climate of political and economic uncertainty the country is presently facing. The resignation of economy minister Martin Guzman caused shockwaves, as he was one among the most important articulators of the deal the country linked with the International Money Fund(IMF) to structure the debt that the country has with the organization.

The resignation of Guzman conjointly led to demissions from alternative necessary officers of the ministry, together with Ramiro Tosi, Roberto Arias, and Rodrigo Ruete. This created the rate of exchange of pesos for the U.S. Dollars reach record numbers on completely different cryptocurrency exchanges. In step with Bloomberg, the speed reached 257 Argentine pesos on the Binance exchange, an increase of 6.6%. On the Lemon money exchange, the price jumped 11% to 279 pesos.

Inflation and Devaluation Driving Argentinians to Foreign Currencies and Crypto

The situation has caused Argentinians to rush to exchange their pesos for foreign currencies just like the U.S. Dollars and conjointly for dollar-pegged stablecoins like USDT. Even with the appointment of a brand new economy minister, Silvina Batakis, the market failed to recover to its previous rates. In step with native media, the rate of exchange fell even lower to 280 pesos per greenback, even reaching the 300 pesos per Dollar on some exchanges.

Furthermore, the volumes of stablecoins listed inflated considerably. Some operators rumored will increase 500% in volumes listed throughout some hours of the weekend, with most traders making an attempt to anticipate the increase in ancient markets to require advantage of the arbitrage opportunities.

The rate of exchange of the digital dollar went over the rate of exchange of the physical Dollar, showing that Argentinians value more highly to purchase these variants because of the simplicity of trading once more for alternative products and conjointly for the various uses they afford compared to greenback bills. The movements are according to a survey conducted by Americas Markets Intelligence in Apr, that found that 12% systems of the population have endowed in crypto, and 18% were inquisitive about finance in crypto.

The post Argentina Runs to Stablecoins Amidst Political and Economic Uncertainty first appeared on BTC Wires.

Source link

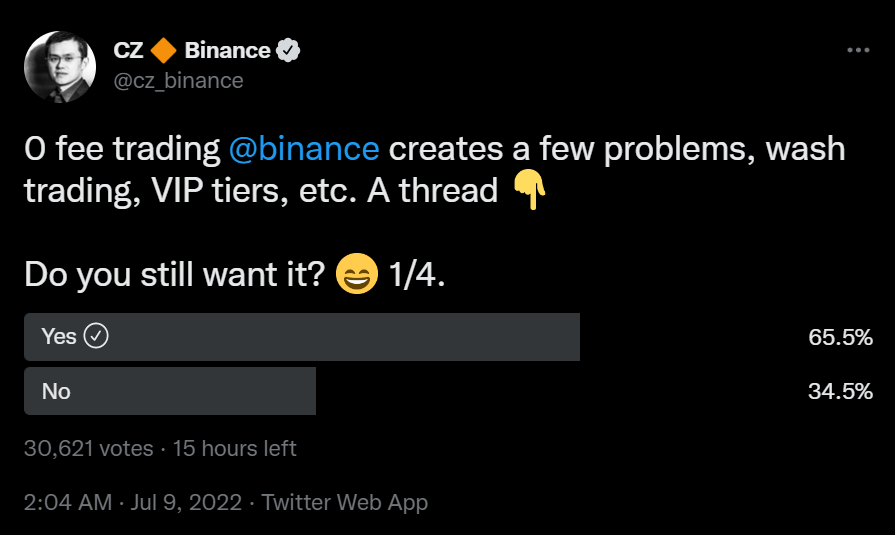

Both traditional and crypto investors consider trading fees as one of the most significant liabilities when it comes to investing over exchanges. So no wonder when Changpeng “CZ” Zhao, the founder and CEO of Binance, asked investors about their interest in trading on the crypto exchange with no fees, the response was a resounding yes despite the inherent risks pointed out by the entrepreneur.

Binance stands as the biggest crypto exchange, outdoing its nearest competition FTX by 10x in terms of the trading volume. Zhao, known for implementing features based on community feedback, reached out over Twitter to gauge investor sentiment regarding the complete removal of trading fees.

0 fee trading @binance creates a few problems, wash trading, VIP tiers, etc. A thread

Do you still want it? 1/4.

— CZ Binance (@cz_binance) July 8, 2022

While 0-fee trading may seem ideal for investors, CZ pointed out some of the issues it may sprout in the process — one of them being wash trading. Wash trading, wherein a user makes a series of buys and sells to manipulate market activity, can be used to go up the VIP tiers on Binance.

Moreover, CZ stated that bringing 0-fee trading to the masses will require Binance to implement numerous safeguards, which include detection tools for identifying illegitimate trades. Each VIP tier is tied to certain trading benefits including lower trading fees. As a result, professional poker player Brian Rast asked “So if there are no fees, why do you need VIP tiers?”

Over 30,600 investors voted on CZ’s poll at the time of writing — with around 65.5% inclined to trade with no fee whatsoever. CZ is open to implementing the changes regardless of the challenges that a new system would bring:

“Let’s see what the poll say. We listen to our users.”

Related: Binance gets VASP registration for its Spanish subsidiary from the Bank of Spain

Binance continues to spread its roots across the world as it steadily acquires registrations and operational licenses from regulators.

Maintaining its expansion streak, Binance’s Spanish subsidiary, Moon Tech Spain, got registered as a VASP by Spain’s central bank on Thursday. CZ attributed the development to Binance’s intent to protect users:

“Effective regulation is essential for the widespread adoption of cryptocurrencies. We have invested significantly in compliance and introduced AMLD 5 and 6 compliant tools and policies to ensure that our platform remains the safest and most trustworthy in the industry.”

Source link

Into Crab Mode, Bitcoin Bullish Potential Capped For The Coming Months?

How to build a passive income stream from cloud mining?

Successful Beta Service launch of SOMESING, ‘My Hand-Carry Studio Karaoke App’

List of TOP BTC Gambling Sites

US Treasury Delivers Crypto Framework to Biden as Directed in Executive Order

Bitcoin price indicator that marked 2015 and 2018 bottoms is flashing

Successful Beta Service launch of SOMESING, ‘My Hand-Carry Studio Karaoke App’

Tezos (XTZ) Nears 3-Week High

How a Presale Ethereum Wallet Containing 1000 ETH Was Recovered by KeychainX

Ethereum co-founder responds to PoS critics amid upcoming Merge

theBlock Research Pins Stacks as a Key Player in the BTC Network

Bitcoin price hits 7-day low as US warns of ‘highly elevated’ CPI data

Bitcoin Erases Last Week Gains As Price Sinks Below $20,000

The UK’s largest Bitcoin conference comes to Scotland

Are North Korean IT Remote Workers Targeting Crypto Firms? Here’s What We Know

BNM DAO Token Airdrop

New Minting Services

Could an Earnings Recession Lead to More Pain for Crypto? – Blockchain News, Opinion, TV and Jobs

‘Crypto is just like the end of the 90s with the internet bubble,’ says Hodl CEO Maurice Mureau

Virginia passes new crypto law whilst macro headwinds mount up – Blockchain News, Opinion, TV and Jobs

Interview with Ruud Feltkamp, Owner of AI-driven Trading Bot Cryptohopper – Blockchain News, Opinion, TV and Jobs

A Bear of Historic Proportions – Blockchain News, Opinion, TV and Jobs

High-profile BAYC collector denies allegations of wrongdoing brought by DeFi detective

BNM Live Stream

Tesla, Blockstream and Jack Dorsey’s Block Team-up to Mine Bitcoin Sustainably – Blockchain News, Opinion, TV and Jobs

Are expiring copyrights the next goldmine for NFTs?

Block News Media Live Stream

Live Stream Block News Media

Fintech-Ideas brings blockchain functionality to its range of platforms – Blockchain News, Opinion, TV and Jobs

CULT DAO’s Revolt 2 Earn Concept Draws the Attention of Anonymous – Blockchain News, Opinion, TV and Jobs

-

Uncategorized6 months ago

BNM DAO Token Airdrop

-

Uncategorized8 months ago

New Minting Services

-

bear market2 weeks ago

bear market2 weeks agoCould an Earnings Recession Lead to More Pain for Crypto? – Blockchain News, Opinion, TV and Jobs

-

Blockchain2 weeks ago

Blockchain2 weeks ago‘Crypto is just like the end of the 90s with the internet bubble,’ says Hodl CEO Maurice Mureau

-

Bitcoin2 weeks ago

Bitcoin2 weeks agoVirginia passes new crypto law whilst macro headwinds mount up – Blockchain News, Opinion, TV and Jobs

-

Blockchain2 weeks ago

Blockchain2 weeks agoInterview with Ruud Feltkamp, Owner of AI-driven Trading Bot Cryptohopper – Blockchain News, Opinion, TV and Jobs

-

bear markets2 weeks ago

bear markets2 weeks agoA Bear of Historic Proportions – Blockchain News, Opinion, TV and Jobs

-

Blockchain Analytics2 weeks ago

Blockchain Analytics2 weeks agoHigh-profile BAYC collector denies allegations of wrongdoing brought by DeFi detective