Europe

How new EU regulation will affect the global crypto market

From the beginning of July, crypto exchanges and stablecoin issuers will operate in the EU according to the rules provided for by the MiCA law.

The entry into force of the Markets in Crypto-Assets (MiCA) law on June 30 means significant changes for the cryptocurrency industry in the EU. One of MiCA’s key provisions is regulating stablecoins, as well as rules for a wide range of crypto assets and exchange platforms.

What MiCA says

MiCA is a regulatory framework that clarifies and uniformly regulates the cryptocurrency market. It defines digital asset classification and specifies laws and areas of responsibility for their implementation.

Last April, members of the European Parliament voted in favor of the cryptocurrency regulation bill MiCA. The EU has become one of the first jurisdictions in the world to introduce comprehensive regulations on crypto assets.

Companies will have to provide full disclosure to customers, present a public business model, establish an effective governance system, including risk management, register with the European Banking Authority (EBA), establish a buyback mechanism, and have sufficient reserves.

In addition, issuers of asset-related tokens (ART) and electronic money tokens (EMT) must disclose sustainability information from June 30, and crypto service providers must begin asking for disclosure requirements by the end of the year.

ART issuers (other than credit institutions) may continue to operate if tokens were issued before June 30, until they are granted or denied authorization under the MiCA, provided they apply for permission until July 30.

Entities not complying with MiCA may be fined and barred from operating in the European Union.

What restrictions have crypto companies introduced?

Due to the introduction of MiCA legislation in the EU, some crypto firms have begun restricting the use of stablecoins.

In March, OKX suspended trading of the largest stablecoin, Tether (USDT), for users located in the European Union.

In early June, the Binance exchange announced that it would limit access to unregulated stablecoins for customers from the European Union. Binance will also limit the number of services that may involve unregulated stablecoins. The copytrading service and participation in the Launchpad and Launchpool programs will be entirely unavailable for European exchange clients.

Crypto exchange Bitstamp said it will delist the EURT, the euro-pegged Tether’s stablecoin, and other stablecoins that do not comply with new EU crypto asset laws by June 30.

Also, the European company Lugh announced that it would cease issuing its EURL stablecoin before the MiCA regulation entered into force.

State of the Stablecoin Market

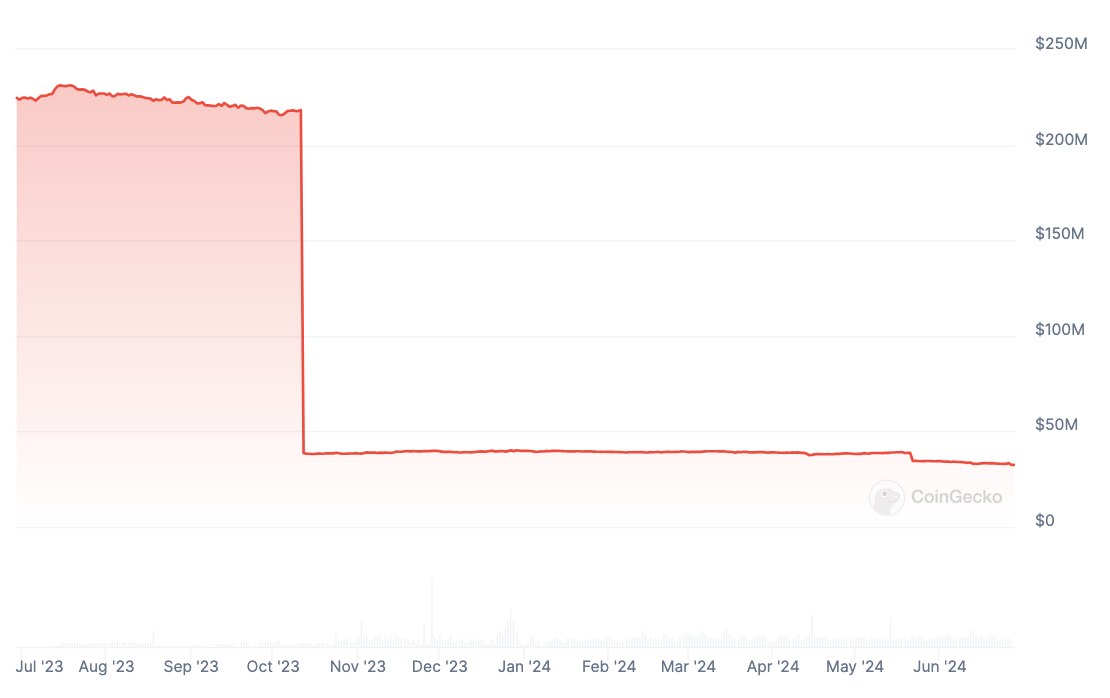

According to CoinGecko, throughout 2023, the stablecoin EURT rapidly lost its popularity in the European crypto community. By October last year, the crypto asset’s capitalization fell almost tenfold compared to its peak in 2022—from $231 million to $32 million.

EURT is the second-largest stablecoin pegged to the euro by capitalization. Compared with USDT from the same Tether, EURT’s volume in circulation is small—only 32.1 million coins as of June 26.

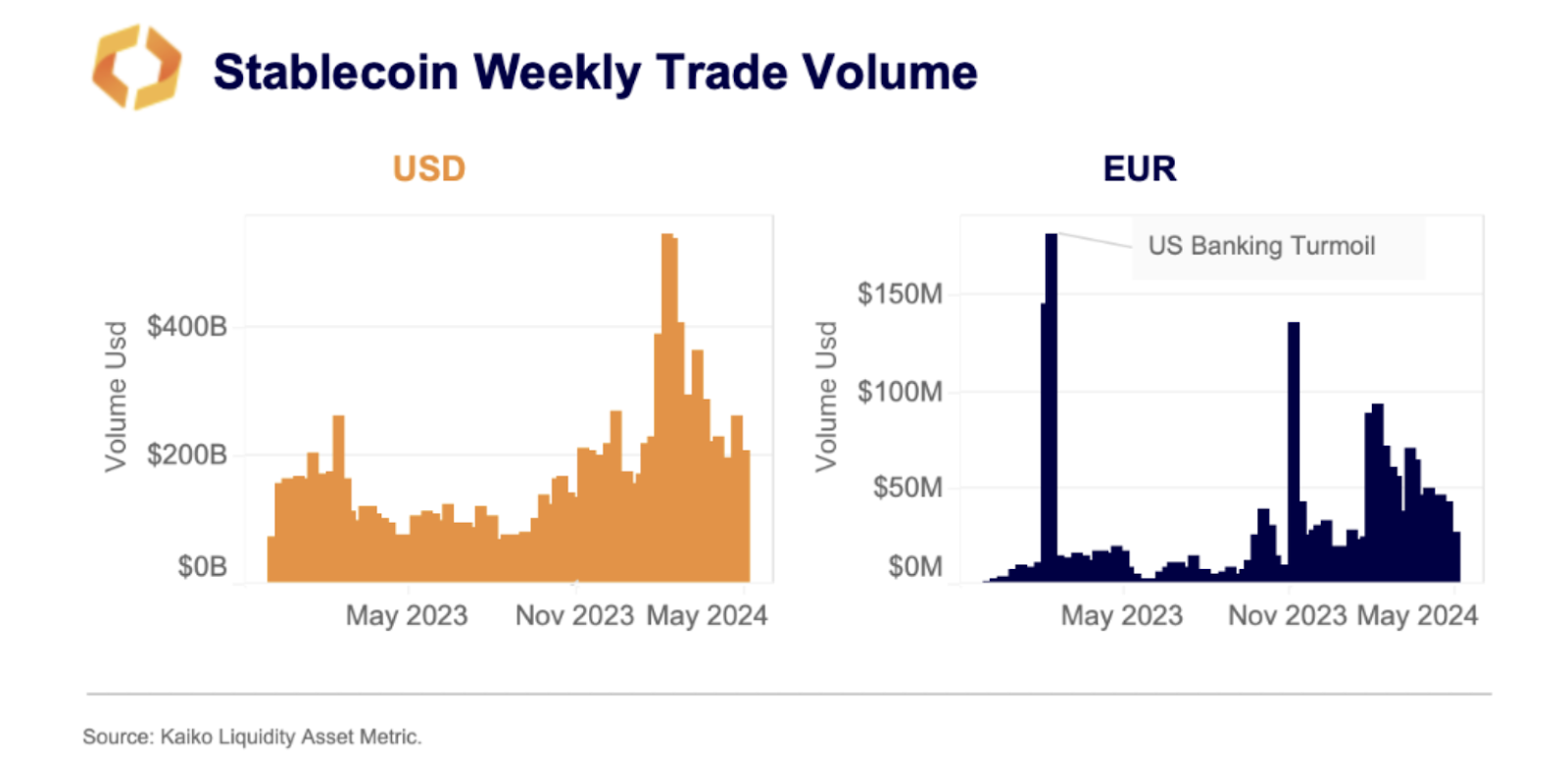

According to a report from analytics firm Kaiko, stablecoins backed by euro reserves account for just 1.1% of the total trading volume of stablecoins backed by fiat currencies.

The study also shows that most (90%) of stablecoin transactions are in U.S. dollar-backed assets. Only 10% of stablecoins are backed by reserves in other currencies and real assets, including gold.

The weekly trading volume of dollar stablecoins such as USDT exceeds $270 billion. Meanwhile, the total turnover of euro stablecoins EURT, EURS, EURCV, AEUR, and the like is only about $40 million per week. However, analysts expect growth in this segment as European regulators pressure exchanges to withdraw dollar assets from circulation.

What the experts say

Analyst MartyParty generally expects an explosion of stablecoins after the implementation of MiCA. He believes European Union banks, institutions, and stablecoin issuers will begin minting trillions of euro-backed stablecoins in July.

Alexander Ray, CEO and co-founder of Albus Protocol, notes that new regulations will require all organizations involved in business transactions using asset-linked tokens to implement many regulatory measures, such as KYC and AML protocols.

He said that implementing KYC and AML protocols will definitely increase crypto companies’ operating costs, and users will ultimately pay for it.

Sven Mohle, managing director of BitGo Europe GmbH, added that with the adoption of MiCA, Europe is helping to set the bar for promoting international standards regarding rules and regulations related to combating money laundering and the financing of terrorism. However, it is unlikely that users will see fully standardized international rules across the board.

Source link

Disclosure: The views and opinions expressed here belong solely to the author and do not represent the views and opinions of crypto.news’ editorial.

The Markets in Crypto-Assets Regulation (MiCA) marks a significant milestone in the European Union’s journey toward regulating the rapidly evolving crypto market. Its timeline and provisions hold immense importance for both crypto businesses and investors. As we approach crucial dates, starting with the application of stablecoin provisions from June 30, 2024, and the complete application of MiCA on December 30, 2024, the crypto landscape is undergoing a transformative phase.

Over the next two years

MiCA’s staggered timelines and transitional periods, extending up to June 30, 2026, imply a period of fragmented implementation across the EU and European Economic Area (EEA). Jurisdictions such as Ireland (12 VASPs), Spain (96 VASPs), and Germany (12 VASPs) will grant a 12-month transitional period. In contrast, other jurisdictions will offer more extended periods, such as France (107 VASPs) with 18 months, while Lithuania (588 VASPs) will likely only grant five months. This transitional phase will prompt market consolidation as not all existing service providers will secure MiCA licenses. Many will look to capitalize on this interim period before winding down operations.

The race among EU/EEA jurisdictions to become the primary hub for crypto activities intensifies, with jurisdictions like France, Malta, and Ireland competing to take the top spot. However, regulator readiness and compliance for crypto-asset businesses pose significant challenges. Regulators are facing an adjustment period to upskill their staff to process MiCA applications, particularly in jurisdictions with high applicant volumes. The complexity of various business models, encompassing numerous products unfamiliar to regulators, exacerbates this challenge. The general lack of expertise to authorize and supervise this sector requires substantial training efforts.

Challenges for crypto businesses

MiCA, coupled with the vast array of related Level-2 measures (many of which still need to be finalized) and other applicable EU instruments such as the anti-money laundering laws, the Digital Operational Resilience Act (DORA), and the Electronic Money Directive (EMD), create a complex regulatory framework. Understanding what provisions apply to each entity type and what documentation needs to be implemented will be challenging for some.

The delisting of crypto-assets, particularly stablecoins, from EU exchanges due to their issuers’ failure to obtain their licenses on time will pose considerable hurdles and limit the availability of certain assets for consumers.

Adapting to MiCA will strain many entities and require substantial investments in technological infrastructure. The Travel Rule, a requirement in which information must be shared between VASPs with each crypto transaction, also comes into effect at the same time as MiCA. The Travel Rule mandates that CASPs transfer a substantial amount of information about the originator. This includes their address, personal identification number, and customer identification number. In rare cases, it may even require the disclosure of the originator’s date and place of birth. This adds another layer of complexity, further highlighting the need for harmonization within the EU and solutions to comply with the Travel Rule that are interoperable and enable secure data sharing while preserving user privacy.

Key crypto market outcomes

Despite the challenges, MiCA instils confidence in EU entities due to heightened regulatory oversight, the promotion of investor protection and attracting mainstream institutional participation. Enhanced consumer protection measures mitigate risks such as fraud and hacking, fostering trust among retail clients.

MiCA’s reporting requirements will result in regulators across the EU possessing more data, empowering them to monitor market activities effectively. The ability to freely passport activities across the EU will facilitate cross-border operations and reduce regulatory fragmentation while expanding market reach.

MiCA’s prescriptive nature and all-encompassing regime set a precedent for global regulatory frameworks. Other jurisdictions are already observing and may replicate some of MiCA’s provisions and its approach, contributing to regulatory harmonization on a worldwide scale. However, concerns remain as to whether it will stifle growth and innovation and whether businesses will look to relocate to more permissive and less restrictive jurisdictions.

Steps after MiCA

MiCA’s gaps in regulating emerging areas like true defi (the provision of financial services or issuance of financial assets without identifiable intermediaries and with no single point of failure), lending, and NFTs necessitate ongoing policy discussions and further regulatory measures. Reports on these aspects will inform future regulatory developments, potentially leading to a second iteration of MiCA in at least the next four to five years or supplementary measures.

MiCA signals a new era of regulation in the crypto market, aiming to balance innovation with investor protection and market integrity. While challenges persist, MiCA lays the groundwork for a more transparent, secure, and inclusive crypto framework in the EU and beyond. As the crypto landscape continues to evolve, regulatory regimes must adapt to emerging trends and technologies, ensuring sustainable growth and fostering investor confidence.

Source link

Blockchain-based payments firm Ripple Labs can now provide certain digital asset services in Ireland.

In a new statement, the San Francisco-based firm says the Central Bank of Ireland (CBI) has just granted its local subsidiary, Ripple Markets Ireland Limited, the license to operate as a Virtual Asset Service Provider (VASP).

VASPs can carry out transactions involving crypto assets — including exchanges, transfers, wallet custody and crypto-related financial services — on behalf of clients.

Says Ripple vice president of strategic initiatives, Eric van Miltenburg,

“Ireland has positioned itself as a supportive jurisdiction for the virtual assets industry and consequently as a great place for businesses like Ripple’s to operate, reinforcing our decision to select Ireland as our primary base for EU regulation.

By providing regulatory clarity for the industry, Ireland – and the EU more broadly – are boosting confidence in the digital assets, payments and fintech ecosystem and demonstrating their commitment to the long-term development of these industries.”

The CBI says it grants the VASP license to firms with satisfactory anti-money laundering and combating the financing of terrorism (AML/CFT) policies and procedures following a risk-based assessment process.

Other firms on the central bank’s VASP register include the crypto exchanges Coinbase and Gemini and the online payments company Paysafe.

Ripple says it is now aiming to operate in more jurisdictions in Europe.

“Ripple will seek to provide services to clients across the European Economic Area once the Markets in Crypto Assets Regulation (MiCA) comes into force at the end of 2024, subject to the acquisition of other necessary licenses.”

Don’t Miss a Beat – Subscribe to get email alerts delivered directly to your inbox

Check Price Action

Follow us on Twitter, Facebook and Telegram

Surf The Daily Hodl Mix

Disclaimer: Opinions expressed at The Daily Hodl are not investment advice. Investors should do their due diligence before making any high-risk investments in Bitcoin, cryptocurrency or digital assets. Please be advised that your transfers and trades are at your own risk, and any loses you may incur are your responsibility. The Daily Hodl does not recommend the buying or selling of any cryptocurrencies or digital assets, nor is The Daily Hodl an investment advisor. Please note that The Daily Hodl participates in affiliate marketing.

Generated Image: Midjourney

Source link

Fintech innovations and emerging technologies have swept the world, causing global lawmakers to rush to understand and regulate them.

While some countries like the United States and El Salvador have had a public relationship with adopting new technologies, others have quietly joined the game. Among these is Latvia, a small country located in the Baltics, neighboring Estonia and Lithuania.

Cointelegraph spoke with Marine Krasovska, the head of financial technology at Latvijas Banka (Bank of Latvia) — Latvia’s central bank — to better understand how regulators in the country are dealing with new technologies like cryptocurrencies and artificial intelligence (AI).

Unlike its neighbor Estonia, which was the first European country to provide clear regulations and guidelines for digital currencies, these assets remain unregulated in the Latvian landscape. The Latvian Personal Income Tax Act defines crypto as a capital asset subject to the general capital gains tax of 20%.

Back in 2020, one of the country’s financial regulators, the Financial and Capital Market Commission (FCMC), warned the public about crypto fraud — particularly given that in Latvia, crypto companies “operate in an infrastructure that is currently characterized by lower regulation than in the financial and capital markets.”

An upcoming hub of innovation

Since early warnings from the FCMC, Latvia has not developed new cryptocurrency regulations. However, Krasovska explained that in the last five years, the central bank, which is the primary regulator in Latvia, has been operating its Innovation Hub.

Krasovska said participation by fintech companies is not mandatory; however, the bank advises it as a “first entry point” to the Latvian market. The central bank offers this service free of charge for international companies and those originating from Latvia.

“When businesses come to the Innovation Hub and begin to describe their business model, sometimes we start to understand what companies actually need and don’t need,” she said.

She added that it’s an opportunity for businesses to talk in person with regulators to understand the business licensing needed and get risks assessed.

“We always suggest for companies to bring a lawyer to disclose interpretation risks. Interpretation of legislation is a very high-level responsibility.”

Within the Innovation Hub, the bank has also created a pre-licensing process. According to Krasovska, this was created to help fintech companies — particularly those dealing with digital assets — create a “package of documents” that they can receive feedback on regarding the quality.

Related: Germany’s blockchain funding increases 3% amid market downturn: Report

“So when the official application goes in,” she said, “the license process will be focusing on the main ideas rather than the quality of the application. This new pre-licensing began last summer.”

“We want to see more innovation on the market. But we also want to see that the risks are managed in a proper way.”

Krasovska said that last year, the Innovation Hub had 72 consultations with around 40% of all participants from Latvia. She commented that the hub’s data reveals increased interest from companies in “crypto and electronic money institutions services.”

Adoption from the inside

Along with helping businesses thrive in the Latvian fintech landscape, Krasovska said that the Latvian central bank itself is adopting new technologies to streamline its processes from the inside.

This includes moving central bank data into the cloud and adopting AI technologies like OpenAI’s popular chatbot ChatGPT.

“We, as a central bank, will also start this year to integrate artificial intelligence and ChatGPT in our work. Not just not just trying to do some kind of studies as everyone is using it, but we’re starting to adapt it in terms of we have identified our needs.”

She said the central bank created an internal lab two years ago, which began experimenting with different kinds of technological solutions.

Related: European Banking Authority calls for early adoption of stablecoin standards

She highlighted ChatGPT feasibility studies the bank has conducted, which will help it summarize large quantities of documents, such as tax documents that she called “not structured information.”

Krasovska also said the bank employs AI to help with data direction projects and supervise code.

Synthetic data creation

When it comes to data, the fintech executive said the Bank of Latvia is spearheading a new project in relation to synthetic data.

She said that when newcomers or tech companies developing new solutions ask for a data set to train business models, it has nothing it can legally provide.

“This year and also next year, we will be working with the database ideas from which we can create this synthetic data that is like a synthetic lottery or something along those lines,” she said.

“Then companies can come and use these different types of data to understand how their tools work or don’t work before they scale the business and offer their solution to real customers.”

For example, businesses may need access to a large transaction database to understand how related monitoring tools work, “so what we’re doing right now is working on this integrated database,” she said.

Latvia and the current state of crypto

Over the summer, a report from the Latvian central bank said that local investments in crypto assets had declined by 50% over the past year.

“The number of the people purchasing crypto-assets as well as making payments with payment cards to invest in crypto-assets in Latvia declines.

This can be explained by global developments such as the negative sentiment of investors, detected cases of fraud and cases of… pic.twitter.com/uOIbJvIlsi

— Joshua Rosenberg (@_jrosenberg) August 4, 2023

The report was based on findings from payment card usage, revealing that 4% of the population bought crypto assets in February 2023, compared to 8% in the same month of 2022.

When asked about the sentiment toward cryptocurrencies in Latvia, Krasovska pointed to the crypto market conditions in combination with slumping market trends globally: “Globally, the financial markets are the way they are right now, and of course, this is [excluding] the crypto [market].”

Magazine: Crypto lawyer Irina Heaver on death threats, lawsuit predictions: Hall of Flame

Aside from the rocky conditions for the crypto community brought on by the lingering bear market, regulatory difficulties in major markets have caused investor sentiment to become less optimistic.

However, Krasovska pointed toward the European Union’s adoption and implementation of the Markets in Crypto-Assets (MiCA) legislation as something the central bank can lean on.

“With the adoption of MiCA, we can ensure very high standards for financial services.”

Collect this article as an NFT to preserve this moment in history and show your support for independent journalism in the crypto space.

Source link

MATIC Price Crash: Reaching A Two Year Low

Multicoin Pledges up to $1M for Pro-Crypto Senate Candidates

Crypto heists near $1.4b in first half of 2024: TRM Labs

FTX Founder Sam Bankman-Fried’s Family Accused Of $100M Illicit Political Donation

Bitcoin Price Falls as Mt Gox Starts Repayments

20% Price Drop Follows $87 Million Spending Outrage

More than 10 years since the collapse of Mt. Gox, users confirm reimbursements

Leading Telecom Company Taiwan Mobile Gets Crypto Exchange License

Here Are Price Targets for Bitcoin, Solana, and Render, According to Analyst Jason Pizzino

Bitcoin price plunges below $55k as Mt. Gox announces repayments

Jasmy Sheds 20% Amid Bitcoin Sell-Off

Are they a good thing?

Mt. Gox Transfers $2.7 Billion in Bitcoin From Cold Storage Amid Market Rout

What’s Next For Ethereum (ETH) as Price Hovers $3,000?

Bitcoin’s quick dip below $57k forces beginners to capitulate, CryptoQuant says

Bitcoin Dropped Below 2017 All-Time-High but Could Sellers be Getting Exhausted? – Blockchain News, Opinion, TV and Jobs

What does the Coinbase Premium Gap Tell us about Investor Activity? – Blockchain News, Opinion, TV and Jobs

BNM DAO Token Airdrop

NFT Sector Keeps Developing – Number of Unique Ethereum NFT Traders Surged 276% in 2022 – Blockchain News, Opinion, TV and Jobs

A String of 200 ‘Sleeping Bitcoins’ From 2010 Worth $4.27 Million Moved on Friday

New Minting Services

Block News Media Live Stream

SEC’s Chairman Gensler Takes Aggressive Stance on Tokens – Blockchain News, Opinion, TV and Jobs

Friends or Enemies? – Blockchain News, Opinion, TV and Jobs

Enjoy frictionless crypto purchases with Apple Pay and Google Pay | by Jim | @blockchain | Jun, 2022

How Web3 can prevent Hollywood strikes

Block News Media Live Stream

Block News Media Live Stream

Block News Media Live Stream

XRP Explodes With 1,300% Surge In Trading Volume As crypto Exchanges Jump On Board

Altcoins2 years ago

Altcoins2 years agoBitcoin Dropped Below 2017 All-Time-High but Could Sellers be Getting Exhausted? – Blockchain News, Opinion, TV and Jobs

Binance2 years ago

Binance2 years agoWhat does the Coinbase Premium Gap Tell us about Investor Activity? – Blockchain News, Opinion, TV and Jobs

- Uncategorized3 years ago

BNM DAO Token Airdrop

BTC1 year ago

BTC1 year agoNFT Sector Keeps Developing – Number of Unique Ethereum NFT Traders Surged 276% in 2022 – Blockchain News, Opinion, TV and Jobs

Bitcoin miners2 years ago

Bitcoin miners2 years agoA String of 200 ‘Sleeping Bitcoins’ From 2010 Worth $4.27 Million Moved on Friday

- Uncategorized3 years ago

New Minting Services

Video2 years ago

Video2 years agoBlock News Media Live Stream

Bitcoin1 year ago

Bitcoin1 year agoSEC’s Chairman Gensler Takes Aggressive Stance on Tokens – Blockchain News, Opinion, TV and Jobs