dApp

dApp Store kit adopts new tech stack to power Web3 gaming development

dApp Store Kit, which was initially incubated by Polygon Labs, will integrate Ready Games’ mobile game development toolkit to help developers roll out Web3 games.

dApp Store Kit’s toolkit for deploying EVM-compatible DApp stores will combine with Ready Games, allowing developers to integrate Web3 on-chain support. This will include the ability to integrate wallets and on-chain user profiles as well as a DApp Store frontend stack to launch Web3 games.

The announcement highlighted the prevalence of ‘clunky user experience’ on mobile Web3 games, which often require users to constantly switch in and out of games to interact with external wallet apps.

Ready Games operates in the free-to-play gaming space, with studios representing over 2500 games and 80 million active monthly users set to feature their titles in the platform’s soon to be launch dApp Store.

Related: What are Web3 games, and how do they work?

Many of these publishers are expected to migrate existing games to Web3 using Ready Games’ development tools and dApp Store Kit and deployed on decentralized Polygon scaling protocols.

Ravikant Agrawal, Polygon Labs director of growth said that gaming remains a focal point for the Web3 ecosystem in which Dapp stores can drive improved user experience and engagement:

“By leveraging decentralized application stores, gamers can enjoy a seamless and secure experience while also contributing to the growth of the Web3 community.”

Ready Games CEO David Bennahum added that the integration of the platform’s Web3 gaming technology and dApp Store Kit could innovate the mobile gaming landscape:

“This integration paves the way for a new era of immersive and decentralized gaming experiences that will drive mass adoption of Web3 technology.”

Decentralized application (DApp) development platform dApp Store Kit has incorporated a leading Web3 game development technology stack to help Web2 game publishers migrate their titles into Web3.

Casual gamers have been earmarked as a potential driver of blockchain-powered games by industry players. Meanwhile the Web3 gaming industry still draws criticism from mainstream commentators for tokenomics issues and general user experience and playability concerns.

Magazine: Blockchain games take on the mainstream: Here’s how they can win

Source link

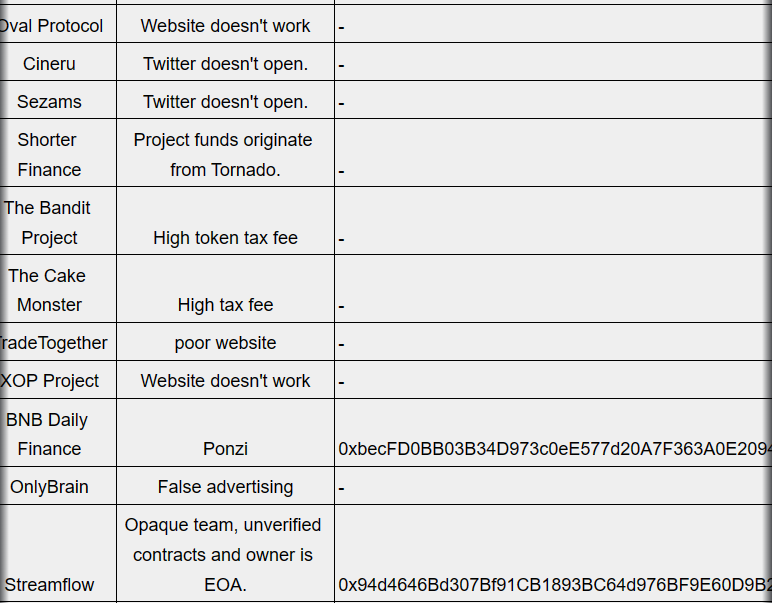

BNB Chain, the blockchain developed by crypto exchange Binance, updated its red alarm list to include 191 high-risk projects and decentralized applications (DApps) currently hosted on the blockchain.

BNB Chain’s red alarm list — updated every Friday — includes projects and DApps deemed risky investments purely based on smart contract assessment. The 191 new projects on BNB Chain that have been added to the list are either suspected of issuing fake tokens, high or opaque tax fees or simply because their websites or Twitter handles don’t work.

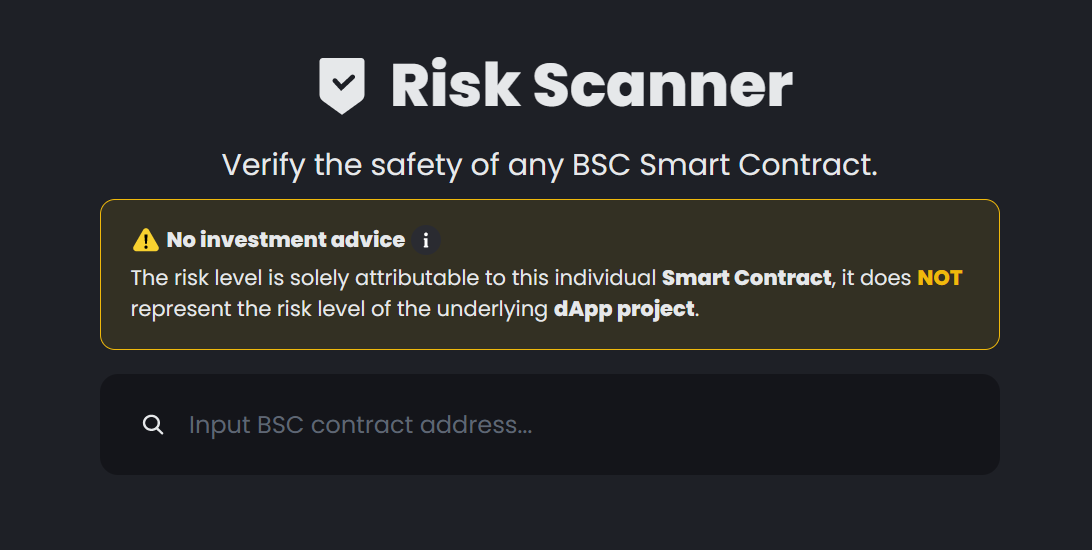

The above screenshot shows a portal wherein users can scan any BNB Chain projects for risks. Out of the lot, three projects — CycGo, Piston token and Shorter Finance — were flagged after being suspected of being funded by assets originating from Tornado.

“Make sure to review our weekly Red Alarm list to familiarize yourself with suspicious actors on our network,” read BNB Chain’s announcement on the matter. It is important to note that BNB Chain’s proactive alert is not investment advice and does not represent the risk level of the underlying DApp projects. Instead, it is aimed at helping users in their research before making investment decisions.

Related: 73.3% of Q1 rug pulls happened on BNB Chain: Immunefi

On April 10, BNB Chain began testing BNB Greenfield, an in-house attempt to deliver decentralized storage solutions.

We’re celebrating the BNB Greenfield testnet release!

Read the article below, then complete the following steps and we’ll pick 5 entries to share a prize pool of $500 on April 19th.https://t.co/O5BkyIJDSq

♥️ Like

♻️ RT

Share your thoughts on testnet using #BNBGreenfield pic.twitter.com/gmIvwCSvvB— BNB Chain (@BNBCHAIN) April 12, 2023

As Cointelegraph reported, BNB Greenfield allows users to create wallets and manage data, while developers can exercise control over data assets.

Magazine: Crypto audits and bug bounties are broken: Here’s how to fix them

Source link

The cryptocurrency space has no shortage of skeptics. While many people criticize the environmental impact of proof-of-work blockchains or the proliferation of scams, one particular argument against crypto often stands out: Blockchain has no real use cases.

Every two weeks, Cointelegraph’s The Agenda podcast breaks down this critique and explores the various ways blockchain and crypto can help everyday people.

On this week’s episode of The Agenda, hosts Jonathan DeYoung and Ray Salmond chat with Elisha Owusu Akyaw, Cointelegraph’s own social media specialist and host of the Hashing It Out podcast, to break down how Africans are using crypto to strengthen financial inclusivity and potentially turn countries into hubs of technological innovation.

How crypto is helping everyday Africans

According to Akyaw, crypto offers a more convenient, affordable way to send money both regionally and around the world. “Western Union, MoneyGram and all of these money transaction firms or rails have made millions from Africa for so long” by charging high fees, said Akyaw, whereas the cost required to send money via crypto is significantly lower.

Bitcoin (BTC) also offers a better store of value for most Africans than local fiat currencies, Akyaw argued. Speaking on his own experience of living in Ghana, he said that “you can buy Bitcoin and keep it for the next one year or six months. It’s a better hedge against inflation than keeping the Ghanaian cedi.”

Finally, the crypto industry is opening up new opportunities on the continent. “At every point of development, Africa has been left behind,” said Akyaw. But the global nature of the industry and the fact that it’s still in its early development present a unique opportunity to participate and benefit from its growth.

“This is one of the first times where there is a big shift happening and Africans are able to contribute. Africans are able to benefit directly from the shift that is happening without it having to pass through an intermediary, which is usually the state. And I think it’s an amazing thing.”

The next Silicon Valley?

When asked about what it would take for countries in Africa to become “magnets for crypto builders or a new kind of Silicon Valley,” Akyaw pointed to two factors that need to be improved for developers, startups and fintech companies to want to make the continent their home: regulation and infrastructure.

Umm. So I met @jack at the @AfroBitcoinOrg Conference.

I have been smiling since pic.twitter.com/SJKjkU6nAb

— Elisha - GhCryptoGuy (@ghcryptoguy) December 5, 2022

The majority of African countries lack proper regulation, according to Akyaw, while also condemning the use of crypto. This means companies are often unable to obtain licenses to set up shop and residents are dissuaded from interacting with Web3 protocols and firms:

“You can’t get a license. You can’t work with a bank in the country. You can’t do a lot of things. So, it makes no sense for you to come in.”

The other thing that needs to change, said Akyaw, is that electric grids need to be more stable and internet needs to be more reliable. “If you want a lot of Big Tech companies to come in, they must have great, 24/7 electricity. Internet must be awesome because a lot of what we do in the crypto space is virtual.”

To hear more from Akyaw’s conversation with The Agenda — including his backstory, whether outside funding has any negatives and the potential near-term future of crypto in Africa — listen to the full episode on Cointelegraph’s Podcasts page, Apple Podcasts or Spotify. And don’t forget to check out Cointelegraph’s full lineup of other shows!

Magazine: Unstablecoins: Depegging, bank runs and other risks loom

Source link

Blockchain gaming

Gamers made up nearly half of all blockchain activity in January: DappRadar Report

Play-to-earn blockchain gaming experienced a downturn over the last year as gamers prioritized improving the gameplay experience.

However, according to a new report from DappRadar, in the first month of 2023, gamers made up nearly half (48%) of all blockchain activity.

January also saw the market caps for top gaming tokens increase by 122% on average, with Gala (GALA), the digital utility token of the Gala Games ecosystem, surging by 218%.

According to the report, the rise in interest in these gaming tokens comes as industry buzz hits mainstream audiences. For example, Gala Games made headlines after it acquired a new mobile gaming studio with more than $20 million in assets under management and 15 games.

Blockchain analyst at DappRadar, Sara Gherghelas, told Cointelegraph that based on on-chain metrics from the past two years, it’s safe to assume blockchain gaming will continue to be a significant sector in the industry.

“This is because blockchain gaming is already a vertical in the traditional industry. As blockchain gains more traction, it will bring more adoption to Web3 games which will become mainstream.”

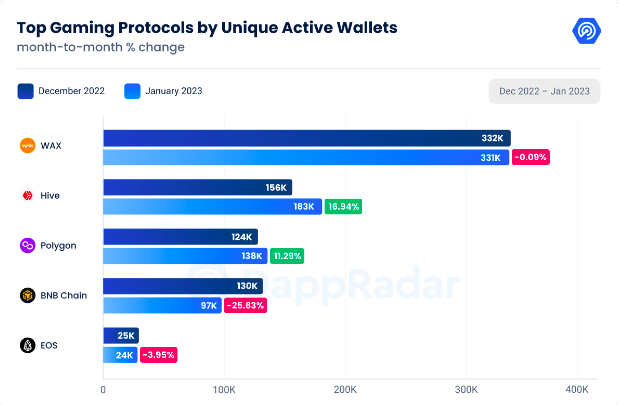

The Wax blockchain continues to have the most active gaming activity, with 331,000 unique active wallets. The top three blockchain gaming ecosystems all saw an increase in gaming protocols from the end of 2022 to the beginning of 2023, except for the BNB Chain.

The beginning of 2023 saw increased activity as strong funding set the stage for what many call blockchain gaming’s “buidling” year. This term encapsulates the industry’s focus on building more powerful, high quality games.

Gherghelas said the amount of investments toward this vertical is “increasing significantly,” with overall investment in 2022 around $7.6 billion — a 105% increase from 2021. Investments into the blockchain gaming industry topped $156 million in January alone.

Related: Ushering in a new era of Web3 gaming by making Play-to-Earn sustainable

Additionally, the report highlighted the metaverse’s role in the uptick in blockchain gaming activity this year. The data revealed that the trading volume for January in virtual world-related games hit $44.5 million, a 114% increase from the month prior.

Although sales decreased by 19%, the overall growth can be attributed to the success of major metaverse platforms such as The Sandbox and Decentraland, with an increase in trading volume of 114% and 83%, respectively.

According to at 2022 report from DappRadar, Web3 gaming accounted for nearly half of all blockchain-based transactions in the year.

Source link

XRP Allegedly Attacked By SEC’s Hinman For Ethereum’s Benefit

On-chain sleuth ZachXBT sued for libel after claiming plaintiff drained funds from project

Percentage Of ETH Addresses In Profit Reaches 5-Month Low

Think AI tools aren’t harvesting your data? Guess again

Bitcoin Bullish Momentum Building: Expert Predicts Rise To $27,200

Which altcoins will survive the SEC crackdown? Bitcoin OG explains

Curve (CRV) Observes 7% Bounce As Short Squeeze Occurs

Bakkt follows Robinhood, eToro in delisting major altcoins: Report

Shiba Inu Lead Developer Unveils Shibacals, Advancing Shibarium Development

dApp Store kit adopts new tech stack to power Web3 gaming development

Polygon Sees Surge In Whale Buying: Recovery In The Cards?

7 alternatives to ChatGPT

What Happens To Bitcoin Price If Spot ETF Is Approved?

SEC argues against Dentons’ motion to dismiss Terraform and Do Kwon’s lawsuit

Why Is Bitcoin Up Today?

Judge rules LBRY video platform’s token is a security in case brought by the US SEC

Will the Bitcoin mining industry collapse? Analysts explain why crisis is really opportunity

Silvergate Capital’s crypto-to-fiat transfers decrease by $50B compared to Q3 2021

Exchange Outflows Shows Bitcoin, Ethereum Accumulation Trend Continues

Bitcoin Dropped Below 2017 All-Time-High but Could Sellers be Getting Exhausted? – Blockchain News, Opinion, TV and Jobs

BNM DAO Token Airdrop

What does the Coinbase Premium Gap Tell us about Investor Activity? – Blockchain News, Opinion, TV and Jobs

Fed policy and crumbling market sentiment could send the total crypto market cap back under $1T

New Minting Services

Can Cardano’s July hard fork prevent ADA price from plunging 60%?

Friends or Enemies? – Blockchain News, Opinion, TV and Jobs

SEC’s Chairman Gensler Takes Aggressive Stance on Tokens – Blockchain News, Opinion, TV and Jobs

LUNA2 Recovers 70% In Nine Days From Historic Lows

Enjoy frictionless crypto purchases with Apple Pay and Google Pay | by Jim | @blockchain | Jun, 2022

A String of 200 ‘Sleeping Bitcoins’ From 2010 Worth $4.27 Million Moved on Friday

-

SEC7 months ago

SEC7 months agoJudge rules LBRY video platform’s token is a security in case brought by the US SEC

-

Antminer11 months ago

Antminer11 months agoWill the Bitcoin mining industry collapse? Analysts explain why crisis is really opportunity

-

Banking8 months ago

Banking8 months agoSilvergate Capital’s crypto-to-fiat transfers decrease by $50B compared to Q3 2021

-

Bitcoin8 months ago

Bitcoin8 months agoExchange Outflows Shows Bitcoin, Ethereum Accumulation Trend Continues

-

Altcoins12 months ago

Altcoins12 months agoBitcoin Dropped Below 2017 All-Time-High but Could Sellers be Getting Exhausted? – Blockchain News, Opinion, TV and Jobs

-

Uncategorized1 year ago

BNM DAO Token Airdrop

-

Binance11 months ago

Binance11 months agoWhat does the Coinbase Premium Gap Tell us about Investor Activity? – Blockchain News, Opinion, TV and Jobs

-

Asia11 months ago

Asia11 months agoFed policy and crumbling market sentiment could send the total crypto market cap back under $1T