Banking

Silvergate Capital’s crypto-to-fiat transfers decrease by $50B compared to Q3 2021

On Oct. 18, Silvergate Capital, a crypto-fiat gateway network designed for financial institutions, announced its financial results for Q3 2022.

The bank, known for services such as processing consumer fiat deposits to cryptocurrency exchanges, saw thetransfer volume on the Silvergate Exchange Network plummet close to $50 billion compared to Q3 2021. Silvergate handled $112.6 billion of such transfers in Q3 2022.

It appears that investors were less than satisfied with the results. Silvergate’s share price, as listed on the U.S. NASDAQ exchange, fell by close to 22% at the time of publication after the results were announced.

In addition, Alan Lane, Silvergate’s president and CEO, said in an earnings call with investors that the company would likely “miss its goal” of launching a stablecoin pegged to the U.S. dollar this year, citing ongoing regulatory compliance work. Earlier this year, Silvergate acquired Facebook’s (now Meta) former stablecoin project Diem. The company plans to integrate the Diem stablecoin into its own SEN technology.

Interestingly, the company’s profits actually surged 84% year-over-year to $43.328 million. This is because the bank relies on interest earned from its digital asset customers’ deposits, which stood at $13.2 billion in Q3. Over the past 12 months, the U.S. Federal Reserve has increased the benchmark Fed Funds Rate from 0.00% to 0.25% last September to 2.25% to 2.50% in Septembe 2022. Correspondingly, the average interest earned on Silvergate’s custodied assets increased from 1.27% in Q3 2021 to 2.58% in Q3 2022.

With regard to the results, CEO Alan Lane stated:

“While volumes on the Silvergate Exchange Network (SEN) decreased this quarter compared to the overall industry, we remain confident in the power of our platform and the opportunities for expansion within the network. We continued to see demand for our SEN Leverage product and growth in our new customer pipeline.”

Source link

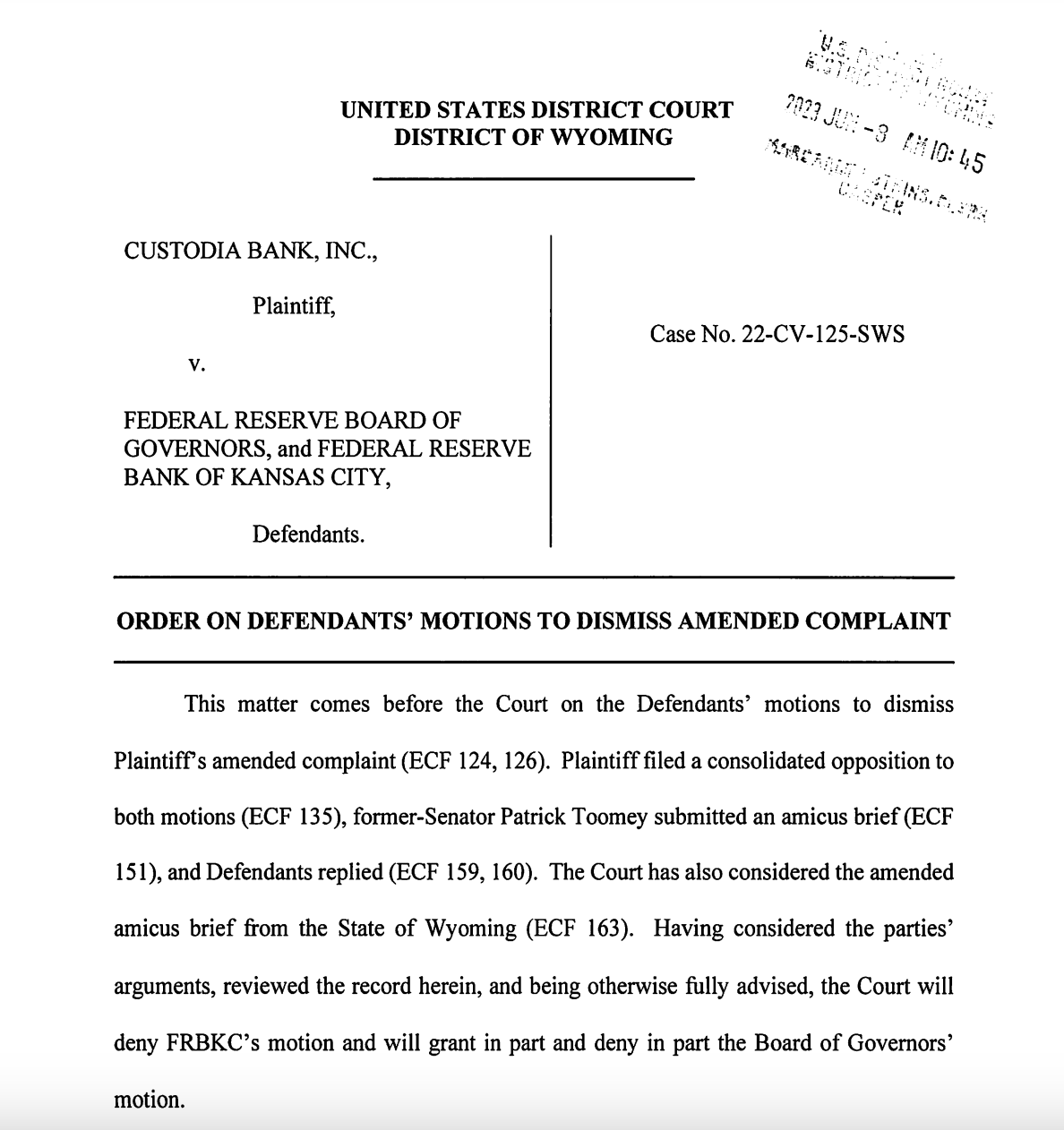

Custodia Bank won a step forward in its legal battle against the Federal Reserve, as a Wyoming federal judge denied dismissal motions from both the Fed and the Federal Reserve Bank of Kansas City.

The digital asset bank sued the Federal Reserve in June 2022, claiming an “unlawful delay” in processing an application for its master account. In 2020, Caitlin Long, former Morgan Stanley and an early proponent of Bitcoin, founded the bank to provide account services for crypto companies and serve as a bridge to the United States dollar.

“The Federal Reserve’s latest motion to dismiss Custodia Bank’s lawsuit was once again rejected. We are pleased that the Fed’s attempt to provide itself a veto over state bank chartering decisions will now be tested in federal court,” Nathan Miller, a spokesperson for Custodia Bank, told Cointelegraph in a statement.

Custodia submitted an application for a Federal Reserve master account in October 2020. The application, if granted, would enable the bank to use the Federal Reserve’s payment system, the FedWire network, which processed over 196 million transactions last year. In January 2023, the Fed denied the membership application, saying it was “inconsistent with the required factors under the law” and citing the bank’s involvement in the crypto space.

Custodia was one of Wyoming’s first Special Purpose Depository Institutions (SPDIs), also known as “blockchain banks.” SPDIs were created to serve businesses unable to secure Federal Deposit Insurance Corporation (FDIC) banking services due to their dealings with cryptocurrency. In April, the state of Wyoming requested to intervene in the case between the bank and the Fed, defending its framework allowing certain crypto firms to qualify as state-chartered banks.

According to Miller, the Fed is reinterpreting federal laws to grant itself special authority that it never received from Congress after decades of automatically granting master accounts to chartered banks.

“The Fed has never held such authority in U.S. history, nor does it need discretion to block banks that already have been validly chartered by state banking authorities that rigorously separate the wheat from the chaff,” Miller continued, adding that Custodia received its bank charter after more than 150 prospective applicants were rejected by the Wyoming Division of Banking. “We look forward to the court’s review of this power grab by the Fed,” he stated.

Magazine: The legal dangers of getting involved with DAOs

Source link

Boosting financial inclusion is one of crypto’s strongest value propositions. Yet, ironically, the banking crisis has effectively de-banked the crypto industry itself, at least in the United States.

How things panned out with Silvergate, Silicon Valley Bank and Signature — the three crypto-friendly U.S. banks — reeks of what Nic Carter called “Operation Chokepoint 2.0.” There’s good merit to this claim, though naysayers peddle conspiracy theory allegations with much harshness.

Signature, for one, did not face a bank run. The Federal Deposit Insurance Corporation still took the bank over in a jiffy. Anonymous sources even alleged the FDIC had asserted that any purchaser “must agree to give up all the crypto business,” though the agency walked back those claims.

I don’t want to alarm, but since the turn of the year, a new Operation Choke Point type operation began targeting the crypto space in the US. it is a well-coordinated effort to marginalize the industry and cut of its connectivity to the banking system - and it’s working

— nic carter (@nic__carter) February 7, 2023

Crypto not only has the resilience but also the tools to fight back — by leveraging stablecoins to minimize bank dependence. Besides solving an immediate crisis, it can also provide the ground to establish crypto as a self-sufficient and parallel financial system. That was Satoshi’s vision, after all.

U.S. regulators are shooting themselves in the foot

There’s a reason why most regulatory authorities — except in some progressive jurisdictions — have their guns blazing for crypto. Their power rests on the toxic relationship between governments, money printers, big corporations and oligopolies disguised as banking systems. The non-intermediated, permissionless and autonomous systems that crypto enables threatens this anti-individual nexus to its very core.

Our journey toward a more equitable, individual-centric world of crypto was never meant to be easy. The hyper-aggressive response from regulators is also pretty much in line with the expectations. But somehow the authorities, especially in the U.S., don’t seem to realize that their actions are self-destructive.

Related: Did regulators intentionally cause a run on banks?

Technological progress has been crucial in taking the U.S. to its current position of dominance in global geopolitics. Emerging crypto-based technologies enabled the next giant leap in this direction. And if only the regulators could overcome their greed for short-term power and control, they would see how stifling innovation isn’t in their best interest.

For instance, the ongoing banking crisis, which is very much due to misguided policy action and selective enforcement, ultimately hurts financial stability in the United States. Moreover, if it’s indeed a coordinated effort to de-bank the crypto industry, the average U.S. taxpayer is bearing most of the brunt, despite staying within legal limits.

Some projects have found a scalable way to assist crypto firms in becoming regulated institutions — such as Archblock, which onboards U.S.-based community banks to expand on-chain “real-world asset” financing for regulated entities.

While this approach might eventually resolve some regulatory tussles, a sizeable section of the global crypto community is rooting for more radical solutions.

Crypto firms don’t need banks when they have stablecoins

Stablecoins have been under much scrutiny since Terra’s “algorithmic” coin, TerraUSD (renamed to TerraClassicUSD, crashed last year, setting off a chain of events that partly led to the FTX fiasco. The crash wiped out an ecosystem worth $40 billion, but it also served valuable lessons in due diligence, overexposure and risk management.

Something like Operation Chokepoint 2.0, actual or hypothetical, is possible because crypto companies and investors use banks as on-ramps or off-ramps. There are practical reasons for this choice: One can’t buy crypto with cash, for example, and must pay with U.S. dollars from their bank account. Even while using an exchange, they need bank transfers to deposit fiat.

Related: The world could be facing a dark future thanks to CBDCs

Involving banks so much isn’t necessary, though. Stablecoins can offer the fiat tokenization services for which crypto companies depend on banks with much risk and despair. The process isn’t decentralized, but neither is banking for that matter. It’s not about decentralization here since the goal is to connect centralized and decentralized finance while minimizing counterparty risks.

Former BitMEX CEO Arthur Hayes published a richly informative blog on the subject in March in which he presented a detailed case for choosing stablecoins over banks. Most importantly, he proposed an innovative stablecoin model, which he called the Satoshi Nakamoto Dollar or NakaDollar (NUSD). The idea is to leverage Bitcoin (BTC) and inverse perpetual swaps such that NUSD doesn’t involve banks in the issuance or redemption process.

Proposals like NUSD are signs of our collective willingness to fight back in the face of regulatory uncertainty and aggressive onslaughts. As crypto evolves, there will be lesser attack surfaces for regulators, and we’ll have more robust alternatives to legacy systems.

Innovation isn’t merely a business model — it’s our biggest strength. And it is through innovation that crypto will overcome all hurdles. The show must go on since future generations deserve a better world.

Sarah Austin is the co-founder of QGlobe Games, a Steam-modeled gaming platform for crypto. She was the founding CMO of Kava Labs, the founding CEO of Pop17.com and the original community builder for Twitch. She graduated from the Dominican University of California before obtaining a data science certification from John Hopkins University.

This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Source link

As more institutions explore digital assets, the need for on-chain analytics platforms has never been higher.

Compliance experts, investigators and regulators employ these blockchain analytical tools to better understand the patterns and entities in cryptocurrency transactions.

To learn more about the tools and how they fit into broader cryptocurrency adoption, Cointelegraph sat down with Tom Robinson, the co-founder and chief scientist at analytics firm Elliptic; and Eray Akartuna, a senior cryptocurrency threat analyst at Elliptic.

Cointelegraph: What are the typical use cases you see for on-chain analytics for institutional clients?

Tom Robinson: Anti-Money Laundering (AML) and sanctions compliance for crypto exchanges and other businesses handling crypto assets: Our crypto transaction and wallet screening tools help businesses remain compliant with regulations and to reduce fraud.

Due diligence on crypto businesses: Our Discovery product provides risk profiles of exchanges and other crypto services based on analysis of their blockchain transactions. This is used by crypto businesses and financial institutions to gain insights into the businesses they are transacting with.

Magazine: ‘Moral responsibility’: Can blockchain really improve trust in AI?

Investigating crypto transactions: Investigator — our blockchain investigations software — allows graphical exploration of crypto wallets and the transactions between them. Law enforcement investigators use this to “follow the money” and link criminal activity to individuals. It is also used by crypto businesses to investigate potential illicit activity by their customers.

CT: How is Anti-Money Laundering in crypto different from mainstream AML within banks for fiat?

TR: The main difference is that most crypto transactions are visible on the blockchain. This makes it much easier to identify whether funds have originated from criminal activity by tracing them using blockchain analytics tools.

CT: Do you see a role for artificial intelligence (AI) and machine learning to play within on-chain analytics? Particularly within fraud prevention and AML?

Eray Akartuna: Yes, we already use machine learning within our blockchain analytics products. However, it’s very important to ensure the accuracy of these techniques through extensive testing.

There are certain aspects of blockchain transactions where we can use machine learning to understand or identify certain patterns. Patterns seen on the Bitcoin blockchain may not necessarily be the same as patterns on the Ethereum blockchain; they work in slightly different ways. I would point out the use of heuristics.

There are certain aspects of the blockchain transactions where we have common spend that will help us know whether the addresses are owned by a single entity or not — if I want to identify illicit activities and illicit actors on a blockchain — and identify their wallet addresses.

For instance, the North Korean cyber hackers were using a programmatic way of laundering. The hack was conducted in 2018, where they used about 113 wallets to disassociate funds from the original theft in an automated fashion. We could programmatically analyze the timestamps of those individual transactions to understand exactly how this automated software works.

If we are analyzing dark web markets or terrorist entities, etc., using heuristics can help us identify if a wallet address has been associated with a certain illicit entity. We can then use those heuristics to understand what other wallet addresses may also belong to or be associated with that entity.

We’ve got a risk score which fits into predictive analysis. When we look at the incoming and outcoming transactions to a cluster of wallets, we can see ultimately where they ended up. Entities identified as belonging to an exchange, a terrorist group or a dark market can be spotted when they are transacting with particular entities that we’re focusing on.

Let’s say about 50% of that crypto has gone to a certain dark web market; we can actually use that to provide a risk score of how risky the wallet is. The risk score is then used by exchanges and banks to decide if they want to do business with these wallet holders or not.

CT: What are the most complex problems you are solving at Elliptic? Why are they complex, and why is it important to solve them?

TR: The most complex and important problem we have solved recently is how to identify proceeds of crime in crypto, even when they have been laundered cross-asset and cross-chain. Criminals now move their proceeds between assets, using decentralized exchanges; and between blockchains, using cross-chain bridges.

We developed holistic screening as a way of automatically tracing crypto funds between assets and blockchains. This unique capability is now absolutely essential; otherwise, money launderers will exploit businesses’ lack of visibility into their activity.

CT: How do you see banks adopting digital assets and with that on-chain analytics? What has the uptake been so far?

EA: We are seeing slow but steady adoption, but compliance is top of mind for banks. Blockchain analytics is seen as an essential part of the puzzle and a way to assuage the concerns of regulators.

If institutions want to get involved in the decentralized finance (DeFi) space and plan to invest clients’ funds, they need to know whether the liquidity pool that they are investing in is credible and has the right risk profile. If the liquidity pool has illicit funds going in and out of it, there is a compliance issue there. That is a key use case for institutions who are looking to get involved in DeFi.

Recent: German banks slowly adopt crypto, mostly for institutional investors

The other use case is where some challenger banks like Revolut are allowing their customers to hold and trade cryptocurrencies. These banks will need compliance and AML capabilities before offering these products to customers.

CT: Have you had any interactions with regulators that would affect how you would serve the financial services industry, and what are the key areas of interest from a regulatory perspective?

TR: We have a constant dialogue with regulators around the world, many of whom use our products. It’s important that they understand how our blockchain analytics solutions function so that they can have confidence in the compliance programs run by the exchanges and banks that use our products.

Source link

XRP Allegedly Attacked By SEC’s Hinman For Ethereum’s Benefit

On-chain sleuth ZachXBT sued for libel after claiming plaintiff drained funds from project

Percentage Of ETH Addresses In Profit Reaches 5-Month Low

Think AI tools aren’t harvesting your data? Guess again

Bitcoin Bullish Momentum Building: Expert Predicts Rise To $27,200

Which altcoins will survive the SEC crackdown? Bitcoin OG explains

Curve (CRV) Observes 7% Bounce As Short Squeeze Occurs

Bakkt follows Robinhood, eToro in delisting major altcoins: Report

Shiba Inu Lead Developer Unveils Shibacals, Advancing Shibarium Development

dApp Store kit adopts new tech stack to power Web3 gaming development

Polygon Sees Surge In Whale Buying: Recovery In The Cards?

7 alternatives to ChatGPT

What Happens To Bitcoin Price If Spot ETF Is Approved?

SEC argues against Dentons’ motion to dismiss Terraform and Do Kwon’s lawsuit

Why Is Bitcoin Up Today?

Judge rules LBRY video platform’s token is a security in case brought by the US SEC

Will the Bitcoin mining industry collapse? Analysts explain why crisis is really opportunity

Silvergate Capital’s crypto-to-fiat transfers decrease by $50B compared to Q3 2021

Exchange Outflows Shows Bitcoin, Ethereum Accumulation Trend Continues

Bitcoin Dropped Below 2017 All-Time-High but Could Sellers be Getting Exhausted? – Blockchain News, Opinion, TV and Jobs

BNM DAO Token Airdrop

What does the Coinbase Premium Gap Tell us about Investor Activity? – Blockchain News, Opinion, TV and Jobs

Fed policy and crumbling market sentiment could send the total crypto market cap back under $1T

New Minting Services

Can Cardano’s July hard fork prevent ADA price from plunging 60%?

Friends or Enemies? – Blockchain News, Opinion, TV and Jobs

SEC’s Chairman Gensler Takes Aggressive Stance on Tokens – Blockchain News, Opinion, TV and Jobs

LUNA2 Recovers 70% In Nine Days From Historic Lows

Enjoy frictionless crypto purchases with Apple Pay and Google Pay | by Jim | @blockchain | Jun, 2022

A String of 200 ‘Sleeping Bitcoins’ From 2010 Worth $4.27 Million Moved on Friday

-

SEC7 months ago

SEC7 months agoJudge rules LBRY video platform’s token is a security in case brought by the US SEC

-

Antminer11 months ago

Antminer11 months agoWill the Bitcoin mining industry collapse? Analysts explain why crisis is really opportunity

-

Bitcoin8 months ago

Bitcoin8 months agoExchange Outflows Shows Bitcoin, Ethereum Accumulation Trend Continues

-

Altcoins12 months ago

Altcoins12 months agoBitcoin Dropped Below 2017 All-Time-High but Could Sellers be Getting Exhausted? – Blockchain News, Opinion, TV and Jobs

-

Uncategorized1 year ago

BNM DAO Token Airdrop

-

Binance11 months ago

Binance11 months agoWhat does the Coinbase Premium Gap Tell us about Investor Activity? – Blockchain News, Opinion, TV and Jobs

-

Asia11 months ago

Asia11 months agoFed policy and crumbling market sentiment could send the total crypto market cap back under $1T

-

Uncategorized2 years ago

New Minting Services